Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693918

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693918

Europe Military Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 139 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

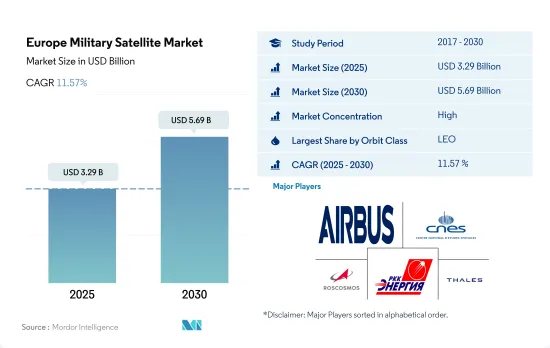

The Europe Military Satellite Market size is estimated at 3.29 billion USD in 2025, and is expected to reach 5.69 billion USD by 2030, growing at a CAGR of 11.57% during the forecast period (2025-2030).

LEO satellites are driving the market's growth and occupies a significant share of 84% in 2029

- There is a growing need for secure and resilient communication systems to support military operations. European countries are investing in military satellite systems that offer enhanced encryption capabilities and protection against cyber threats. These systems ensure reliable and secure communication channels for command and control, intelligence gathering, and coordination among military forces.

- At launch, a satellite or spacecraft is usually placed in one of several special orbits around the Earth, or it can be launched during interplanetary travel. There are three types of Earth orbits, namely, geostationary orbit (GEO), medium Earth orbit, and low Earth orbit. Many weather and communications satellites tend to have high Earth orbits farthest from the surface. Medium Earth orbit satellites include navigational and specialized satellites that are designed to monitor a specific area. Most science satellites, including those, are in low Earth orbit.

- The different satellites manufactured and launched in this region have different applications. For instance, during 2017-2022, out of the 16 satellites manufactured and launched in MEO, most were built for navigation/global positioning purposes. Similarly, out of the 14 satellites in GEO, most were deployed for communication and Earth observation purposes. European organizations owned around 500+ LEO satellites that were manufactured and launched during the historical period.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive demand for space sensors in the European satellite launch vehicle market during the forecast period. During 2023-2029, the market is expected to surge by 104%.

Europe Military Satellite Market Trends

The rising demand for satellite miniaturization in Europe is boosting the market

- Miniature satellites leverage advances in computation, miniaturized electronics, and packaging to produce sophisticated mission capabilities. As the microsatellites can share the ride to space with other missions, they considerably reduce launch costs.

- The demand from Europe is primarily driven by Germany, France, Russia, and the United Kingdom, which manufacture the largest number of small satellites annually. Though the launches from the region have decreased over the last three years, a huge potential lies in the region's industry. The ongoing investments in the startups and the nano and microsatellite development projects are also expected to boost the revenue growth of the regional market. On this note, from 2017 to 2022, more than 50 nano and microsatellites were placed into orbit by various players in the region.

- Companies are focusing on cost-effective approaches to produce these satellites on a large scale to meet the growing demand. The approach involves the use of low-cost industrial-rated passives at the development and design validation stages. The miniaturization and commercialization of electronic components and systems have driven market participation, resulting in the emergence of new market players that aim to capitalize on and enhance the current market scenario. In August 2021, France launched the BRO satellite into LEO. These nanosatellites can locate and identify ships worldwide, providing tracking services for maritime operators and helping security forces. The country plans to build a fleet of 20-25 nanosatellites by 2025.

The surge in investment opportunities is expected to boost the Europe military satellite market

- European countries are recognizing the importance of various investments in the space domain. They are increasing their spending in areas such as Earth observation, satellite navigation, connectivity, space research, and innovation to stay competitive in the global space industry. On this note, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. The ESA is requesting its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In September 2022, the French government announced that it was planning to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years. In November 2022, Germany announced that about EUR 2.37 billion were allocated, including about EUR 669 million for Earth observation, about EUR 365 million for telecommunications, EUR 50 million for technology programs, EUR 155 million for space situational awareness and space security, and EUR 368 million for space transport and operations.

- The UK government has planned a USD 7.5 billion upgradation of the satellite telecommunication capabilities of the armed forces. In July 2020, the UK Ministry of Defence (MoD) awarded a USD 630 million contract to Airbus Defence and Space for constructing a new telecommunications satellite as a stopgap to bolster military capabilities ahead of the introduction of a new generation of spacecraft that is scheduled to start entering service by 2025. Under the terms of the contract, the fully indigenous satellite will be based on Airbus' Eurostar Neo spacecraft.

Europe Military Satellite Industry Overview

The Europe Military Satellite Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Airbus SE, Centre National D'etudes Spatiales (CNES), ROSCOSMOS, RSC Energia and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50000972

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Russia

- 4.4.4 United Kingdom

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Satellite Mass

- 5.1.1 10-100kg

- 5.1.2 100-500kg

- 5.1.3 500-1000kg

- 5.1.4 Below 10 Kg

- 5.1.5 above 1000kg

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 Satellite Subsystem

- 5.3.1 Propulsion Hardware and Propellant

- 5.3.2 Satellite Bus & Subsystems

- 5.3.3 Solar Array & Power Hardware

- 5.3.4 Structures, Harness & Mechanisms

- 5.4 Application

- 5.4.1 Communication

- 5.4.2 Earth Observation

- 5.4.3 Navigation

- 5.4.4 Space Observation

- 5.4.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Centre National D'etudes Spatiales (CNES)

- 6.4.3 GomSpaceApS

- 6.4.4 ROSCOSMOS

- 6.4.5 RSC Energia

- 6.4.6 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.