PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687470

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687470

RF GaN - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

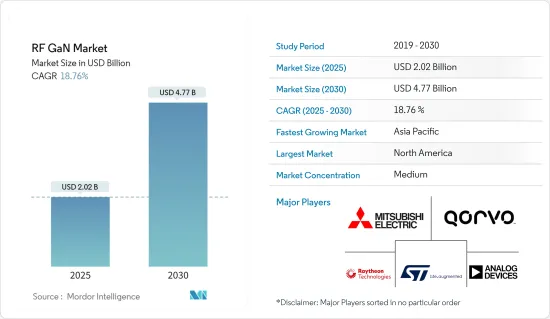

The RF GaN Market size is estimated at USD 2.02 billion in 2025, and is expected to reach USD 4.77 billion by 2030, at a CAGR of 18.76% during the forecast period (2025-2030).

Due to the benefits of RF GaN usage across a wide range of real-time linked devices and applications, more industries are expected to use the Internet of Things (IoT) technology, which is expected to drive market growth. With the continuously evolving GaN technology, GaN enables higher frequencies in more complex applications, such as phased arrays, radar, and base transceiver stations for cable TV (CATV), very small aperture terminal (VSAT), and defense communications.

Key Highlights

- RF GaN plays a key role in wireless infrastructure, improving efficiency and expanding bandwidth to support ever-increasing data transmission speeds. The market for RF GaN is primarily driven by increasing 5G adoption and advances in wireless communications. Telecom operators could also benefit from increased use of GaN power transistors.

- The increasing adoption of RF GaN in electric automotive is also one of the major factors driving demand in this market. Silicon carbide devices are used in the onboard battery chargers of electric buses, taxis, lorries, and passenger cars. Further, increasing government laws favoring the electric vehicles market stimulates demand in the RF GaN market.

- The infrastructure needed to create autonomous vehicles and drones is another factor that increases demand for RF GaN technologies. Hence, growth in the adoption and development of autonomous vehicles and drones for various applications, especially military and defense, is expected to increase further the adoption of RF GaN devices over the forecast period.

- The inherent material advantages of GaN come with some associated manufacturing challenges that include the cost and optimization of device processing and packaging. Other issues include charge trapping and current collapse, which need to be resolved for increased adoption of these devices. Although significant improvements have been made in RF GaN-based devices (performance and yields), there are still some barriers preventing the gallium nitride on silicon carbide (GaN-on-SiC) from entering mainstream applications (i.e., in wireless telecom base-stations or CATV).

- The COVID-19 pandemic impacted supply lines and the telecoms industry. It considerably hindered the penetration of 5G in the telecommunications sector. In this critical situation, consumers are expected to continue using mobile phones, but most of them may not be able to invest more in a technology that is still in a nascent stage.

- Rapidly increasing data consumption has resulted in the growth of commercial networks and is encouraging network providers to adopt next-generation networks, such as 4G and 5G. According to the Cisco Visual Networking Index, global mobile data traffic is expected to register a CAGR of 46%, reaching 77.5 exabytes per month by 2022.

- Organizations across the world are innovating new products and expanding their business. For instance, in June 2022, Integra, a provider of innovative RF and microwave power solutions, announced that it had begun shipping its breakthrough 100V RF GaN technology to customers in the United States and Europe. The company also announced the expansion of its 100V RF GaN product portfolio with the launch of seven new products for the avionics, directed energy, electronic warfare, radar, and scientific market segments, delivering power levels of up to 5kW in a single transistor.

Radiofrequency Gallium Nitride Market Trends

Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- As a primary driver of global digitization and an industry undergoing comprehensive changes in the market environment, the telecommunications industry is regarded as a major user of digital transformation technologies. The telecommunications industry's investment in interoperability and technology has facilitated a paradigm shift in the flow of capital and information throughout the global economy, providing the building blocks for the emergence of entirely new business models across the industry.

- The 5G technology is expected to revolutionize the domain of various broadband services and empower connectivity across different end-user verticals. The major factors boosting the market share of GaN are increasing mobile subscriptions, streaming of online video content, 5G infrastructure, and various IoT applications using 5G. 5G is anticipated to support different services and associated service requirements across multiple scenarios.

- Currently, the number of 5G mobile subscriptions is valued at 0.42 million, and it is expected to reach 400 million subscriptions by 2022. With the substantial growth in the rollouts of 5G technology globally, the demand for RF GaN technology is expected to increase.

- In May 2022, STMicroelectronics (ST) and MACOM Technology Solutions Holdings (MACOM), a supplier of semiconductor products for the telecommunications, industrial, defense, and data center industries, announced the production of RF GaN on silicon (RF Gan-on-Si) prototypes. With this success, ST and MACOM will continue to work together and expand their relationship. GaN-on-Si technology under development by ST and MACOM is anticipated to offer competitive performance and significant economies of scale enabled by integration into standard semiconductor process flows.

- Qorvo is one of the suppliers of RF solutions to the 2G, 3G, and 4G base station manufacturers. It is uniquely positioned in the market to support the development of sub-6 GHz and cmWave/mmWave wireless infrastructure. Qorvo has been investing in product solutions covering relevant 5G bands, such as 3.5, 4.8 and 28, and 39GHz, to service the market, mainly to enable 5G.

- The need for dense, small-scale antenna arrays in 5G infrastructure results in key challenges with power and thermal management in radio frequency (RF) systems. With their improved wideband performance, efficiency, and power density, GaN devices offer the potential for more compact solutions that can address these challenges.

Asia-Pacific is Expected to Experience Significant Growth

- The Asia-Pacific region's discrete semiconductor industry is driven by China, Japan, Taiwan, and South Korea, constituting around 65% of the global discrete semiconductor market. In contrast, others, like Vietnam, Thailand, Malaysia, and Singapore, contribute to the region's dominance in the market.

- According to the Electronics and Semiconductors Association of India,the Indian market for semiconductor components would register a 10.1% CAGR (2018-2025) to reach USD 32.35 billion by 2025. The country is a vital destination for global research and development centers. Therefore, the ongoing 'Make in India' initiative by the Government of India is expected to result in significant investment in the semiconductor market. Such initiatives by the government of India will leverage the RF GaN market.

- In February 2022, Navitas Semiconductor, a provider of GaN integrated circuits (ICs), announced its participation in the China International Capital Corporation Limited (CICC) Investor Conference. The company's proprietary GaN power IC integrates GaN power and GaN drive, control, and protection in a single SMT package. Such participation will leverage the GaN market in the region.

- Demand for RF GaN across the APAC region is expected to increase due to growing investor interest in developing infrastructure to support 5G technology. For instance, according to the GSMA, the Asia-Pacific mobile operator is expected to spend more than USD 400 billion by 2025, of which USD 331 billion will be expended on 5G deployments.

- The growth of RF GaN companies in China is part of a broader trend as the nation shifts from a manufacturing- to an innovation-driven economy. The Chinese market is witnessing an exploding demand for commercial wireless telecom applications, and Chinese companies are already developing next-gen telecom networks.

- Moreover, in December 2021, researchers from IIT Kanpur in India developed a high-performance, industry-standard model of aluminum GaN (AlGaN) high electron mobility transistor (HEMT). This model provides a simple design method that can be used to manufacture high-power RF circuits. RF circuits include amplifiers and switches used in wireless transmissions and are useful in aerospace and defense applications. Constant innovations by researchers will drive the market growth of RF GaN in the region.

Radiofrequency Gallium Nitride Industry Overview

The competitive rivalry among the players in the RF GaN market is high owing to the presence of some key players such as Raytheon Technologies, STM microelectronics, amongst others. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over other players. Through research and development, strategic partnerships, and mergers and acquisitions, these players have been able to gain a strong foothold in the market.

In June 2022, Qorvo, a prominent provider of innovative RF solutions that connect the world, was selected by the US Department of Defense (DoD) to proceed with the Advanced Integration Interconnection and Fabrication Growth for Domestic State-of-the-Art (SOTA) RF GaN program, also known as STARRY NITE, as part of the Office of Undersecretary of Defense Research & Engineering's (OUSD R&E) microelectronics roadmap. The program seeks to develop and mature domestic, open SOTA RF GaN foundries in alignment with the DoD's advanced packaging ecosystem.

In May 2022, STMicroelectronics and MACOM Technology Solutions Holdings Inc., a significant supplier of semiconductor products for the industrial, telecommunications, defense, and data center industries, announced the successful production of RF Gan on Silicon (RF Gan-on-Si) prototypes. With this achievement, ST and MACOM would continue to work together and enhance their relationship.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- 5.1.2 Favorable Attributes Such As High-performance and Small Form Factor to

- 5.2 Market Restraints

- 5.2.1 Cost & Operational Challenges

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Military

- 6.1.2 Telecom Infrastructure (Backhaul, RRH, Massive MIMO, Small Cells)

- 6.1.3 Satellite Communication

- 6.1.4 Wired Broadband

- 6.1.5 Commercial Radar and Avionics

- 6.1.6 RF Energy

- 6.2 By Material Type

- 6.2.1 GaN-on-Si

- 6.2.2 GaN-on-SiC

- 6.2.3 Other Material Types (GaN-on-GaN, GaN-on-Diamond)

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Aethercomm Inc.

- 7.1.2 Analog Devices Inc.

- 7.1.3 Wolfspeed Inc. (Cree Inc.)

- 7.1.4 Integra Technologies Inc.

- 7.1.5 MACOM Technology Solutions Holdings Inc.

- 7.1.6 Microsemi Corporation (Microchip Technology Incorporated)

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Qorvo Inc.

- 7.1.10 STMicroelectronics NV

- 7.1.11 Sumitomo Electric Device Innovations Inc.

- 7.1.12 HRL Laboratories

- 7.1.13 Raytheon Technologies

- 7.1.14 Mercury Systems, Inc

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS