PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910441

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910441

Dynamic Random Access Memory (DRAM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

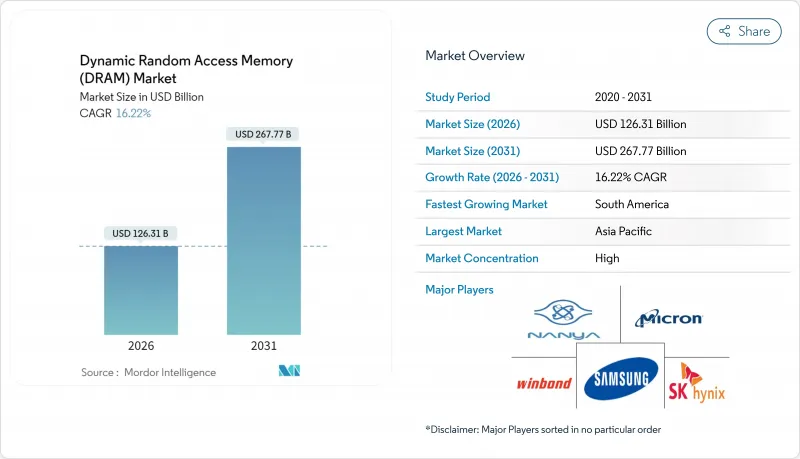

The Dynamic Random Access Memory market was valued at USD 108.68 billion in 2025 and estimated to grow from USD 126.31 billion in 2026 to reach USD 267.77 billion by 2031, at a CAGR of 16.22% during the forecast period (2026-2031).

Accelerated adoption of AI-centric servers, the steep ramp-up of high-bandwidth memory, and tighter automotive qualification requirements have shifted purchasing criteria from capacity alone to a balanced focus on bandwidth, power, and thermal performance. Hyperscale cloud operators began refreshing racks with DDR5 and HBM3E modules during 2024, while handset OEMs in Asia moved much of their flagship and mid-tier portfolios to LPDDR5X, collectively keeping fab utilization above 95% through mid-2025. Memory content per electric vehicle rose quickly as zonal architectures replaced traditional ECU networks, pushing automotive DRAM demand into multi-gigabyte territory. At the same time, supply allocation conflicts between lucrative HBM3E and legacy DDR4 lines triggered price surges that reshaped cost-performance trade-offs for PCs, smartphones, and industrial IoT boards.

Global Dynamic Random Access Memory (DRAM) Market Trends and Insights

Ascending content footprint of AI and generative-AI workloads in hyperscale data centers

NVIDIA's 2025 Blackwell GP-AI platforms established bandwidth baselines that eclipsed conventional DDR architectures, lifting average server memory from 256 GB in 2024 to multi-terabyte deployments by mid-2025. With each HBM3E stack delivering more than 1 TB/s, cloud operators re-architected racks around memory-centric topologies. Samsung delivered production-ready CXL 2.0 DRAM that allowed Azure and other providers to pool memory across hosts, improving utilization while deferring capex on additional compute nodes. Suppliers consequently shifted wafer starts from DDR4 to HBM, triggering tightness in legacy grades but accelerating profit growth in the premium segment.

Soaring LPDDR adoption in 5G flagship and mid-tier smartphones across APAC

Micron's 1Y LPDDR5X samples running at 9,200 MT/s reached handset makers in Q1 2025, cutting power by 20% and raising baseline configurations in Chinese and Indian models from 8 GB to 12 GB RAM. Xiaomi, OPPO, and emerging brands such as Transsion are locked in forward contracts that consume a growing slice of APAC fab capacity, forcing suppliers to juggle commitments between mobile and datacenter lines. The shift gave LPDDR a steeper growth curve than any other mobile memory since LPDDR4 entered mass production in 2015.

