PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907217

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907217

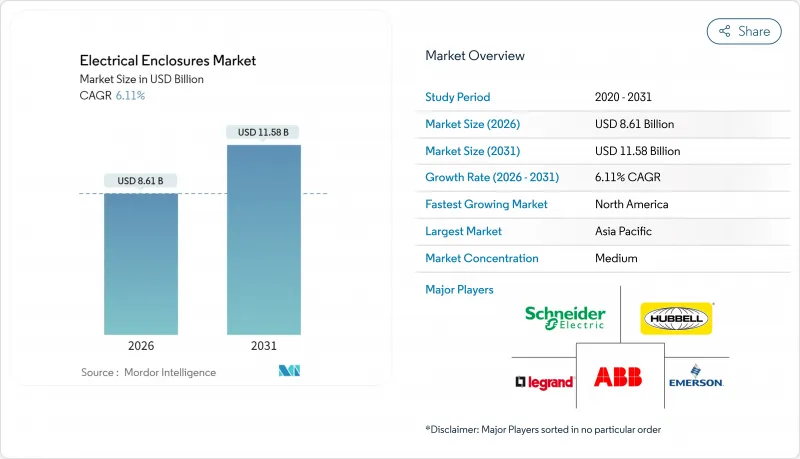

Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The electrical enclosures market was valued at USD 8.11 billion in 2025 and estimated to grow from USD 8.61 billion in 2026 to reach USD 11.58 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031).

Demand accelerates as utilities, factories and telecom providers replace legacy cabinets with intelligent housings that host sensors, edge processors and wireless modules. Rapid power-sector build-outs, 5G densification and the electrification of transportation keep ordering cycles robust, while material innovations such as UV-stabilized polycarbonate and fiberglass address corrosion, thermal and weight challenges. Vendors differentiate through modularity, thermal management and IIoT connectivity, driving strategic mergers focused on data-center, renewable-energy and grid-modernization niches.

Global Electrical Enclosures Market Trends and Insights

Accelerating Renewable-Energy Build-Out

Utility-scale solar and offshore-wind farms specify IP67/IP68 cabinets that tolerate salt spray, UV irradiance above 1,000 W/m2 and internal temperatures surpassing 70 °C. Active cooling, surge protection and integrated communication modules are now baseline requirements for photovoltaic combiner boxes, inverter housings and battery-energy-storage switchboards. Compliance with IEC 61215 and UL 1741 standards guides enclosure designs toward enhanced arc-fault detection and insulation tracking, supporting safe grid interconnection.

Industrial Automation and Industry 4.0 Expansion

Digitized plants embed vibration, humidity and temperature sensors directly in switchgear to cut unplanned downtime by up to 82%. As edge servers migrate from control rooms to the shop floor, cabinets must dissipate higher heat loads; every 10 °C rise inside a panel doubles outage risk. Modular frames and quick-mount rail systems enable rapid re-tooling, helping automotive, electronics and food producers align with make-to-order strategies.

Raw-Material Price Volatility

Aluminum premiums rose 10% in 2024 amid energy-cost spikes and export curbs, squeezing enclosure gross margins and prompting dual-sourcing pacts. Stainless-steel surcharges track nickel swings, pushing OEMs toward fiberglass and polycarbonate for cabinets exceeding 300 mm dimensions. Currency gyrations further complicate costing, prompting just-in-time inventories and price-adjustment clauses in multiyear framework deals.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Modernization and Substation Retrofits

- Stricter Global Safety and Ingress-Protection Codes

- Seal-Integrity and Thermal-Management Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic housings retained 74.15% of electrical enclosures market share in 2025, anchored by carbon steel in factory automation and 316L stainless in food, pharma and marine environments. The electrical enclosures market size for non-metallic alternatives is projected to grow at an 7.98% CAGR, outpacing the overall curve as polycarbonate delivers IK10 impact ratings and 25-year UV endurance at roughly one-third the cost of stainless. Fiberglass-reinforced polyester dominates cabinets larger than 300 mm X 300 mm thanks to moldability and chemical resistance, while aluminum addresses rail and aerospace weight targets.

Polycarbonate boxes integrate transparent lids for visual inspection and patent-pending hingeless snaps that cut assembly time by 40%. Fiberglass' dielectric strength supports live-line work, eliminating grounding hardware. Stainless continues to command hygienic applications where weld-less seams and smooth #4 finishes deter bacterial growth. Vendors compete on next-generation flame-retardant resins and bio-based composites that reduce lifecycle emissions without sacrificing performance.

Wall-mounted cabinets captured 46.20% revenue in 2025 for distributed control loops and building automation endpoints. Facility expansions and data centers, however, are driving the electrical enclosures market toward floor-standing racks, forecast to post a 7.51% CAGR as hyperscale operators adopt aisle-containment frames with 3,500-lb load ratings. Modular base plinths enable cable entry from any side, while seismic kits satisfy Zone 4 requirements in California and Japan.

Pole- and pad-mounted variants support utility metering, EV chargers and 5G nodes, combining powder-coated aluminum shells with vandal-proof locks. Underground housings serve suburban distribution networks, hiding switchgear beneath grade-level lids to preserve streetscape aesthetics. Manufacturers push quick-swing doors and 180-degree hinges that let technicians service gear without obstruction in cramped corridors.

The Electrical Enclosures Market Report is Segmented by Material (Metallic, and Non-Metallic), Mounting Type (Wall-Mounted, Floor-mounted/Free-standing, and More), Form Factor (Small [Less Than or Equal To 10L], Compact [10-50L], and More), End-User Industry (Energy and Power, Oil and Gas, Industrial Manufacturing and Robotics, Metals and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 38.10% of 2025 revenue, led by United States initiatives to replace aging switchgear and harden grids against cyber threats. Federal funding drives smart-grid rollouts that specify enclosure-level intrusion detection and IEEE 1613-rated surge protection. Canada adds demand from mining, LNG and wind projects that face -40 °C winters, favoring fiberglass and double-wall steel for thermal buffering.

Asia-Pacific will register the quickest 7.22% CAGR as governments channel more than USD 3 trillion into transmission corridors, semiconductor fabs and high-speed rail. China transitions from welded sheet-metal boxes to intelligent, sensor-rich cabinets that feed substation digital twins. India's smart-city plans couple 33-kV ring-main units with pad-mounted composite kiosks capable of resisting monsoon floods. Southeast Asia absorbs relocated electronics manufacturing, lifting orders for stainless controls that endure 90% relative humidity.

Europe advances steadily on offshore-wind, hydrogen and factory-automation programs. Germany leads Industry 4.0 adoption, embedding condition monitoring in Rittal VX series racks. Nordic utilities request cold-climate enclosures that deploy silicon heaters and breathable hydrophilic vents. The EU Cyber-Resilience Act pushes OEMs to embed secure boot and tamper logging at the panel door, elevating certification complexity.

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation plc

- nVent Electric plc (Hoffman and Schroff)

- Rittal GmbH and Co. KG

- Emerson Electric Company

- Hubbell Incorporated

- Pentair plc

- Legrand SA

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet (Scott Fetzer Company)

- Allied Moulded Products, Inc.

- Fibox Oy Ab

- Eldon Holding AB

- Siemens AG

- General Electric Company

- Saginaw Control and Engineering

- BOXCO Co., Ltd.

- Nitto Kogyo Corp.

- Socomec Group SA

- Bison ProFab Inc.

- Integra Enclosures Inc.

- Austin Electrical Enclosures

- ITS Enclosures (Builder's Service Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating renewable-energy build-out

- 4.2.2 Industrial automation and Industry 4.0 expansion

- 4.2.3 Grid-modernization and substation retrofits

- 4.2.4 Stricter global safety and ingress-protection codes

- 4.2.5 Outdoor 5G small-cell rollout needing IP-rated housings

- 4.2.6 Smart, IoT-enabled enclosures for predictive maintenance

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (steel, aluminium)

- 4.3.2 Seal-integrity and thermal-management failures

- 4.3.3 Cyber-attack risk in connected enclosures

- 4.3.4 Skilled-labour shortage for custom fabrication

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Metallic (Carbon Steel, Stainless Steel, Aluminum)

- 5.1.2 Non-metallic (Polycarbonate, Fiberglass, Polyester, ABS)

- 5.2 By Mounting Type

- 5.2.1 Wall-mounted

- 5.2.2 Floor-mounted / Free-standing

- 5.2.3 Underground / Pad-mounted

- 5.2.4 Pole-mounted

- 5.3 By Form Factor

- 5.3.1 Small (Less than or Equal to 10 L)

- 5.3.2 Compact (10-50 L)

- 5.3.3 Free-size / Full-size (Above 50 L)

- 5.3.4 Modular / Configurable systems

- 5.4 By End-user Industry

- 5.4.1 Energy and Power

- 5.4.2 Oil and Gas

- 5.4.3 Industrial Manufacturing and Robotics

- 5.4.4 Metals and Mining

- 5.4.5 Transportation (Rail, Road, Air, EV-charging)

- 5.4.6 Data Centres and Telecom

- 5.4.7 Food and Beverage and Pharmaceuticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd.

- 6.4.3 Eaton Corporation plc

- 6.4.4 nVent Electric plc (Hoffman and Schroff)

- 6.4.5 Rittal GmbH and Co. KG

- 6.4.6 Emerson Electric Company

- 6.4.7 Hubbell Incorporated

- 6.4.8 Pentair plc

- 6.4.9 Legrand SA

- 6.4.10 Hammond Manufacturing Ltd.

- 6.4.11 AZZ Inc.

- 6.4.12 Adalet (Scott Fetzer Company)

- 6.4.13 Allied Moulded Products, Inc.

- 6.4.14 Fibox Oy Ab

- 6.4.15 Eldon Holding AB

- 6.4.16 Siemens AG

- 6.4.17 General Electric Company

- 6.4.18 Saginaw Control and Engineering

- 6.4.19 BOXCO Co., Ltd.

- 6.4.20 Nitto Kogyo Corp.

- 6.4.21 Socomec Group SA

- 6.4.22 Bison ProFab Inc.

- 6.4.23 Integra Enclosures Inc.

- 6.4.24 Austin Electrical Enclosures

- 6.4.25 ITS Enclosures (Builder's Service Company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment