PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692507

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692507

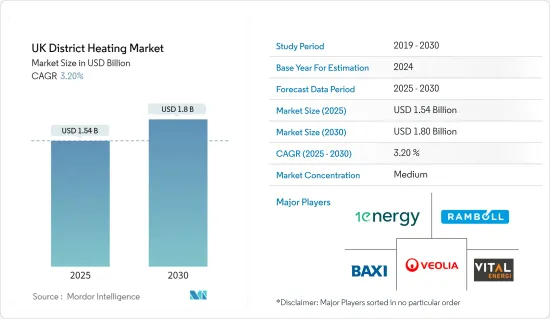

UK District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The UK District Heating Market size is estimated at USD 1.54 billion in 2025, and is expected to reach USD 1.80 billion by 2030, at a CAGR of 3.2% during the forecast period (2025-2030).

Key Highlights

- To meet the Sustainable Development Scenario (SDS), clean heating technologies, such as district heating, heat pumps, and renewable and hydrogen-based heating, are expected to increase the sales of district heating networks, positively influencing market demand.

- The rising demand for energy-efficient heating solutions is pushing for the adoption of new technologies. As per the UK government's research, 14-20 percent of the heat demand in the United Kingdom is expected to be met by heat networks by 2030 and 43 percent by 2050. Around half of the energy consumed in the United Kingdom is used as heat. The commercial, domestic, and public sectors accounted for two-thirds of the final energy consumption. Heat is primarily used for water and space heating in residential/domestic and commercial buildings.

- The fifth generation is emerging as a new system to replace the existing fourth-generation district heating system. 5th generation district heating & cooling systems are bi-directional, decentralized, close-to-ground temperature networks that use the direct exchange of cold and warm thermal storage and return flows to balance the thermal demand in full measure.

- Several government-led initiatives to expand the heat networks in the country also create a favorable outlook for the growth of the studied market. For instance, in late 2022, the UK Government announced GBP19.1 million (USD 23.8 million) funding that came from the government's GBP320 million (USD 399 million) Heat Networks Investment Project (HNIP), aimed at supporting heat networks across England and Wales.

- However, district heating systems are more capital-intensive as compared to alternatives in the market. The DHC system requires a network of trenches and continuous maintenance of pumps and systems. These factors hinder the demand for DHC systems.

- Furthermore, it becomes difficult and costly to install distribution pipes for district heating in pre-existing cities/buildings that were not planned for such features, thereby adding complexity to the installation process, which continues to remain among the major challenging factors for the growth of the studied market.

UK District Heating Market Trends

Rising Urbanization and Industrialization to Drive the Market

- Rapid urbanization across the world, including in the UK, is driving the demand and pushing the switch to renewable energy sources for centralized heating & cooling, which can help reduce CO2 emissions, improve efficiency, increase urban energy needs, and provide cost-effective temperature control. For instance, driven by urbanization, the United Kingdom has rapidly increased its use of centralized systems in its northern regions.

- In the United Kingdom, urbanization amounted to 84.39% in 2022, as per the World Bank. This presents almost a three percentage point increase over the past decade. Though slow, the upward trend has been consistently positive, significantly influencing the market growth.

- Considering the prominence of cold weather conditions, the UK commands a prominent share of the global demand for DHC solutions, and a major share of the distribution network is situated in urban areas in the region. Large heat distribution infrastructures were developed during the second half of the 20th century in the region. These remain the principal ways to provide energy for space and water heating in urban areas.

- District energy systems benefit from and support this environment and are inherently appropriate to urban landscapes. The technology's synergy with the environmental conditions and the working population's needs are well suited for urban demographics. The growth of urban centers facilitates the construction of district networks. England, London, Wales, and Nottingham are some of the best examples in the market. In addition to requiring a particular scale of development, the high capital costs of heat networks demand energy services be delivered in the tightest space possible to maximize the number of end users. Thus, dense urban developments are highly suitable for distributed heat provision.

Residential and Domestic Segment Holds Significant Market Share

- Domestic heating accounts for nearly 14 percent of all emissions in the United Kingdom (according to the Institute for Government) and needs to be tackled urgently in line with the government's aim to meet its carbon reduction targets. District heating offers an effective solution for the supply of low-carbon heat to homes across the United Kingdom. While just over 2 percent of residences in the United Kingdom are currently connected to a district heating network (as per Energy Saving Trust), more are expected to come online as the country transitions to net zero over the coming decades.

- Most district heating systems currently installed in the United Kingdom use a gas-powered combined heat and power system (CHP), which generates electricity. A single CHP is usually more efficient in a housing estate or block of flats and requires less maintenance than a gas-powered boiler in every flat or house. The UK government's Committee for Climate Change (CCC) estimates that around 12 percent of domestic heat will be supplied by district heating by 2050.

- There are over 17,000 heat networks in place in the United Kingdom, and around half a million connections to them, most of them being domestic customers (as per Energy Saving Trust). They are perceived as a particularly attractive option in dense urban areas. They are an effective way of dealing with fuel poverty while reducing housing management costs.

- The establishment of heat networks, which can vary widely in size, implies that cheaper, lower-carbon sources of heat generation can be added over time without abrupt changes, such as digging up roads or changing people's homes. Hence, the growing efforts to reduce the carbon footprint of the residential sector will support the studied market's growth. For instance, according to sources like the UK Department for Business, Energy and Industrial Strategy, carbon dioxide emission from the residential real estate sector in the United Kingdom is anticipated to reach 68 million metric tons by 2040.

- Furthermore, the Future Homes Standard, expected to be introduced in the United Kingdom in 2025, requires carbon emissions produced by new homes to be around 75-80 percent lower than those built to current standards. Houses will have to be 'zero carbon ready,' with no retrofit work needed to benefit from the electricity grid's decarbonization and the heating's electrification. Fossil fuel heating may be banned in new houses, with an expected shift toward low-carbon heating technologies, such as heat networks.

UK District Heating Industry Overview

The UK district heating market is moderately competitive, with the presence of major players like Vital Energi, 1 Energy Group Limited, Baxi Heating UK, Ramboll UK Limited, and Veolia Environnement SA. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In May 2023, the UK Government awarded government funding to 7 state-of-the-art heat network projects across England, which includes the UK's first system drawing heat from underground, with the potential of providing low-cost heating for nearly 4,000 homes. According to the government, the identified projects will receive a share of GBP 91 million (USD 113.6 million) from the government's Green Heat Network Fund.

In April 2023, Utility company Pinnacle Power entered an agreement with DIF Capital Partners to build and deploy GBP 1 billion (USD 1.25 billion) worth of low-carbon heat networks across the UK. The new partnership between the companies will accelerate the deployment of "town-and-city-scale heat networks" that will likely help to decarbonize several homes and buildings across the country.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Analysis

- 4.3 Impact of Macroeconomic Scenarios on the Market

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Intensity of Competitive Rivalry

- 4.4.5 Threat of Substitutes

- 4.5 Industry Supply Chain Analysis

- 4.6 Government Initiatives and Programs

- 4.7 District Heating Contracts/Live Tenders

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Challenges

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Residential/Domestic

- 6.1.2 Non-domestic

- 6.2 Current Energy Mix of Heat Networks and Future Trends

- 6.3 Heat Network Connections by Sectors and Customers

- 6.4 Thermal Storage Usage and Future Potential

- 6.5 Heat Networks Density Based on Regions

- 6.6 Consumer Attitudes to Heat Networks

- 6.7 Opportunities for Heat Network

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vital Energi Utilities Ltd.

- 7.1.2 1Energy Group Limited

- 7.1.3 Baxi Heating UK

- 7.1.4 Ramboll UK Limited

- 7.1.5 Veolia Environnement SA

- 7.1.6 Sweco UK (AWECO AB)

- 7.1.7 Vanttenfall (Vattenfall AB)

- 7.1.8 Equans Services Limited

- 7.1.9 E.ON PLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET