PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940553

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940553

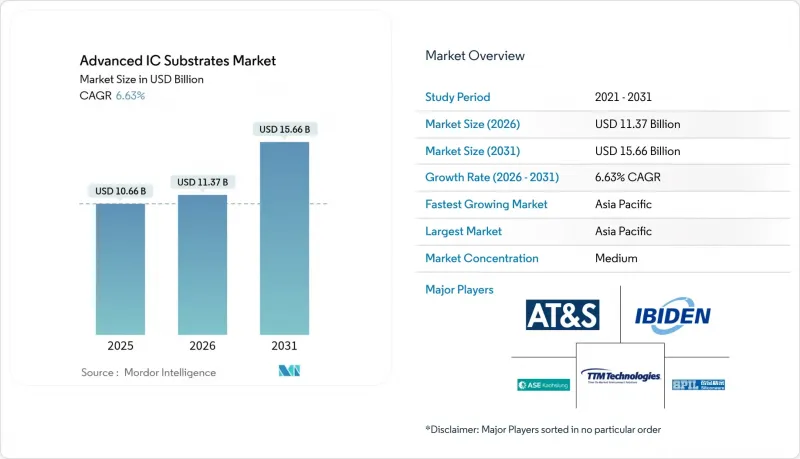

Advanced IC Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The advanced IC substrates market is expected to grow from USD 10.66 billion in 2025 to USD 11.37 billion in 2026 and is forecast to reach USD 15.66 billion by 2031 at 6.63% CAGR over 2026-2031.

Demand shifted decisively from traditional computing toward AI-centric workloads that require higher layer counts, finer linewidths, and tighter warpage control. Asia-Pacific-based substrate vendors benefited from this pivot because they already possessed high-volume ABF capacity and close relationships with foundry packaging lines. Major cloud service providers accelerated long-term purchase agreements in 2025 to secure guaranteed CoWoS and FC-BGA supply, further tilting pricing power to substrate producers. At the same time, glass-core innovation matured, creating a strategic alternative to ABF for ultra-high-density packages scheduled for commercial release in the latter half of the decade.

Global Advanced IC Substrates Market Trends and Insights

Surge in ABF-substrate demand for AI/HPC accelerators

Massive roll-outs of generative-AI servers in 2025 tightened supplies of Ajinomoto Build-up Film, pushing lead-times for ABF panels past 35 weeks and triggering spot-price premiums of up to 25% over 2024 contract levels. Taiwanese suppliers Unimicron, Kinsus, and Nan Ya PCB restored double-digit revenue growth after concluding a prolonged inventory correction, yet still operated at 90% utilization to keep pace with demand. Samsung Electro-Mechanics ramped AI-oriented ABF volume in Q2 2025 and started pilot glass-core runs, reflecting a dual-sourcing strategy aimed at mitigating single-material risk. TSMC disclosed plans to double annual CoWoS output, implying substrate demand well above existing capacity. Collectively, these moves widened a 20% supply gap that substrate makers do not expect to close until fresh lines come online in 2026.

Miniaturization and heterogeneous integration trend

Chiplet architectures, coreless interposers, and through-silicon vias redefined package design rules and pushed substrate line-widths below 10 µm in production settings. Applied Materials highlighted that on-package integration of discrete chiplets delivered superior performance per watt compared with monolithic die approaches. TOPPAN unveiled a coreless organic interposer with a 45% lower coefficient of thermal expansion than legacy ABF solutions, easing mechanical stress inside multi-die stacks. Broadcom's 3.5D XDSiP technology integrated more than 6,000 mm2 of silicon and 12 HBM stacks, underscoring the demand for substrates that can route thousands of high-speed signals in confined footprints. TSMC and ASE invested in panel-level packaging lines up to 310 X 310 mm to gain stepper efficiency and reduce cost per square inch. These shifts position the advanced IC substrates market as a pivotal enabler for next-generation compute density.

ABF-substrate capacity shortage and lead-time spikes

A persistent deficit in ABF panel output restricted upside for the advanced IC substrates market during 2024-2025. Ajinomoto, the near-monopoly supplier of ABF resin, acknowledged a 20% demand-supply gap that would remain until new resin reactors started in 2026. Foundries confirmed the constraint when TSMC said it could satisfy only 80% of CoWoS demand. Competitors such as Sekisui Chemical aimed to break dependence on alternate build-up chemistries, yet qualification cycles for high-end AI packages slowed adoption. Parallel shortages of T-Glass core material, prized for low expansion coefficients, delayed capacity expansions at Nittobo, compounding lead-time spikes. Substrate makers deployed inline metrology to raise first-pass yield and stretch existing capacity, but most customers still entered allocation programs through 2025.

