Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687157

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687157

Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 183 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

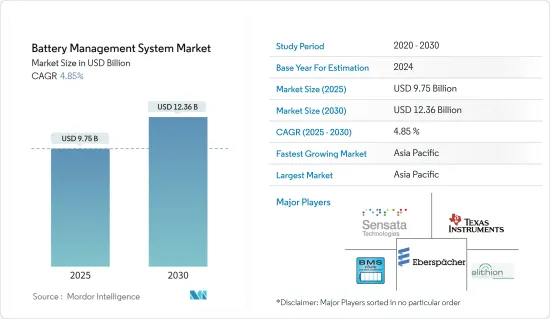

The Battery Management System Market size is estimated at USD 9.75 billion in 2025, and is expected to reach USD 12.36 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the medium term, the growing demand for battery management systems is expected to stimulate the market growth of battery management systems. Furthermore, the increasing adoption of electric vehicles, the need for robust charging infrastructure, and the focus on increasing the energy efficiency of batteries are also expected to drive the growth of the market studied.

- On the other hand, technological limitation on off-the-shelf battery management systems or standard battery management systems is one of the major restraints for the market.

- Nevertheless, technological advancements in battery management systems with advantages, such as reduced complexity, better efficiency, and improved reliability, among others, are expected to provide growth opportunities in the forecast period.

- The Asian-Pacific region dominates the market and is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the rapid rise in sales of electric vehicles in countries like China and Japan. This rise has been due to the extensive efforts of the governments to reduce greenhouse gas emissions.

Battery Management System Market Trends

Transportation Segment Expected to Dominate the Market

- Vehicles with internal combustion engines (ICE) were the only types used earlier. However, technology has been shifting toward electric vehicles (EVs) due to growing environmental concerns. Therefore, due to these reasons, battery management systems do not have any market in the ICE sector.

- Last year's global EV sales stood at around 6.6 million (including battery electric vehicles and plug-in hybrid electric vehicles). The sales are likely to increase further with various EV policy adoption by different countries globally.

- Lithium-ion batteries are mostly used in EVs as they provide high energy density, low self-discharge, less weight, and low maintenance. For ICE vehicles, the lead-based battery is widely used and is expected to continue to be the only viable mass-market battery system for the foreseeable future. Lithium-ion batteries still require higher cost reductions for use in SLI applications to be considered a viable mass-market alternative to lead-based batteries.

- Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Due to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology that meets OEM requirements for the vehicle driving range and charging time. The lead-based traction batteries are not competitive for use in full hybrid electric vehicles or electric vehicles because of their lower specific energy and higher weight.

- The global production of batteries for electric vehicles is mainly concentrated in the Asian-Pacific region, with Chinese, Japanese, and South Korean companies dominating the sector and building European factories to conserve their supremacy. China's significant market share in the midstream and downstream value chain of li-ion batteries makes it the largest producer of li-ion batteries globally. The country is also making efforts to reduce air pollution levels, which is expected to register a high growth rate in the sales of electric vehicles and lead to high demand for EV batteries.

- Additionally, China is the global hotspot for electric vehicle battery manufacturing. There are 93 Giga factories in China, and the country is projected to have around 130 by 2030; the country is expected to dominate the market during the forecast period. This, in turn, is expected to create tremendous demand scope for battery management systems in the country.

- Furthermore, the Indian state government has taken several initiatives to promote electric vehicles in the country. For instance, the Delhi government has an EV policy that provides incentives per Kwh of battery and per EV. For instance, the state provides about USD 120 as incentives per KWh battery capacity and about USD 1,850 incentives per EV. The main objective of such a scheme is to promote faster adoption of electric and hybrid vehicles in the Indian automotive market.

- In recent years, the Asian-Pacific region dominated the electric battery manufacturing market, and it is expected to continue to do so during the forecast period. Europe is expected to witness significant growth during the forecast period owing to factors like increasing investment in electric vehicle projects by various private players.

- For instance, in July 2022, Volkswagen planned to invest nearly USD 20 billion in developing EV batteries in a new company named Power Co in Germany. The plant production is expected to begin by 2025 and will likely cater to the demand for nearly 500,000 EVs in the upcoming years.

- Hence, based on the factors mentioned above, the transportation segment is likely to dominate the battery management systems market during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is likely to be a major market for battery management systems during the forecast period. In Asia-Pacific, China is expected to witness strong growth due to the rapid growth in the EV market.

- The rising demand for consumer electronics is likely to add to the demand for BMS, owing to the increasing integration of BMS in consumer electronics for safety purposes.

- China is the largest market for electric vehicles (EVs), with over 3.33 million EVs sold last year, and it is expected to remain the largest global electric car market. China accounted for almost 40% of global electric car sales in 2021.

- Earlier, foreign automakers faced a 25% import tariff or were required to build a factory in China with a cap of 50% ownership. Currently, the 50% ownership rule is relaxed for passenger cars. The rules restricting a foreign company from establishing more than two joint ventures producing similar vehicles in the country are also removed.

- The Government of China is likely to cut subsidies on electric vehicles by 30% in 2022 and eliminate it by the end of the year, as the electric vehicle industry in the country is now successful. The planned subsidy cut is aimed at reducing manufacturers' reliance on government funds for developing new technologies and vehicles.

- Furthermore, according to the Indian Brand Equity Foundation (IBEF), the Indian appliance and consumer durables market is expected to increase to a CAGR of 9%, accounting for INR 3.15 trillion in the current year. Furthermore, the Indian government anticipates that the Indian electronics manufacturing sector is likely to reach USD 300 billion in the future. Thus, the increasing demand for consumer electronics is likely to increase the demand for battery management systems in India during the forecast period.

- The automotive industry is one of India's major end users of battery management systems. In the automobile industry, BMS is used for critical applications such as temperature, voltage, current monitoring, battery state of charge (SoC), and cell balancing for lithium-ion batteries. In addition, the rising adoption of electric vehicles in India is driving the market for the automotive battery management system to provide safety, performance optimization, health monitoring and diagnostic of battery, and communication with other electronic control units (ECU).

- In June 2022, EV startup Mecwin India announced that it is likely to invest approximately USD 6.38 million to set up an EV motor, controller, and BMS systems manufacturing plant in Karnataka, India. The factory will likely have an initial manufacturing capacity of 2,000 units per day and will likely cater to the demand for EV Original Equipment Manufacturers (OEMs). Thus, such upcoming projects are likely to increase the demand for BMS systems in India during the forecast period.

- Therefore, the above-stated factors can be considered the major driving factors for battery management systems in the region, where the market is expected to grow during the forecast period.

Battery Management System Industry Overview

The battery management system market is moderately fragmented. Some of the major players in the market (in no particular order) include Eberspaecher Vecture Inc., Elithion Inc., BMS Powersafe, Texas Instruments Incorporated, and Sensata Technologies Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 55767

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Stationary

- 5.1.2 Portable

- 5.1.3 Transportation

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 Francy

- 5.2.2.3 Italy

- 5.2.2.4 United Kingdom

- 5.2.2.5 Russian Federation

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Eberspaecher Vecture Inc.

- 6.3.2 Elithion Inc.

- 6.3.3 Leclanche SA

- 6.3.4 Renesas Electronics Corporation

- 6.3.5 LION Smart GmbH

- 6.3.6 Sensata Technologies Inc.

- 6.3.7 RCRS Innovations Pvt. Ltd

- 6.3.8 Nuvation Energy

- 6.3.9 Texas Instruments Incorporated

- 6.3.10 BMS Powersafe

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.