Supply-demand cyclicality driving extreme ASP volatility

High-margin HBM pull-ins persuaded fabs to postpone DDR4 runs early in 2025, igniting a 50% spot-price jump for mainstream modules in May. DDR5 contracts also climbed 15-20%, prompting OEMs to re-engineer product bills of materials or over-order to hedge against further spikes. The feedback loop amplified volatility and cut visibility for production planning, knocking two-plus points from the Dynamic Random Access Memory market's forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Automotive zonal and domain controllers migrating from NOR to high-temperature DRAM

- Edge-AI and industrial IoT boards requiring extended-temperature DRAM modules

- Yield-erosion challenges below 10 nm EUV nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DDR5 accounted for a minimal share of the Dynamic Random Access Memory market in 2025, yet carried the fastest 29.1% forecast CAGR, underpinned by JEDEC's JESD79-5C update that lifted performance ceilings to 8,800 Mbps. That technical leap allowed tier-1 cloud builders to run mixed DDR5-HBM3E configurations that doubled per-socket effective bandwidth. Micron's 1Y DDR5 reached 9,200 MT/s in February 2025, a milestone that pushed server OEMs to pull forward platform refreshes. Meanwhile, DDR4 retained a 44.78% Dynamic Random Access Memory market share through 2025 because corporate IT budgets still favoured cost-optimized configurations. Legacy DDR3 and DDR2 footprints continued to shrink as industrial and automotive design-ins migrated to newer standards.

Suppliers confronted a balancing act: every wafer reassigned to DDR5 meant fewer DDR4 chips for PCs, driving cost spikes that flowed downstream to notebook assemblers in China. Holders of long-tail inventory exploited arbitrage trading, unloading stockpiled DDR4 at premiums unseen since 2017. JEDEC's new CAMM2 form factor removed the height constraints of SO-DIMMs, letting laptops and edge servers adopt denser single-sided stacks. Those packaging gains fed into the Dynamic Random Access Memory market's momentum toward higher-bandwidth norms across consumer and enterprise devices.

The 19 nm-10 nm bracket held 41.85% of the Dynamic Random Access Memory market size in 2025 and is projected to grow 24.4% through 2031 as suppliers squeeze additional dies per wafer without plunging into the yield-risk chasm of sub-10 nm. EUV-enabled 1Y production began shipping revenue units in Q1 2025, but line yields remained at least eight points below mature 1z lines. Consequently, many device makers renewed agreements for 1z and 1y grades to buffer cost risk, giving mid-node processes a volume boost.

SK Hynix laid out a vertical-gate DRAM roadmap that promises wafer-level stacking beyond 2027, signalling the long-term pivot from lateral scaling to 3D architectures. Each successive planar shrink delivers less than 12% cost reduction after mask set, materials, and depreciation are factored in, nudging fabs to look for structural redesigns rather than geometrical shrink alone. Cost sensitivity in mobile and consumer electronics kept >=20 nm nodes alive for price-focused SKUs, ensuring a stratified production mix that diversified fab output and underpinned overall revenue resiliency.

Dynamic Random Access Memory Market is Segmented by Architecture (DDR2 and Earlier, DDR3, DDR4, DDR5, LPDDR, and GDDR), Technology Node (>=20 Nm, 19 Nm-10 Nm, and <10 Nm), Capacity (<=4 GB, 4-8 GB, 8-16 GB, and >=16 GB), End-Use Application (Smartphones and Tablets, Pcs and Laptops, Servers and Hyperscale Data Centers, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific retained a 30.88% revenue position in 2025 on the strength of fabs clustered across South Korea, Taiwan, and mainland China. South Korean suppliers pledged KRW 120 trillion (USD 84 billion) for capacity build-outs through 2028, a figure intended to safeguard leadership in both HBM and traditional DRAM production. Taiwan's contract assembly houses, meanwhile, expanded advanced packaging lines to service rising HBM4 demand, leveraging front-end know-how from logic nodes to introduce Through-Silicon-Via innovations that reduce thermal resistance.

North America formed the largest consumption market as hyperscale builders accelerated rack refreshes and automakers in the United States integrated zonal controllers. Micron secured USD 6.1 billion CHIPS Act funding to construct a new megafab, a move aimed at de-risking geopolitical exposure and shortening lead times for domestic clients. Europe maintained a technology focus on automotive and industrial applications, with German OEMs insisting on extended temperature and longevity guarantees that fetched premium pricing.

South America is forecast to grow at a 21.6% CAGR as Brazil, Argentina, and Mexico nurture electronics assembly ecosystems to localize supply. Policy incentives cut import tariffs on memory components assembled domestically, creating modest but meaningful shifts in sourcing strategies. The Middle East and Africa displayed mid-single-digit growth anchored by data-center build-outs in Gulf Cooperation Council states and rising smartphone penetration in Nigeria and Kenya, yet political instability continued to temper wider adoption. Combined, these regional narratives underscore how the Dynamic Random Access Memory market diversifies revenue streams even as manufacturing remains concentrated in East Asia.

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Micron Technology Inc.

- ChangXin Memory Technologies Inc. (CXMT)

- Nanya Technology Corporation

- Winbond Electronics Corporation

- Powerchip Semiconductor Manufacturing Corp. (PSMC)

- Fujian Jinhua Integrated Circuit Co., Ltd. (JHICC)

- GigaDevice Semiconductor (Beijing) Inc.

- Etron Technology Inc.

- Integrated Silicon Solution Inc. (ISSI)

- Elite Semiconductor Memory Technology Inc. (ESMT)

- Zentel Electronics Corporation

- Alliance Memory, Inc.

- AP Memory Technology Corp.

- Phison Electronics Corporation

- JSC Mikron (Mikron Group)

- AMIC Technology Corporation

- Utron Technology Inc.

- Hua Hong Semiconductor Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ascending Content Footprint of AI and Generative-AI Workloads in Hyperscale Data Centers

- 4.2.2 Soaring LPDDR Adoption in 5G Flagship and Mid-Tier Smartphones Across APAC

- 4.2.3 Automotive Zonal/Domain Controllers Migrating from NOR to High-Temperature DRAM

- 4.2.4 Edge-AI and Industrial IoT Boards Requiring Extended-Temperature DRAM Modules

- 4.2.5 Cloud Service Providers' Transition to CXL-attached Memory Pools

- 4.3 Market Restraints

- 4.3.1 Supply-Demand Cyclicality Driving Extreme ASP Volatility

- 4.3.2 Yield-Erosion Challenges Below 10 nm EUV Nodes

- 4.3.3 Geopolitical Export Controls on China Limiting High-density Server DRAM Shipments

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.8.1 DRAM Spot Price (Per GB)

- 4.8.2 Pricing Trends Analysis

- 4.9 Macroeconomic Impact Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 DDR2 and Earlier

- 5.1.2 DDR3

- 5.1.3 DDR4

- 5.1.4 DDR5

- 5.1.5 LPDDR

- 5.1.6 GDDR

- 5.2 By Technology Node

- 5.2.1 >=20 nm

- 5.2.2 19 nm - 10 nm

- 5.2.3 <10 nm (EUV)

- 5.3 By Capacity

- 5.3.1 <=4 GB

- 5.3.2 4 - 8 GB

- 5.3.3 8 - 16 GB

- 5.3.4 >=16 GB

- 5.4 By End-use Application

- 5.4.1 Smartphones and Tablets

- 5.4.2 PCs and Laptops

- 5.4.3 Servers and Hyperscale Data Centers

- 5.4.4 Graphics and Gaming Consoles

- 5.4.5 Automotive Electronics

- 5.4.6 Consumer Electronics (Set-top Boxes, Smart TV, VR/AR)

- 5.4.7 Industrial and IoT Devices

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Taiwan

- 5.5.3.3 South Korea

- 5.5.3.4 Japan

- 5.5.3.5 India

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Chile

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 SK Hynix Inc.

- 6.4.3 Micron Technology Inc.

- 6.4.4 ChangXin Memory Technologies Inc. (CXMT)

- 6.4.5 Nanya Technology Corporation

- 6.4.6 Winbond Electronics Corporation

- 6.4.7 Powerchip Semiconductor Manufacturing Corp. (PSMC)

- 6.4.8 Fujian Jinhua Integrated Circuit Co., Ltd. (JHICC)

- 6.4.9 GigaDevice Semiconductor (Beijing) Inc.

- 6.4.10 Etron Technology Inc.

- 6.4.11 Integrated Silicon Solution Inc. (ISSI)

- 6.4.12 Elite Semiconductor Memory Technology Inc. (ESMT)

- 6.4.13 Zentel Electronics Corporation

- 6.4.14 Alliance Memory, Inc.

- 6.4.15 AP Memory Technology Corp.

- 6.4.16 Phison Electronics Corporation

- 6.4.17 JSC Mikron (Mikron Group)

- 6.4.18 AMIC Technology Corporation

- 6.4.19 Utron Technology Inc.

- 6.4.20 Hua Hong Semiconductor Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment