PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639433

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639433

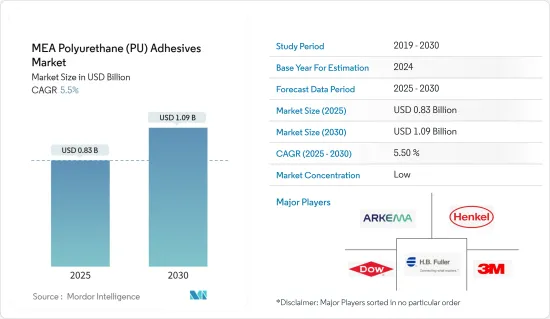

MEA Polyurethane (PU) Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The MEA Polyurethane Adhesives Market size is estimated at USD 0.83 billion in 2025, and is expected to reach USD 1.09 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The COVID-19 outbreak negatively impacted the market. Stoppage or slowdown of several industrial projects, movement restrictions, production halts, and labour shortages led to a decline in the polyurethane (PU) adhesives market growth. However, it recovered significantly in 2021, owing to rising consumption from various end-use industries, including building and construction, packaging, healthcare, and automotive.

Key Highlights

- Over the short term, increasing demand from the construction industry and healthcare infrastructure are some of the major factors driving the studied market's growth.

- Conversely, stringent environmental regulations regarding VOC emissions are expected to hinder the studied market's growth.

- However, shifting focus towards bio-based adhesives and growing inclination towards manufacturing lightweight products will likely offer opportunities for the PU adhesives market.

- Saudi Arabia dominates the Middle East and Africa PU adhesives market and will also witness the highest CAGR during the forecast period.

MEA Polyurethane (PU) Adhesives Market Trends

Building and Construction Industry Dominates the Market

- Among end-user industries, the building and construction segment dominates the consumption of PU adhesives in the region.

- PU adhesives include rapid curing and low-strength properties, making them an excellent choice for woodworking and other construction applications. They provide the high strength required to hold construction materials together.

- Besides, this material is versatile when it comes to product assembly adhesives. It suits plastics, glass, PVFs, aluminum, stainless steel, and other metals, regardless of the toughness of bond substrates.

- Countries such as Saudi Arabia, Kuwait, Qatar, United Arab Emirates, and Egypt is witnessing strong growth in construction investments and activities. For instance, the sustainable living environment axis in Kuwait Vision 2035 includes five pillars, the most prominent of which is to provide housing care to citizens through what is planned. It is to ensure the provision of 65.5 thousand housing units through five projects costing about KWD 3.22 billion (USD 10.5 billion), the last of which ends by 2029.

- When these projects are implemented, the state will meet approximately 72% of the current housing requests, which are 91,000. The first project of the residential care plan revolves around the vision of Kuwait 2035 (New Kuwait) in the city of Jaber Al-Ahmad, which includes a completion rate of 95% and will complete at the end of 2022. The second project is in Al-Mutla'a, with a completion rate of 64%, to be completed by the end of 2023.

- The third project is in the suburb of South Abdullah Al-Mubarak, which contains a completion rate of 72% and will be completed by the end of 2025. The completion rate in the fourth project, the South Sabah Al-Ahmad, is about 14%, as it is still in the preparation stage and is expected to be completed in 2029. This south of Saad Al-Abdullah includes a completion rate of 13% as it is still in its preparatory phase and ends in 2029. Therefore, the growing residential housing construction in Kuwait is expected to create an upside demand for Kuwait's polyurethane(PU) adhesives market.

- Hence, the growth prospects for the construction industry in such countries are expected to propel the consumption of PU adhesives in the region.

Saudi Arabia to Dominate the Market

- Saudi Arabia holds the largest Middle East and African market share for polyurethane (PU) adhesives. The demand for polyurethane (PU) adhesives is expected to rise throughout the forecast period due to rising investments in construction, healthcare infrastructure, and the efforts to develop automotive hubs in the country. The rise in the population and disposable income increased the demand for better-quality residential building development.

- The Saudi Arabian construction market is expected to witness significant growth and offer lucrative potential due to its Vision 2030, NTP 2020, and several ongoing reforms to diversify away from oil. Vision 2030, NTP 2020, the private sector investment boost, and the ongoing reforms are expected to be the growth drivers for the Saudi polyurethane adhesives market from the country's construction industry during the forecasted period.

- Moreover, under Vision 2030, 80 new hotels with more than 11,000 luxurious rooms will be opened across Saudi Arabia by 2030. Therefore, increasing investments in the construction of hotels is expected to create demand for the polyurethane (PU) adhesives market.

- The country's economy is entering a post-oil era in which the kingdom's mega-cities, which are under construction, will provide future growth. According to industry sources, more than 5,200 construction projects are ongoing in Saudi Arabia at a value of USD 819 billion. These projects account for approximately 35% of the total value of active projects across the Gulf Cooperation Council (GCC).

- Some major urban construction projects in Saudi Arabia include the King Abdullah Security Compounds (Phase 5) and the Grand Mosque (Holy Haram Mosque expansion). Each of these is valued at USD 21.3 billion and developed by the Ministry of Municipalities and Rural Affairs in Makkah.

- The top construction projects in Saudi Arabia include Neom, the Red Sea Project, Qiddiya entertainment city, Amaala, Jean Nouvel's Sharaan resort in Al-Ula, Makkah Grand Mosque - Third Expansion, Jeddah Tower, Ministry of Housing's Sakani Homes, Jabal Omar, Al Widyan, and Riyadh Metro. It also includes Riyadh Rapid Bus Transit System, King Fahd Medical City Expansion, King Abdullah Bin Abdulaziz Medical Complexes, King Salman Energy Park (Spark), Saudi Aramco's Berri and Marjan, Hanergy Solar Park, Dumat Al Jandal Wind Power Plant, Saudi Aramco-Total's PIB factory, and Pan-Asia bottling facility.

- Saudi Arabia's Amid Vision 2030 is a significant development plan supported by megaprojects to grow the nation's infrastructure. With an emphasis on environmental commitments, enhancing citizen quality of life, and creating a strong economy, Vision 2030 aspires to bring about change. Investments in several fields, including healthcare, education, and infrastructure, expanded due to the introduction of Vision 2030 and the corresponding National Transformation Plan (NTP).

- Many residential and commercial projects are being launched in Saudi Arabia, which is anticipated to increase the country's construction activity. Some of these projects are the USD 500 billion futuristic mega-city "Neom" project and the Red Sea Project Phase 1 (due for completion in 2022), which includes 14 luxurious and hyper-luxury hotels that may total 3,000 rooms spread across five islands. It also includes two inland resorts, Qiddi Entertainment City, Amaala - the luxurious wellness tourism destination, Jean Nouvel's Sharaan resort in Al-Ula, the Ministry of Housing's Sakani homes, and Jeddah Tower.

- According to the Gulf Council Corporation, Saudi Arabia planned to invest USD 66.49 billion in healthcare facilities, with help from the private sector, whose participation is expected to rise by 65% by 2030.

- Saudi Arabia is focusing on establishing itself as the new automotive hub in the Middle East. Though the country is a large importer of vehicles and auto parts, it is now trying to attract original equipment manufacturers (OEMs) to open their production plants in the kingdom to develop the domestic auto industry. For instance, several OEM manufacturers such as Renault, Peugeot, and Volkswagen already set up units in Morocco, and major automotive manufacturers see Morocco as a cost-effective country.

- The healthcare industry in Saudi Arabia accounts for the largest expenditure in the GCC region, and there is a rising demand for increasing hospital and long-term care centers. Saudi Arabian Government aims to increase private sector contribution from 40% to 65% by 2030, targeting the privatization of 290 hospitals and 2,300 primary health centers.

- Hence, all such trends are expected to drive the consumption of the polyurethane adhesives market in the country during the forecast period.

MEA Polyurethane (PU) Adhesives Industry Overview

The Middle East and African polyurethane (PU) adhesives market is highly fragmented. Some of the major players in the market include 3M, Arkema, Dow, H.B. Fuller, and Henkel AG & Co. KGaA, amongst others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Robust Growth of Construction Industry

- 4.1.2 Growing Healthcare Infrastructure

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Resin Type

- 5.1.1 Thermoset

- 5.1.2 Thermoplastic

- 5.2 Technology

- 5.2.1 Water Borne

- 5.2.2 Solvent-borne

- 5.2.3 Hot Melt

- 5.2.4 Other Technologies

- 5.3 End-user Industry

- 5.3.1 Automotive and Aerospace

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Footwear and Leather

- 5.3.5 Healthcare

- 5.3.6 Packaging

- 5.3.7 Other End-user Industries

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 South Africa

- 5.4.5 Egypt

- 5.4.6 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Dow

- 6.4.5 Dymax

- 6.4.6 Franklin International

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat AG

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Sika AG

- 6.4.14 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Towards Bio-Based Adhesives

- 7.2 Growing Inclination Towards Manufacturing of Lightweight Products