Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693978

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693978

North America Cat Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 297 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

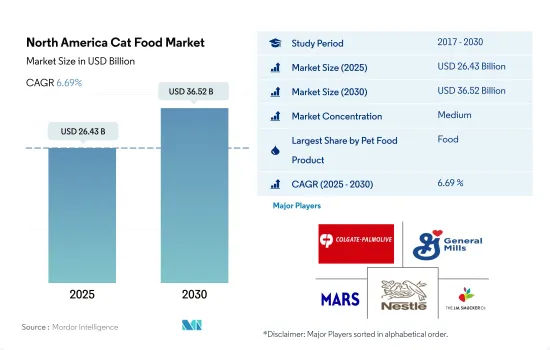

The North America Cat Food Market size is estimated at 26.43 billion USD in 2025, and is expected to reach 36.52 billion USD by 2030, growing at a CAGR of 6.69% during the forecast period (2025-2030).

The availability of a strong distribution network and a wide range of cat food brands is driving the market

- In North America, the value of the cat food market reached USD 21.14 billion in 2022, making it the largest market for cat food in the world. This is due to the substantial cat population and the significant spending on cats by their owners.

- In North America, pet food held the largest market share, with a market value of USD 15.57 billion in 2022. Among pet food, wet food represented the majority share of 52.5% by value in 2022, while dry food accounted for 47.5%. The large share of pet food can be attributed to the multiple benefits of pet food and the availability of a wide range of dry and wet food choices in both mainstream and niche brands, which is driving the overall growth of the pet food market for cats in the region.

- The treats segment is the second-largest segment in the cat food market in North America; it was valued at USD 2.56 billion in 2022. Among cat treats, freeze-dried and crunchy treats are the primary segments, accounting for major shares of 24.9% and 22.3% by value, respectively, in 2022. The use of various ingredients and the presence of added vitamins, minerals, and other supplements in these treats are estimated to drive the growth of this segment in the cat food market.

- The veterinary diets segment is the fastest-growing segment in the cat food market. It witnessed an 81.8% increase between 2017 and 2022, reaching USD 2.42 billion in 2022. The increasing usage of veterinary diets as preventative care is estimated to drive the segment at a faster CAGR of 9.1% during the forecast period.

- The growing availability of various forms of pet food through different distribution channels is estimated to drive the growth of the cat food market during the forecast period.

The United States dominated the cat food market in the region with more than an 88% share in 2022

- North America accounted for the largest share of the global cat food market in 2022, with a value of around USD 21.14 billion. The United States and Canada are the major contributors to the cat food market in North America, with a high demand for pet food products due to the high pet ownership rates in these countries.

- The North American cat food market is dominated by the United States, which accounted for a market value of USD 18.69 billion in 2022. This can be attributed to several factors, including the large population of pet cats in the country, which was estimated to be over 64.6 million in 2022. Additionally, the country's high standard of living and disposable income also play a role, allowing pet owners to allocate a greater portion of their budget toward their cats' food and care products.

- The cat food market in Canada is experiencing significant growth due to the growing population of cats compared to dogs in the country. The cat population grew by 1.7% between 2017 and 2022, reaching a total of 8.2 million. As a result, the Canadian cat food market reached a value of USD 1.66 billion in 2022, representing 36.7% of the Canadian pet food market value in the same year.

- The cat food market is experiencing rapid growth in Mexico and countries in the Rest of North America, which are projected to record CAGRs of 7.2% and 9.9%, respectively, during the forecast period. This can be attributed to the growing cat population in these countries. For instance, in the Rest of North America, the cat population increased by 23.4% between 2017 and 2022, reaching a total of 16.7 million in 2022.

- The growing cat population and the increasing awareness about the benefits of feeding pet foods are estimated to drive the market during the forecast period.

North America Cat Food Market Trends

Increasing adoptions from young adults and millennials are driving the cat food market

- There is an increase in the adoption of cats as pets in North America, owing to the high demand for companionship and less expenditure on pet food for cats than dogs. In the region, cats as pets increased by 13.6% between 2017 and 2022 due to the rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, households owning a cat as a pet was 26% in 2020, which increased to 53.5% in 2022.

- The United States, Canada, and Mexico witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials were 33% of pet parents in the United States, and in 2020, 40% of the cat pet population was adopted from animal shelters in the country. Additionally, pet parents purchased cats from pet stores due to high income. For instance, in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in the region increased by 5.34% between 2020 and 2022.

- Young cats are being adopted more than adult cats in the region, with the United States leading in terms of that number. For instance, in 2021, the adopted cat population in the United States was 684,144, and young cats accounted for 53.5% of the cats adopted. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet food products during the forecast period. An increase in the adoption and purchase of cats and an increase in pet humanization are expected to help in the growth of the pet population. The increasing pet population will help in the growth of the pet food market in the region.

The surging demand for premium cat food products is driving the market

- Pet expenditure is increasing in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. In North America, cat owners prefer to provide their pets with premium pet food and are willing to adopt eco-friendly pet care products. For instance, in 2022, more than 50% of pet parents were willing to provide their pets, including cats, with eco-friendly pet care products by paying a premium price; 42% of cat owners provided cats with premium pet food.

- The highest expenses of pet parents are on pet food and treats, which are estimated to increase during the forecast period. For instance, cat food and snacks accounted for 22.7% of expenses incurred for cats in the United States in 2022. The share is projected to increase as more pet parents treat their pets as family members and the awareness about specialized pet food increases. Cat parents are willing to provide their cats with natural pet food and treats as a high number of millennials are pet parents in the region.

- Pet parents are also investing in other services such as pet insurance, pet grooming, and pet training for socialization. Pet parents are getting their cats insured as emergency veterinary care can be very expensive. This is evident as pet parents, including cat parents, in the United States invested USD 2 billion in pet insurance in 2020, an increase of 27.5% from the previous year; 17% of the cat population was insured in 2020.

- Premiumization and rising awareness about the benefits of quality food are factors anticipated to help in increasing pet expenditure in the region.

North America Cat Food Industry Overview

The North America Cat Food Market is moderately consolidated, with the top five companies occupying 55.47%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and The J. M. Smucker Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50001460

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 General Mills Inc.

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 PLB International

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 The J. M. Smucker Company

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.