PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644590

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644590

India Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

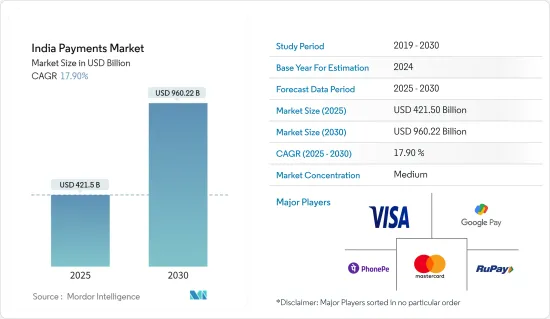

The India Payments Market size is estimated at USD 421.50 billion in 2025, and is expected to reach USD 960.22 billion by 2030, at a CAGR of 17.9% during the forecast period (2025-2030).

Key Highlights

- Shopping for goods and services on the internet, supported by an increasing number of online shoppers in India, is among the primary drivers for the payments market in the country, with payments made online through both UPI transactions and payment cards. The convenience of digital wallets and the emphasis on cashless transactions further fuel the adoption of online payments using cards and digital wallets, supporting market growth.

- However, the expansion of digital payments extends beyond applications integrated with the UPI ecosystem. Payment cards, particularly credit cards, have demonstrated a robust increase in both user adoption and transaction volumes in India. According to the Reserve Bank of India (RBI), ATM withdrawal transactions reached over 826.49 thousand in March 2023, up from 679.82 thousand in March 2022. Furthermore, credit card transactions at point-of-sale terminals rose to 140 million in March 2023, compared to 113 million in March 2022 made via credit cards. This data underscores a significant rise in cash withdrawals via ATMs over the past year.

- The payments market has seen a surge in diverse stakeholders, including wallets, payment service providers (PSPs), FinTechs, and BigTechs, all competing to establish their digital payment platforms. While these new players may not offer the full suite of services traditional banks do, they excel in catering to specific niches, delivering enhanced customer experiences, often at more competitive rates. Furthermore, these entrants face less stringent regulations than banks, translating into significant cost advantages. To attract and retain customers, FinTechs, wallets, and BigTechs often leverage rewards and cashback approaches. This customer-centric approach has not only driven down pricing but also intensified competition in the market.

- Government regulatory support, continuous technical advancements by the National Payments Corporation of India (NPCI), and innovative solutions from an expanding network of payment service providers have significantly increased public interest. There was an increased demand for contactless payments during the COVID-19 pandemic, and the trend continued even as the pandemic receded, indicating a long-standing shift in consumer behavior.

- The pandemic raised the demand for online purchases and cashless transactions due to the closure of physical shops. It transformed consumer buying behavior to go for payment options through digital wallets, which has been supported by the growth of mobile wallets and internet services in all the regions of the country, creating a market growth opportunity for the payment market during the pandemic and post-pandemic period in India.

India Payments Market Trends

Point-of-Sale is Expected to Drive Market Growth

- Merchants and businesses are increasingly deploying new point-of-sale (PoS) terminals, driven by the growing popularity of credit card payments and the need to accommodate various customer payment preferences. However, there is a significant shift toward QR code-based UPI transactions. The emergence of contactless payments, QR code-based payments, and buy now pay later (BNPL) options continuously enhanced the convenience and security of PoS transactions, attracting more users and retailers to adopt these payment terminals to accept payments.

- The growth of e-commerce has established online shopping as a standard practice, with digital payments becoming the primary transaction method. This behavior has also influenced physical retail, where consumers increasingly prefer using digital wallets or cards at the time of payment. According to the Reserve Bank of India (RBI), in May 2024, nearly 298 million point-of-sale transactions were made through debit cards across India, compared to 174.25 million transactions in January 2023.

- Moreover, the mPOS trends in India are improving because of various initiatives of POS companies. For instance, RapiPay established hybrid micro-ATMs that can function as mobile point-of-sale (mPOS) machines. As a result, customers will be able to swipe credit cards in addition to debit cards for any transaction or purchase at a RapiPay station.

- The rising popularity of point-of-sale transactions using digital wallets, cards, and other modes is a key driver of the Indian payments market. Convenience, security, wider customer reach, and government initiatives are fueling this growth, along with continuous advancements in technology and a focus on financial inclusion. As PoS transactions become more seamless and accessible, they are poised to further drive market growth over the forecast period.

Retail Industry Expected to Hold Major Market Share

- As retail sales rise, there is a corresponding increase in the number of transactions. This translates to a higher demand for efficient and secure payment methods, including digital wallets, mobile payments, and point-of-sale (POS) systems. For instance, according to the Retailers Association of India, from June 2022 to June 2023, the retail industry experienced substantial growth across various categories. The food, grocery, and footwear categories experienced the highest sales growth at 15%, while jewelry followed closely with a 14% increase in sales. Furthermore, sports goods witnessed a 13% growth in sales across India.

- The Government of India's initiatives to promote digitalization and cashless transactions are encouraging consumers to move away from cash. This fuels the adoption of digital payment methods within the retail industry. The government launched several initiatives to fuel digital payments in retail, including promoting digital wallets like BHIM and UPI, offering zero-transaction charges for RuPay debit cards and UPI payments, and setting up the Bharat QR code systems. These initiatives have made digital payments cheaper, faster, and more accessible for both consumers and retailers, leading to a significant increase in cashless transactions within India's retail industry.

- Furthermore, the Indian Ministry of Electronics and Information Technology has reported a significant expansion in the retail digital payment industry, which achieved a compound annual growth rate (CAGR) of 50.84% in transaction volume from 2017 to 2023. According to data from the Reserve Bank of India (RBI), it covers retail credit transfers, debit transfers, direct debits, prepaid payment instruments (PPI), and card payments. During the FY 2022-2023, India processed approximately 368.82 million digital transactions daily. Remarkably, by December 2023, the country had already exceeded 100 billion digital transactions for the FY 2023-2024. Several factors aided in market growth, with key contributors being advancements in payment infrastructure, significant progress in information and communications technology, and the implementation of a dynamic regulatory framework.

- The convenience of digital payments has significantly driven their adoption, leading to a surge in customer demand for digital transaction options at offline retail outlets. In response to the cash shortages at ATMs and bank branches following demonetization, many merchants, influenced by their customers' preferences, transitioned to accepting card and QR code payments.

India Payments Industry Overview

The Indian payments market is fragmented due to the presence of several companies. However, a few significant market players, like Paytm, have contributed considerably to the market's growth. There is intense market competition as different players compete to maximize their profits. Payment aggregators are likewise attempting to expand their market share by implementing various measures, including expanding their product line and adopting strategies like acquisitions and partnerships. Some major companies in the payments market are Visa Inc., Mastercard Inc., Phonepe Pvt Ltd (Flipkart Internet Pvt. Ltd), Google Pay (Google LLC), and Rupay.

- June 2024: Hitachi Payment Services obtained final authorization from the Reserve Bank of India (RBI) to operate as an online payment aggregator under the Payments and Settlement Systems Act. This approval allows the company to enhance its digital solutions and services portfolio, offering a comprehensive array of innovative and merchant-friendly payment options, including UPI, net banking, cards, and wallets, along with value-added services such as EMI, pay later, buy now pay later (BNPL), link-based payments, and customized loyalty solutions for merchants.

- May 2024: Paytm Payments Bank (PPBL) moved its bill payment operations to Euronet Services India, a US-based payment technology firm that specializes in managing backend settlement systems for numerous digital payment channels in India after recently switching its retail point-of-sale business to RBL Bank and merchant payment settlement services to Axis Bank.

- May 2024: Amnex Infotechnologies and Mastercard formed a strategic collaboration to develop advanced payment acceptance solutions within the urban mobility industry. This initiative aims to enhance the efficiency and convenience of transit systems. The partnership highlights the mutual commitment of both companies to co-create advanced transit solutions. They plan to implement these innovations across 20 cities in India, beginning with two pilot projects and subsequently extending their efforts to the Middle East and other regions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the Payments Landscape in India

- 4.5 Key Market Trends Pertaining to the Growth of Cashless Transactions in India

- 4.6 Impact of COVID-19 on the Payments Market in India

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Robust Growth of E-commerce and Rise of M-commerce is Expected to Drive the Payments Market

- 5.1.2 Enablement Programs by Key Retailers and Government Encouraging Digitization of the Market

- 5.1.3 Real-time Payments, such as UPI and Buy Now Pay Later to Drive the Indian Payments Market

- 5.2 Market Challenges

- 5.2.1 Higher Rate of Failure in Digital Transactions

- 5.3 Market Opportunities

- 5.3.1 Move Toward Cashless Society

- 5.3.2 New Entrants to Drive Innovation Leading to Higher Adoption

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of Major Case Studies and Use-cases

- 5.6 Analysis of Key Demographic Trends and Patterns Related to the Payments Industry in India (Coverage to Include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income, etc.)

- 5.7 Analysis of the Increasing Emphasis on Customer Satisfaction and Convergence of Global Trends in India

- 5.8 Analysis of Cash Displacement and Rise of Contactless Payment Modes in India

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (Includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (Includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Other Modes of Payment

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (Includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (Includes Mobile Wallets)

- 6.1.2.3 Others (Includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Visa Inc.

- 7.1.2 Mastercard Inc.

- 7.1.3 PhonePe Pvt Ltd (Flipkart Internet Pvt Ltd)

- 7.1.4 Google Pay (Google LLC)

- 7.1.5 Rupay

- 7.1.6 Paytm (One97 Communications Limited)

- 7.1.7 Amazon Pay (Amazon.com Inc.)

- 7.1.8 American Express Company

- 7.1.9 One MobiKwik Systems Limited

- 7.1.10 Freecharge Payment Technologies Pvt. Ltd

8 Investment Analysis

9 Future Outlook of the Market