PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690934

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690934

North America Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

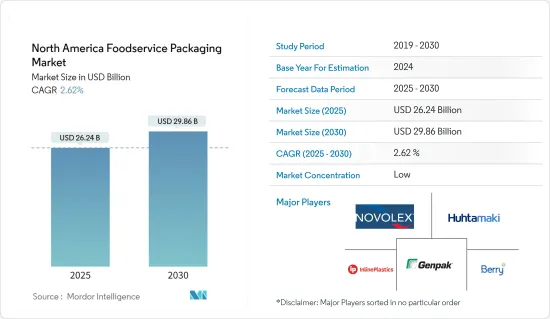

The North America Foodservice Packaging Market size is estimated at USD 26.24 billion in 2025, and is expected to reach USD 29.86 billion by 2030, at a CAGR of 2.62% during the forecast period (2025-2030).

Key Highlights

- The market's growth expansion has been brought on by consumers' heavy reliance on packaged foods and the significant regional presence of food processing businesses. The rising number of foodservice suppliers successfully digitalizing their operations is expected to fuel the industry, supported by the increasing demand for online food ordering, creating an opportunity for market growth in North America.

- The North American foodservice packaging business has experienced consistent growth over the last decade due to changes in substrate choice, new market expansion, ownership dynamics, and numerous developments serving the market for corrugated boxes, cartons, and plastic packaging. Sustainability and environmental issues will continue to be prioritized, especially in the United States.

- Corrugated boxes are types of packaging used to ship different food products. They are often constructed of paperboard, primarily made of cellulose fibers from wood. These boxes are strong, stiff, flexible, long-lasting, light, and attractive. Due to their recyclable nature and lack of use of hazardous chemicals during production, the boxes are advantageous for the environment. Corrugated boxes are used in the North American foodservice industry to package goods. Plastic bottle packing is the principal application for polyethylene. It is a semi-crystalline, lightweight thermoplastic resin with excellent sound insulation, chemical resistance, and low moisture absorption.

- The industry's most significant source of worry is the region's strict environmental restrictions. Over the projection period, bans on plastic items at the national and state levels are projected to present significant difficulties to the industry. Additionally, the growth of raw material prices and the supply chain uncertainty in polymer resins due to macroeconomic factors may challenge the market's growth during the forecast period.

- The foodservice industry's profit margins have been significantly affected by the COVID-19 pandemic. Businesses in this industry are witnessing a notable drop in consumption, coupled with disruptions in their supply chains. The COVID-19 pandemic-induced lockdowns substantially impacted the US foodservice industry with a temporary dip in packaging volumes, and the industry gradually recovered, defying economic challenges. Limited and full-service restaurants are expected to ramp up their consumer-facing packaging post-pandemic. As the economies reopen and diners embrace new eating habits, foodservice packaging must adapt to cater to these evolving needs, driving market growth.

North America Foodservice Packaging Market Trends

Corrugated Boxes and Cartons Segment to Exhibit the Highest Growth Rate

- Corrugated boxes are used only once and then recycled, minimizing the risk of cross-contamination. Additionally, the high heat used in manufacturing ensures they are free from bacteria and other contaminants. They provide a clean, safe environment for food items during transit, storage, and delivery, which is boosting their adoption in the foodservice packaging market in North America.

- Corrugated boxes boast a safety feature and are approved for direct food contact. Moreover, these boxes can be coated with food-safe materials, bolstering their appeal for food packaging. One standard option for a food-safe coating is a water-based or vegetable-based coating that complies with regulatory standards for direct food contact. This coating can be used as a protective layer, preventing any potential migration of substances from the box to the food. It is designed to be non-toxic and moisture-resistant, ensuring the packaging remains intact and safe for food items, supporting its growth in the market studied.

- Sustainability plays a crucial role in all industries, including food packaging. Corrugated boxes score highly in this regard as they are made from renewable resources. Most are manufactured from recycled materials and support circular economies as they can be easily recycled again, which reduces their environmental footprint, thereby supporting their growth in the North American market during the forecast period.

- The International Paper Company, a US-based pulp and paper company, reported the shipments of corrugated packaging in the United States to be growing in line with the increasing growth of shipments of packing products in the country, showing the future growth potential of the segment in the market studied.

- Additionally, with their sturdy construction, versatility, and safe properties, corrugated boxes and cartons have secured their place as a preferred choice in food packaging. They protect and preserve the food products inside and ensure their safe transportation to consumers. Coupled with their sustainable nature, corrugated boxes are a proper win-win solution, benefiting the food industry and supporting the segment's growth in the market studied.

Quick-service Restaurants Hold the Highest Market Share

- The use of sustainable foodservice packaging in QSRs has become crucial. More people are turning to fast food as a supper option because they have less time to prepare meals at home. Foodservice businesses may package meals safely and affordably using sustainable packaging styles, giving clients a quick and easy way to transport meals.

- Most of the foodservice items used in QSRs are either made of plastic, such as expanded polystyrene (EPS), polyethylene terephthalate (PET), polypropylene (PP), and polylactic acid, or paper, including paper, paperboard, and molded pulp. QSRs deliver high-quality food and beverages more quickly than traditional restaurants or cafes. To achieve fair distribution and a high level of consistency in offering these services, several QSRs have implemented dispensers that supply a controlled volume, supporting market growth.

- Some QSRs combine restaurant conveniences with the freedom for customers to express their uniqueness through self-service elements through controlled-volume dispensers, which can help QSRs deliver exceptional customer service, reduce product waste, and save money. The demand for packaging solutions for these small-volume sachets or packets across QSRs in the region is expected to create a growth opportunity for the market over the forecast period.

- Fast food and QSR chains based in the United States are expanding their portfolios in Canada to address the increasing demand for packaged foods, which would support market growth. For instance, in June 2024, the US fast-food chain Shake Shack, known for its burgers and fries, opened its first Canadian location in Toronto, which would fuel the demand for packaging solutions in the foodservice industry during the forecast period.

- Additionally, in August 2023, Inmobi, a contextual mobile advertising company, reported that people were ordering pizza and burgers as the most preferred fast food items in the United States. Such factors could create demand for the foodservice packaging market in the country and support the regional market's growth during the forecast period.

North America Foodservice Packaging Industry Overview

The North American foodservice packaging market will be highly fragmented over the forecast period, with the presence of many players, such as Inline Plastics, Berry Global Inc., Novolex Holdings LLC, Genpak LLC, and Huhtamaki America Inc. There will be increasing competition among local vendors in the region. Owing to the wide range of foodservice packaging suppliers, buyers can choose from multiple vendors.

- May 2024 - Foodservice manufacturing company Genpak invested USD 22.8 million in renovating its Montgomery, Alabama, plant. The upgrades allowed the facility to double its local workforce and included safety enhancements and upgrades focused on better efficiency for the manufacturer's food packaging solutions for clients ranging from convenience stores to restaurants.

- April 2024 - Novolex Holdings LLC, a North American company, announced a strategic investment in Rhode Island-based reusable systems and container brand OZZI. As a part of this investment, Eco-Products, a Novolex business unit and leader in circular solutions for the foodservice industry, will help accelerate OZZI's growth. The OZZI family of products and solutions includes O2GO containers, cups, and cutlery for foodservice packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Convenience Food Remains High in the United States

- 4.2.2 Increasing Emphasis on Sustainability is Causing Vendors to Focus on Recycled Plastic

- 4.3 Market Challenges

- 4.3.1 Increasing Governmental Regulations on Packaging Due to Environmental Pressure and Uncertainty in Polymer Prices

- 4.4 Market Opportunities

- 4.5 Industry Ecosystem Analysis - Material Suppliers, Convertors, Distributors, End-use Organizations, Customers, and Recycling

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET SEGMENTATION

- 5.1 By Packaging Format

- 5.1.1 Corrugated Boxes and Cartons

- 5.1.2 Plastic Bottles

- 5.1.3 Trays, Plates, Food Containers, and Bowls

- 5.1.4 Cups and Lids

- 5.1.5 Clamshells

- 5.1.6 Other Packaging Formats (Cutlery, Stirrers/Straws, etc.)

- 5.2 By End User

- 5.2.1 Quick-service Restaurants

- 5.2.2 Full-service Restaurants

- 5.2.3 Coffee and Snack Outlets

- 5.2.4 Retail Establishments

- 5.2.5 Institutions and Hospitality

- 5.2.6 Other End Users

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pactiv Evergreen Inc.

- 6.1.2 Dart Container Corporation

- 6.1.3 Amhil North America

- 6.1.4 Genpak LLC

- 6.1.5 Huhtamaki America Inc.

- 6.1.6 Berry Global Inc.

- 6.1.7 Inline Plastics

- 6.1.8 Novolex Holdings LLC

- 6.1.9 Sabert Corporation

- 6.1.10 Silgan Plastic Food Container

- 6.1.11 Bennett Plastics Inc.

- 6.1.12 B&R Plastics Inc. (Gilster-Mary Lee Corp.)

- 6.1.13 Graphic Packaging

- 6.1.14 Amcor PLC

- 6.1.15 Sonoco Products Company

7 LIST OF PACKAGING DISTRIBUTORS AND SUPPLIERS IN THE FOODSERVICE PACKAGING INDUSTRY