Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637890

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1637890

Residential Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 125 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

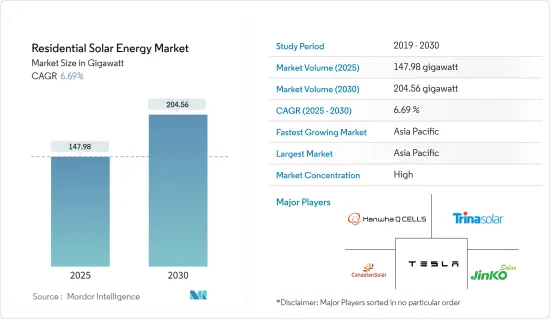

The Residential Solar Energy Market size is estimated at 147.98 gigawatt in 2025, and is expected to reach 204.56 gigawatt by 2030, at a CAGR of 6.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as favorable government policies, increasing investments in upcoming rooftop solar projects, and the reduced cost of solar energy, which has led to increased adoption of solar energy, are expected to drive the market during the forecast period.

- On the other hand, the lack of financing options and the difficulties in integrating residential solar PV systems in regions like Africa are expected to restrain the market's growth.

- However, ambitious targets are being undertaken to increase the renewable share in their energy mix. Governments across these nations also plan to increase the renewable energy share by deploying residential solar PV systems in the coming years. This factor, in turn, is expected to act as an opportunity for residential solar energy manufacturers and suppliers during the forecast period.

- Asia-Pacific is expected to be the fastest-growing market during the forecast period due to the rising energy demand. This growth is attributed to increasing investments and supportive government policies in Asia-Pacific countries, including India, China, and Australia.

Residential Solar Energy Market Trends

Increasing Rooftop Solar Installations to Drive the Market

- The increasing adoption of solar PV systems in the residential sector is primarily driven by expected savings in electricity costs, the need for an alternative source of electricity, and the desire to mitigate climate change risk.

- During the forecast period, the demand for rooftop solar PV is expected to increase due to decreasing solar PV costs, supportive government policies for residential solar PV, FIT programs and incentives, and various solar energy targets.

- The cost of electricity for residential rooftop solar PV applications has rapidly declined in recent years. The falling price has resulted in a massive increase in the global residential PV capacity, and many countries are increasing their residential rooftop targets.

- The Solar Energy Industry Association (SEIA) statistics show that, in 2023, the cumulative residential solar PV installed capacity in the United States accounted for about 36.268 GW. The total installed capacity grew by 23% compared to the previous year. The hike in capacity is mainly due to high household electricity bills and power outages.

- A European Joint Research Centre analysis shows that EU rooftop PV could produce 680 TWh of solar electricity annually.

- In April 2024, the German parliament approved a new series of measures to support solar PV development in the country. Rooftop solar PV installations of 40 kW are made eligible for feed-in tariffs that will be EUR 1.5c/kWh higher than current tariff levels. In addition, the new law increases the limit for ground-mounted solar projects from 20 MW to 50 MW in tenders for large-scale installations. Finally, it will become easier for households to deploy PV balcony systems and smart energy communities.

- All such factors are expected to drive the demand for residential solar energy over the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific accounted for more than 30% of the global residential solar PV market. It is expected to continue its dominance during the forecast period.

- India's solar PV installed capacity increased significantly from 63.048 GW in 2022 to 72.767 GW in 2023, and the demand for power is expected to increase further in the coming years.

- To cater to the rising power demand and meet its renewable energy target of 500 GW by 2030, the Indian government plans to increase the installed capacity of rooftop solar energy in the residential sector to around 4 GW by 2026. Thus, the government has initiated various policies for the residential sector to adopt solar energy to achieve the target.

- The Ministry of New and Renewable Energy (MNRE)'s grid-connected rooftop solar program aims to offer a 40% subsidy for the first 3 kW of generation capacity in rooftop systems and a 20% subsidy up to a 10 kW ceiling.

- Apart from schemes, the rooftop solar energy market for the residential sector seems appealing in India due to its increasing electricity tariff. On average, the electricity tariff in India is around INR 6-9 per unit, which is likely to increase due to a rise in electricity demand. In H1 2023, Indian states like Assam, Karnataka, Maharashtra, and Tamil Nadu raised their tariff for residential users. Hence, people are likely to adopt rooftop solar PV systems in their homes to reduce or make zero electricity bills.

- At the end of 2023, the Chinese government proposed to cover 50% of rooftop space with solar panels on party and government buildings, 40% of schools, hospitals, and other public facilities, 30% of industrial and commercial areas, and 20% of rural households. A total of 676 counties from 31 provinces have registered for the scheme.

- Owing to such factors, the demand for residential solar energy is expected to increase in Asia-Pacific over the forecast period.

Residential Solar Energy Industry Overview

The residential solar energy market is fragmented. Some of the major players in the market (in no particular order) include Trina Solar Co. Ltd, Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Hanwha Q Cells Co. Ltd, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 48265

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Renewable Energy Mix, Global, 2023

- 4.3 Residential Solar Energy Installed Capacity and Forecast, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Favorable Government Policies

- 4.6.1.2 Reduced Cost of Solar Energy Systems

- 4.6.2 Restraints

- 4.6.2.1 Lack of Financing Options Coupled with Difficulties in Integrating Residential Solar PV Systems in Regions like Africa

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION - By Geography

- 5.1 North America

- 5.1.1 United States

- 5.1.2 Canada

- 5.1.3 Rest of North America

- 5.2 Europe

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Spain

- 5.2.6 Russia

- 5.2.7 NORDIC

- 5.2.8 Turkey

- 5.2.9 Rest of Europe

- 5.3 Asia-Pacific

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Australia

- 5.3.5 Malaysia

- 5.3.6 Thailand

- 5.3.7 Indonesia

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia-Pacific

- 5.4 South America

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Rest of South America

- 5.5 Middle East and Africa

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 South Africa

- 5.5.4 Qatar

- 5.5.5 Nigeria

- 5.5.6 Egypt

- 5.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Trina Solar Co. Ltd

- 6.3.2 Yingli Green Energy Holding Company Limited

- 6.3.3 Canadian Solar Inc.

- 6.3.4 JinkoSolar Holding Co. Ltd

- 6.3.5 JA Solar Holdings Co. Ltd

- 6.3.6 Sharp Corporation

- 6.3.7 ReneSola Ltd

- 6.3.8 Hanwha Q Cells Co. Ltd

- 6.3.9 SunPower Corporation

- 6.3.10 Tesla Inc.

- 6.4 List of Other Prominent Players

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Targets to Increase the Renewable Share in Total Energy Mix Worldwide

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.