PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851197

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851197

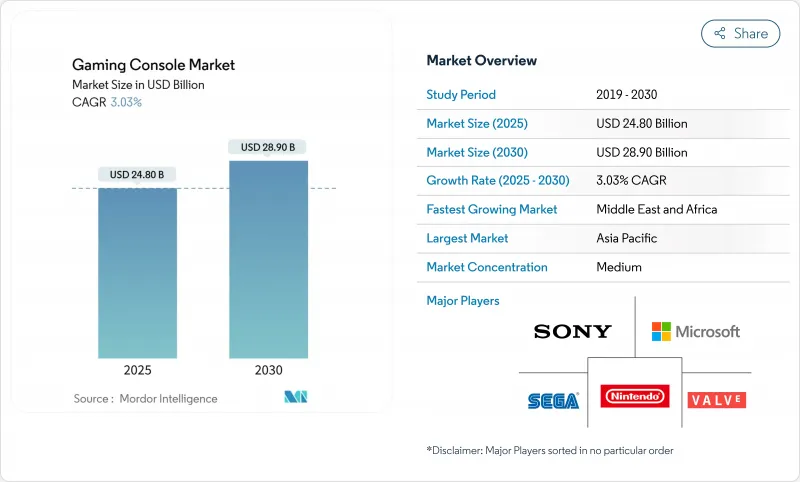

Gaming Console - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The gaming console market size is estimated at USD 24.8 billion in 2025 and is forecast to climb to USD 28.85 billion by 2030, progressing at a 3.03% CAGR between 2025 and 2030.

Demand stems from hardware refresh cycles triggered by visually intense AAA titles, the rapid spread of 8K UHD televisions in Asia, and lower bill-of-materials costs for hybrid devices using cloud-agnostic silicon. While established regions approach saturation, emerging economies in the Middle East, Africa, and Latin America present fresh revenue streams as broadband access widens and esports ecosystems mature. Competitive dynamics underscore Sony's continued dominance, Microsoft's pivot toward a services-first model, and Nintendo's focus on portable-hybrid innovation, even as smaller entrants leverage ARM-based architectures to address untapped niches. Supply-chain volatility around 5 nm wafers and rising substitution risk from cloud-only sticks temper growth yet also spur strategic partnerships that diversify sourcing and drive investments in regional assembly.

Global Gaming Console Market Trends and Insights

Launch of AAA-Grade, Photorealistic Titles Driving Hardware Refresh Cycles

Blockbuster releases such as Grand Theft Auto 6, slated for 2025, are expected to convert a significant portion of lingering PS4 users to new-generation systems. Sony's November 2024 launch of PS5 Pro, equipped with a 45% faster renderer and advanced ray-tracing, exemplifies the tight feedback loop linking software ambition with hardware capability. Historical performance underlines the effect: Hogwarts Legacy pushed PS5 sales up 30% month on month in early 2023, while Helldivers II and Final Fantasy VII Rebirth each added double-digit bumps during 2024 releases. Publishers and platform holders now coordinate launch calendars more closely, ensuring marquee titles arrive alongside or shortly after mid-cycle console upgrades that monetize pent-up demand.

Proliferation of 8K UHD TVs in Asia Accelerating Premium-Console Demand

Rising disposable income and aggressive television pricing have lifted 8K screen penetration across Japan and South Korea, compelling consumers to seek consoles that match display capabilities. Sony's PS5 Pro supports 8K at 60 FPS through PlayStation Spectral Super Resolution, turning the device into an aspirational companion for premium home-theater setups . The phenomenon extends to China, where domestic TV manufacturers bundle consoles in cross-promotions, reinforcing a virtuous upgrade cycle between display and gaming hardware. Early-adopter enthusiasm in Asia remains a bellwether for global high-end trends and informs production planning for the 2026-2027 console refresh window.

Regional league licences create strong local fan identities that, in turn, motivate hardware purchases required for competitive play. Console vendors have begun underwriting prize pools and training facilities, a move that accelerates adoption by embedding hardware standards into the esports rulebook. A logical outcome is that rising console usage in the Middle East and Africa mirrors earlier PC-gaming waves in Southeast Asia, albeit compressed into a shorter timeframe thanks to social-media amplification. Fiscal multipliers appear particularly high where telecom operators bundle low-latency connectivity with console-focused esports subscriptions.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Agnostic Silicon Designs Lowering BOM Costs for Hybrid Consoles

- Intensifying Substitution Threat from Cloud-Gaming-Only Sticks in North America

- Supply-Chain Volatility of Advanced 5 nm GPU Wafers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home systems preserved a 60% hold on 2024 revenue, underpinned by entrenched ecosystems and abundant 4K living-room displays. Yet hybrid devices form the fastest-moving cohort, advancing at a 5.9% CAGR to 2030. The upcoming Switch 2 promises backward compatibility plus an 8-inch screen, positioning it to accelerate hybrid uptake across Japan and family-oriented Western markets. Valve's Steam Deck validated premium handheld viability with 4 million units shipped, nudging Microsoft to prototype its own handheld "Keenan" for 2025. Micro-consoles in the "Others" bucket face intensified pressure from both hybrids and subscription sticks, narrowing their niche to retro enthusiasts and entry-level customers.

Consumer migration toward versatility hints at a structural pivot: households increasingly expect one device to bridge docked 4K play and portable sessions. Should hybrids secure incremental gains beyond their projected pace, the gaming console market size could tilt more decisively away from stationary hardware in the next cycle.

4 K-capable machines led 2024 revenue with a 64% share, supported by networked households sporting UHD screens. The next wave favors 8 K-ready systems, forecast to surge at a 9.4% CAGR. Sony's PS5 Pro already primes the channel, while AI-assisted upscalers such as Project Amethyst hint at strong value retention even if native 8K rendering remains content-limited. Asia's tech-savvy consumers set the adoption tempo: every percentage-point uptick in 8K TV ownership feeds premium console intent. Over time, AI-driven supersampling could allow mid-tier models to emulate flagship visuals, reshaping price ladders and smoothing transition risks for budget-conscious buyers.

Gaming Consoles Market is Segmented by Console Type (Home Consoles, Handheld Consoles, and More), Technology (HD Consoles, 4K-Capable Consoles, 8 K-Ready Consoles), Processor Architecture (x86-Based Consoles, ARM-Based Consoles, and More), End-User (Household / Individual, and More), Distribution Channel (Online Retailers and Marketplaces, Offline), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the gaming console market with a 37% share in 2024, sustained by robust gaming cultures and early adoption of 8K displays in Japan and South Korea. Localized content, exemplified by Arabic-language titles in Gulf markets, reveals the importance of cultural adaptation as regional publishers secure licensing deals. North America remains pivotal; the United States alone generated USD 4.9 billion in gaming revenue in March 2024, confirming high spending power and premium attach rates. Europe, meanwhile, balances console growth with a mobile-centric Gen-Z cohort that challenges traditional upgrade cycles.

Latin America gains momentum, paced by Brazil's May 2024 legal framework that reduces taxes on locally assembled consoles and encourages inward investment. The Middle East & Africa shows the steepest trajectory, logging a 4.8% CAGR to 2030 from a smaller base; Sony's stake in Carry1st supports distribution and payments infrastructure across sub-Saharan markets. Nigeria's anticipated 8.6% CAGR in video games and esports testifies to untapped potential where mobile penetration rises faster than fixed-line broadband. Supply-chain strategies now emphasize regional assembly, with Sony producing physical PS5 discs in Brazil to shorten lead times and dodge import tariffs .

- Sony Group Corporation

- Microsoft Corporation

- Nintendo Co., Ltd.

- Valve Corporation

- NVIDIA Corporation

- Tencent Holdings Ltd.

- Sega Sammy Holdings Inc.

- Atari SA

- Ayaneo

- GPD

- Razer Inc.

- Logitech International S.A.

- SNK Corporation

- Qualcomm Technologies, Inc.

- ASUS (ROG Ally business unit)

- Lenovo Group Limited

- Analogue, Inc.

- Anbernic Technology Co., Ltd.

- Blaze Entertainment (Evercade)

- MSI

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Launch of AAA-grade, photorealistic titles driving hardware refresh cycles

- 4.2.2 Proliferation of 8 K UHD TVs in Asia accelerating premium-console demand

- 4.2.3 Cloud-agnostic silicon designs lowering BOM costs for hybrid consoles

- 4.2.4 Esports franchise licensing boosting console penetration in emerging markets

- 4.2.5 Government subsidies on locally-assembled consoles in Brazil and India

- 4.3 Market Restraints

- 4.3.1 Intensifying substitution threat from cloud-gaming-only sticks in North America

- 4.3.2 Supply-chain volatility of advanced 5 nm GPU wafers

- 4.3.3 Rising mobile gaming stickiness among Gen-Z in Europe

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Console Type

- 5.1.1 Home Consoles

- 5.1.2 Handheld Consoles

- 5.1.3 Hybrid Consoles

- 5.1.4 Others (Micro-consoles / TV Boxes)

- 5.2 By Technology

- 5.2.1 HD (>1080 p) Consoles

- 5.2.2 4K-capable Consoles

- 5.2.3 8K-ready Consoles

- 5.3 By Processor Architecture

- 5.3.1 x86-based Consoles

- 5.3.2 ARM-based Consoles

- 5.3.3 Custom SoC-based Consoles

- 5.4 By End-user

- 5.4.1 Household / Individual

- 5.4.2 Commercial Gaming Lounges and Cafes

- 5.4.3 Institutional (Esports Clubs, Schools)

- 5.5 By Distribution Channel

- 5.5.1 Online Retailers and Marketplaces

- 5.5.2 Offline

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Sony Group Corporation

- 6.3.2 Microsoft Corporation

- 6.3.3 Nintendo Co., Ltd.

- 6.3.4 Valve Corporation

- 6.3.5 NVIDIA Corporation

- 6.3.6 Tencent Holdings Ltd.

- 6.3.7 Sega Sammy Holdings Inc.

- 6.3.8 Atari SA

- 6.3.9 Ayaneo

- 6.3.10 GPD

- 6.3.11 Razer Inc.

- 6.3.12 Logitech International S.A.

- 6.3.13 SNK Corporation

- 6.3.14 Qualcomm Technologies, Inc.

- 6.3.15 ASUS (ROG Ally business unit)

- 6.3.16 Lenovo Group Limited

- 6.3.17 Analogue, Inc.

- 6.3.18 Anbernic Technology Co., Ltd.

- 6.3.19 Blaze Entertainment (Evercade)

- 6.3.20 MSI

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment