PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685953

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685953

Structural Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

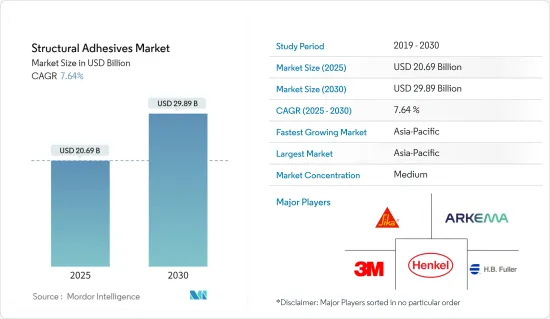

The Structural Adhesives Market size is estimated at USD 20.69 billion in 2025, and is expected to reach USD 29.89 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. However, it recovered significantly in 2021, owing to rising consumption from various end-user industries, such as construction, automotive, and wind energy.

Key Highlights

- Over the short term, the increasing investments in developing Asia-Pacific economies and increasing demand from the global construction and automotive sectors may drive the market studied.

- However, growing environmental and health concerns are expected to hinder the growth of the studied market.

- The growing research on underwater structural adhesives is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market, with the most significant consumption recorded in China.

Structural Adhesives Market Trends

Increasing Demand from the Construction Industry

- In the construction sector, structural adhesives are used to bond materials to withstand loads or stresses. These adhesives offer good impact resistance, fracture toughness, and structural flexibility without affecting bond strength.

- In the construction sector, structural adhesives provide durability to concrete, load-bearing materials, metals such as aluminum and steel, plastics, engineered woods, etc. Apart from durability, structural adhesives are energy-efficient and aesthetically appealing. They also reduce the need for maintenance. These characteristics extend the life cycle of building facades and bridges.

- Some essential structural adhesives used in the construction industry include acrylic structural adhesives, steel glue, anchor glue, pouring glue, carbon fiber reinforcement glue, dry-hanging adhesives, and silicone structural adhesives.

- With growing construction activity worldwide, the demand for structural adhesives is projected to increase during the forecast period. The global construction market was valued at around USD 7.2 trillion in 2021 and is likely to witness a growth rate of 3.6% in 2022.

- The construction sector in the Asia-Pacific region is the largest in the world and is expanding at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization. The highest growth for housing is also expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. According to the National Bureau of Statistics of China, the output value of the construction works in the country in 2021 was CNY 25.92 trillion (~USD 4.03 trillion), increasing from CNY 23.27 trillion (~ USD 3.62 trillion) in 2020.

- The United States occupies a significant share of the North American construction industry. Canada and Mexico also contribute significantly to the construction sector. According to the US Census Bureau, the value of new construction put in place in the country accounted for USD 1,626,444 million in 2021, increasing from USD 1,499,570 million in 2020.

- Therefore, all the factors mentioned above are likely to impact the demand in the market studied significantly.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global structural adhesives market in 2021. China is one of the world's largest consumers of structural adhesives.

- According to China's Five-Year Plan, unveiled in January 2022, the country's construction industry is estimated to register a growth rate of approximately 6% in 2022. China plans to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites.

- Moreover, as per the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects with an estimated investment of around USD 142 billion. These projects are in progress and are estimated to be completed by 2023.

- China is the largest manufacturer of automobiles in the world. According to the OICA, the automotive production in the country reached 26.08 million in 2021, which increased by 3% compared to 25.23 million vehicles produced in 2020. The increase in automotive production is estimated to drive the demand for structural adhesives, especially in the high-end vehicle manufacturing sector.

- Furthermore, as per the Stockholm International Peace Research Institute (SIPRI), China, the world's second-largest spender on the military after the United States, allocated an estimated USD 293 billion to its military in 2021. This was an increase of 4.7% compared to 2020. The 2021 Chinese budget was the first under the 14th Five-Year Plan, which runs until 2025.

- India's massive construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing for all by 2022, are expected to prove an impetus to the slowing construction industry.

- The automotive and aerospace sectors are the other significant users of structural adhesives. According to OICA, around 4,399,112 vehicles were produced in India in 2021, which increased by 30% compared to 3,381,819 units in 2020.

- The factors above are expected to affect the demand for structural adhesives in the Asia-Pacific region over the forecast period.

Structural Adhesives Industry Overview

The global structural adhesives market is partially fragmented in nature, with the presence of various international and domestic players. Some of the major players include Henkel AG & Co. KGaA, Sika AG, 3M, H.B. Fuller Company, and Arkema (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Investments in Developing Economies in Asia-Pacific

- 4.1.2 Increasing Demand from the Global Construction and Automotive Sectors

- 4.2 Restraints

- 4.2.1 Growing Environmental and Health Concerns

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Cyanoacrylate

- 5.1.5 Methyl Methacrylate

- 5.1.6 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.2 Automotive

- 5.2.3 Aerospace

- 5.2.4 Wind Energy

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Bondloc UK Ltd

- 6.4.4 DuPont

- 6.4.5 Engineered Bonding Solutions LLC

- 6.4.6 Forgeway Ltd

- 6.4.7 H. B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Illinois Tool Works Inc.

- 6.4.11 LG Chem

- 6.4.12 Parker Hannifin Corp.

- 6.4.13 Sika AG

- 6.4.14 RS Industrial

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research on Underwater Structural Adhesives