PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687793

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687793

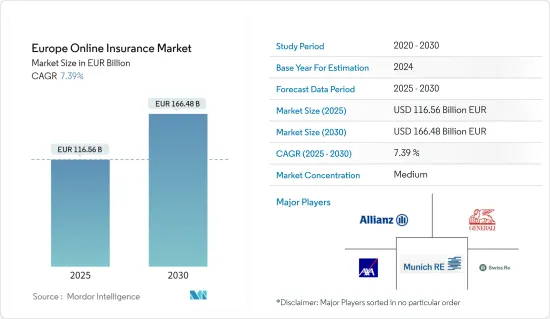

Europe Online Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Online Insurance Market size is estimated at EUR 116.56 billion in 2025, and is expected to reach EUR 166.48 billion by 2030, at a CAGR of 7.39% during the forecast period (2025-2030).

In a business environment that is changing quickly, exploring insurance distribution channels has become more and more important for insurance firms. While the transition to digital has been a natural process for the majority of global companies in recent years, it has not been simple for the insurance sector.

Insurance has always been sold by brokers and agents who know their clients well. It is a trusting relationship, particularly when it comes to life and health insurance. In terms of premiums, more than 99% of life insurance plans are sold in person or through intermediaries. Only the final 1% is sold via other methods, including web aggregators.

Online sales are barely getting started; online sales are prohibited in Bulgaria and are already being partially enforced in the Czech Republic due to COVID-19. Over 80% to 90% of Denmark's sales are made online. Online sales are rising in Estonia. Some businesses only conduct internet sales. Online sales are not seen as a separate channel of distribution in France; they are included with other channels. In Croatia, around 1% of all sales are made online in total.Online sales are possible in Italy and internet sales for cars were 7%. Online sales of non-life products are very widespread in Norway. Online sales in Turkey only account for 2.5% of GWP.

With the growing popularity of price comparison websites among consumers and insurance companies, price comparison website companies are indulging in partnerships and acquisition activities to enrich their market presence and product offerings.

Europe Online Insurance Market Trends

Covid-19 accelerated the Digital insurance

During the COVID-19 crisis, In Insurance sector, chat and videoconference replaced some of the traditional face-to-face interactions between clients and their intermediaries. And, while personal contact remains important.

While only 22% of Belgian brokerage offices is leveraging software or InsurTech applications to work more efficiently, a growing number of comparison websites is helping brokers develop an offering that better matches client needs.

Brokerage firms are becoming increasingly paperless, with two-thirds of them claiming to have already reached this goal.

Rising Numbers of Insurtech Funding

In 2021, European insurtech funding reached an all-time high, with around EUR 2.5 billion invested through 92 deals.

The ecosystem is maturing so that the average deal size jumped from ~EUR 8 million in 2020 to EUR 28 million in 2021 That's also related to mega-rounds (tickets over EUR 100 million) announced across Europe. Most of them were disclosed in the first half of the year: Zego and BoughtByMany in the UK, Wefox in Germany, and Alan and Shift Technology in France. Only one happened in H2 2021: EnvelopRisk in the UK.

Europe Online Insurance Industry Overview

The report covers the major international players operating in the European online insurance market. In terms of market share, the major traditional players are currently partnering with technological companies to gain competitive advantage in the market studied. However, they face stiff competition from mid-size and smaller insurtech companies, which focus on disrupting the market studied by offering tailored solutions. Some of the major Companies includes Allianz Se, Assicurazioni Generali, Axa Sa, Munich Re among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Study Deliverables

- 2.2 Study Assumptions

- 2.3 Analysis Methodology

- 2.4 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Market Opportunities

- 4.5 Industry Value Chain Analysis

- 4.6 Insights into Latest Technological Innovations and Recent Trends in the Market

- 4.7 Insights on Government Regulations in the Industry

- 4.8 Porters Five Force Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Insurance Type

- 5.1.1 Life Insurance

- 5.1.2 Non-life Insurance

- 5.2 By Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Allianz SE

- 6.2.2 Assicurazioni Generali SpA

- 6.2.3 AXA SA

- 6.2.4 Munich RE

- 6.2.5 Swiss Re AG

- 6.2.6 Aviva

- 6.2.7 Zurich Insurance*

7 MARKET OPPORTUNTIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US