Other drivers and restraints analyzed in the detailed report include:

- 5G build-out boosting high-frequency RF packaging

- Automotive-EV electrification needs high-reliability substrates

- High capital intensity and process complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

FC-BGA substrates accounted for 44.32% of the advanced IC substrates market share in 2025. Their lead is derived from proven electrical performance required by AI accelerators and server CPUs. Utilization stayed high through 2025 as GPU makers rushed to secure capacity. Growth, however, shifted toward rigid-flex CSP lines that served automotive domain controllers and foldable mobile devices. Rigid-flex volume increased at an 7.94% CAGR, attracting new laminate suppliers able to balance bend radius with controlled impedance. FC-CSP continued to service mid-tier mobile processors, but its cost pressures limited ASP upside. Organic BGA/LGA remained relevant for legacy desktop platforms, yet ceded design wins to flip-chip options. Panel-level FC substrates, still counted under "Others," emerged in pilot volumes at TSMC and ASE, promising 7X usable area per panel and opening new economies of scale.

FC-BGA stayed the workhorse for CoWoS build-ups. Designers demanded 14-26 layer counts, forcing tighter registration tolerances. In response, substrate makers installed AI-enabled optical inspection to catch via-to-trace violations early in the stack. Rigid-flex CSP benefited when automakers migrated infotainment units to 15-inch curved displays that required Z-axis flexibility. Increased camera integration in foldables presented an additional pull. These dynamics support sustained penetration for rigid-flex through 2031 while FC-BGA continues to anchor high-value positions within the advanced IC substrates market.

ABF represented 60.35% of the advanced IC substrates market size in 2025. Ajinomoto's exclusive resin recipe established consistent dielectric performance and drillability that customers trusted for 2.5D and 3D stacks. Suppliers expanded ABF mixing rooms in 2025, but output gains lagged demand growth, reinforcing seller leverage. Glass substrates, though less than 2% of 2025 shipments, recorded a 13.58% forecast CAGR. Flatness within +-5 µm across 200 mm x 200 mm plates allowed finer redistribution layers and higher I/O density than ABF. Intel's exit from in-house development validated third-party glass suppliers and accelerated ecosystem readiness.

BT resin preserved relevance in automotive control units where 150 °C board temperatures were common. Ceramic and LTCC segments supplied power devices exposed to continuous thermal cycling and offered incremental revenue buffers when ABF lines were oversold. Qualification of glass cores faced hurdles in via formation uniformity, but early builds delivered promising warpage metrics at reflow. AMD signaled its intention to switch its 2026 CPU platforms to glass, encouraging substrate makers to lock capacity slots well ahead of volume ramps. If yields hold, glass could equal or surpass 5.3% revenue share by 2031.

Advanced IC Substrates Market is Segmented by Substrate Type (FC-BGA, FC-CSP, Organic BGA/LGA, and More), Core Material (ABF, BT, Glass, and More), Packaging Technology (2D Flip-Chip, 2. 5D Interposer, and More), Device Node (>=28 Nm, 16/14-10 Nm, and More), End-Use Industry (Mobile and Consumer, Automotive and Transportation, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific captured 68.35% of the advanced IC substrates market in 2025. Taiwan's Unimicron, Kinsus, and Nan Ya PCB returned double-digit growth in 2025 as AI server demand replaced the inventory correction that weighed on 2023 shipments. Japan's resurgence, backed by JPY 3.9 trillion (USD 25.5 billion) in subsidies, re-established Kyushu as a packaging hub anchored by TSMC's Kumamoto fab. South Korea announced a USD 471 billion integrated cluster plan designed to deliver 7.7 million wafer starts per month by 2030, embedding ABF-CoWoS lines adjacent to logic fabs. China deployed regional incentives to build flip-chip and SiP capacity, but export restrictions narrowed tooling access, slowing glass-core adoption.

North America's advanced localization efforts under the CHIPS Act. TSMC's Arizona campus moved to a six-fab vision with potential ABF lines colocated for risk mitigation. Entegris secured up to USD 75 million in federal support for filtration media used in substrate copper plating. OSAT giants evaluated U.S. expansion to satisfy defense-oriented chip packaging mandates, though wage inflation remained a concern.

Europe focused on automotive and power devices. OnSemi's Czech SiC facility created an end-to-end supply chain for inverter substrates inside the bloc. Germany and France considered joint ABF pilot lines to support foundry expansions by Intel and TSMC. Meanwhile, Vietnam, India, and Malaysia pursued assembly subsidies. Amkor opened a USD 1.6 billion plant in Bac Ninh, and India approved INR 7,600 crore (USD 910 million) for an OSAT venture led by CG Power and Renesas. These moves diversified geographic risk in the advanced IC substrates market.

- ASE Technology Holding Co., Ltd.

- AT&S Austria Technologie & Systemtechnik AG

- Siliconware Precision Industries Co., Ltd.

- TTM Technologies, Inc.

- Ibiden Co., Ltd.

- Kyocera Corporation

- Fujitsu Interconnect Technologies Ltd.

- JCET Group Co., Ltd.

- Panasonic Holdings Corporation

- Kinsus Interconnect Technology Corp.

- Unimicron Technology Corp.

- Nan Ya Printed Circuit Board Corp.

- Samsung Electro-Mechanics Co., Ltd.

- LG Innotek Co., Ltd.

- Simmtech Co., Ltd.

- Shinko Electric Industries Co., Ltd.

- Shennan Circuits Co., Ltd.

- Zhen Ding Technology Holding Ltd.

- Daeduck Electronics Co., Ltd.

- Meiko Electronics Co., Ltd.

- WUS Printed Circuit Co., Ltd.

- Zhejiang Kingdom Sci-Tech Co., Ltd.

- SKC Absolics Inc.

- Tripod Technology Corp.

- Toppan Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in ABF-substrate demand for AI/HPC accelerators

- 4.2.2 Miniaturisation and heterogeneous integration trend

- 4.2.3 5G build-out boosting high-frequency RF packaging

- 4.2.4 Automotive-EV electrification needs high-reliability substrates

- 4.2.5 Glass-core substrates unlock >2X layer counts

- 4.2.6 CHIPS-style subsidies tied to substrate fabs

- 4.3 Market Restraints

- 4.3.1 ABF-substrate capacity shortage and lead-time spikes

- 4.3.2 High capital intensity and process complexity

- 4.3.3 Copper-clad-laminate price volatility

- 4.3.4 Tighter chemical-emission rules for build-up films

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Substrate Type

- 5.1.1 FC-BGA

- 5.1.2 FC-CSP

- 5.1.3 Organic BGA/LGA

- 5.1.4 Rigid-Flex and Flex CSP

- 5.1.5 Others

- 5.2 By Core Material

- 5.2.1 ABF

- 5.2.2 BT

- 5.2.3 Glass

- 5.2.4 LTCC / HTCC

- 5.2.5 Ceramic

- 5.3 By Packaging Technology

- 5.3.1 2D Flip-Chip

- 5.3.2 2.5D Interposer

- 5.3.3 3D-IC / SoIC

- 5.3.4 Fan-Out WLP

- 5.3.5 SiP / Module

- 5.4 By Device Node (nm)

- 5.4.1 >=28 nm

- 5.4.2 16/14-10 nm

- 5.4.3 7-5 nm

- 5.4.4 4 nm and below

- 5.5 By End-Use Industry

- 5.5.1 Mobile and Consumer

- 5.5.2 Automotive and Transportation

- 5.5.3 IT and Telecom Infrastructure

- 5.5.4 Data-centre / AI and HPC

- 5.5.5 Industrial, Medical and Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 Taiwan

- 5.6.4.5 India

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ASE Technology Holding Co., Ltd.

- 6.4.2 AT&S Austria Technologie & Systemtechnik AG

- 6.4.3 Siliconware Precision Industries Co., Ltd.

- 6.4.4 TTM Technologies, Inc.

- 6.4.5 Ibiden Co., Ltd.

- 6.4.6 Kyocera Corporation

- 6.4.7 Fujitsu Interconnect Technologies Ltd.

- 6.4.8 JCET Group Co., Ltd.

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Kinsus Interconnect Technology Corp.

- 6.4.11 Unimicron Technology Corp.

- 6.4.12 Nan Ya Printed Circuit Board Corp.

- 6.4.13 Samsung Electro-Mechanics Co., Ltd.

- 6.4.14 LG Innotek Co., Ltd.

- 6.4.15 Simmtech Co., Ltd.

- 6.4.16 Shinko Electric Industries Co., Ltd.

- 6.4.17 Shennan Circuits Co., Ltd.

- 6.4.18 Zhen Ding Technology Holding Ltd.

- 6.4.19 Daeduck Electronics Co., Ltd.

- 6.4.20 Meiko Electronics Co., Ltd.

- 6.4.21 WUS Printed Circuit Co., Ltd.

- 6.4.22 Zhejiang Kingdom Sci-Tech Co., Ltd.

- 6.4.23 SKC Absolics Inc.

- 6.4.24 Tripod Technology Corp.

- 6.4.25 Toppan Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment