PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644949

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644949

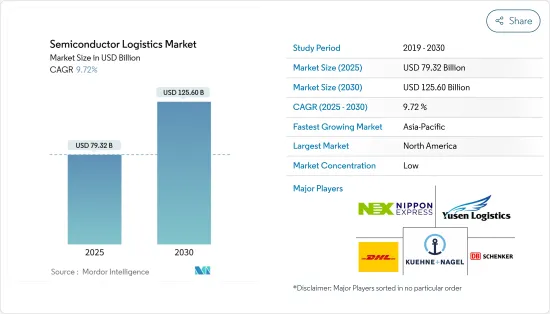

Semiconductor Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Semiconductor Logistics Market is expected to register a CAGR of greater than 7% during the forecast period.

Key Highlights

- There has been an increasing demand for smart devices, the need for sustainable production methods, the importance of cultivating a talent pool, and growth in APAC's semiconductor market share will shape the semiconductor logistics industry. However, supply chain and labour disruptions caused by COVID-19 had resulted in a worldwide chip shortage crisis, which had been exacerbated by ongoing trade tensions between the US and China, as well as conflict in Russia. The pace of technological advancement will quicken. The construction of 5G networks and the Internet of Things has already laid the groundwork for connectivity and automation.

- Insufficient manufacturing capacity to meet market demand is a key thematic trend permeating many facets of the semiconductor supply chain. Semiconductors are essential components in many renewable energy applications, electric vehicles, smartphones and other personal electronics, data centres, and even defence weapons. However, behind the scenes, today's semiconductor companies are facing a slew of challenges. Even at full capacity, fabs have been unable to meet demand, resulting in product lead times of six months or longer. The ongoing semiconductor shortage is now making headlines regularly, especially when it forces automotive OEMs to delay vehicle production. Furthermore, semiconductor firms are dealing with increased design complexity, a talent shortage, and pandemic-related issues, all of which are disrupting the complex, global supply chain that connects players in different markets.

- The semiconductor industry must see the logistical challenges of the last two years as a wake-up call that drastic action is required. When COVID-19 went into effect, many businesses saw a significant drop in sales. The automotive industry lost 80% of its buyers, resulting in a sharp drop in semiconductor demand. Some predict a global semiconductor shortage that will last until 2024. Between 2020 and 2022, it was estimated that these shortages cost the global economy more than USD 500 billion. Worse than the immediate financial impact, these shortages have revealed that semiconductor supply chains are inadequate. Several obvious flaws have been exposed, and addressing them requires more than simply catching up on order backlogs.

- The future of semiconductor companies is dependent on finding a way to compete with logistical challenges as a signal that drastic action is required. Because the demand for semiconductors is only going to increase, those who can get them to end users more efficiently will be the ones to benefit the most in the coming years. The semiconductor value chain is unusually complex, relying on a global network of material and equipment suppliers. This makes efficient supply chain management extremely difficult, resulting in excess stock and routine bottlenecks. A good example is freight management. Freight issues, ranging from port congestion to container shortages, can result in longer lead times and longer shipment delays. Other factors influencing the supply chain include humidity, shock impact, and theft. But without precise data on the progress of shipments and GPS tracking, leaders are often left operating in the dark.

Semiconductor Logistics Market Trends

Increasing demand for semiconductor driving the market

Since 2020, the global chip shortage has worsened, with price increases being the semiconductor industry's defining trend. Upstream material and equipment manufacturers are facing supply shortages, chipmakers have increased investments to expand their product lines on occasion, and downstream semiconductor companies have made significant profits. Overall, the supply shortage of panel drive IC, consumer-grade MCU, memory chips, and other products have begun to ease, signalling the start of a price decrease. However, some power semiconductor chips, particularly those used in automotive, industrial control, IoT, and other fields, remain scarce.

The primary reason for this is that DRAM has quickly entered a downward price trend as the market undergoes cyclical changes. South Korea, the world's largest memory chip producer, has seen the largest increase in chip inventory in more than four years. According to statistics released by the South Korean statistics office in June 2022, the country's chip inventory increased by 53.4% over the same period in 2021 and has been steadily increasing since October 2021. As demand for smartphones, PCs, and consumer applications falls, global demand for memory chips used in electronic products falls. Despite relatively strong server demand, memory chip prices will continue to fall in the second half of 2022 as a result of high inventory levels.

The consumer market's downward trend has accelerated the cyclical changes in the storage market, and MCU chips are also affected. Consumer electronics, as represented by mobile phones and computers, have shown a downward trend in recent years, with likely negative growth in the entire year of 2022. According to this trend, news circulated in April of this year that terminal chips for consumer electronics could face up to 30% order cancellations, putting huge inventory pressure on the supply chain and terminal manufacturers who were busy preparing goods. Order cancellations from consumer electronic terminals have now gradually spread to chip manufacturers.

Increasing use of advanced technology and value-added services driving the market

Key decisions are made with insufficient insight as there is less visibility in the semiconductor supply chain and logistics. Leaders must be able to see their options and compare different courses of action as truck markets fragment and shipping container costs spiral. However, this requires centralized, dependable real-time data. While 83% of businesses say they are more aware of the risks associated with transportation blockades than they were before the pandemic, they still need to find the right technology to enable proper visibility. The pandemic exemplified how disruptive a single event can be, causing cascading effects across entire semiconductor supply chains. This highlights the critical importance of supply chain flexibility - the ability to adjust material purchases, production levels, and transportation capacity to meet demand. However, acknowledging this proves extremely tough.

Overreliance on single partners in semiconductor supply chains is a problem. To ensure the resilience of their supply chains, semiconductor companies require access to multiple partners, whether it's a material supplier, manufacturing base, or freight provider. Gaining access to multiple partners, on the other hand, is not so simple, especially when many brokers have hidden biases. This means that leaders must either navigate multiple highly complex markets on their own or find a partner who can connect them with providers with complete impartiality. Another issue is trust: flexibility necessitates companies having multiple providers they can trust to comply with regulations. This means they must either conduct extensive due diligence or find a partner to whom they can delegate this responsibility in complete transparency.

Semiconductor Logistics Industry Overview

The Semiconductor Logistics Market is highly competitive and fragmented with a large number of local, regional and a few global players penetrating the market. Major players are DHL, Nippon Express, Yusen Logistics, DB Schenker, Kuehne+Nagel, and many more. The use of proper and advanced technology to bring clarity in the semiconductor supply chain and logisitcs is going to bring a difference between the companies. Global players hold a good share in this market due to availibility of services compared to the regional and local players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Overview

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.2 Restraints

- 4.3.3 Opportunities

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of the COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Function

- 5.1.1 Transportation

- 5.1.1.1 Roadways

- 5.1.1.2 Railways

- 5.1.1.3 Water and Seaways

- 5.1.1.4 Airways

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services (Packaging, Customs Clearance, Freight Brokerage, and Other Services)

- 5.1.1 Transportation

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL

- 6.2.2 Nippon Express

- 6.2.3 Yusen Logistics

- 6.2.4 DB Schenker

- 6.2.5 Kuehne+Nagel

- 6.2.6 Omni Logistics

- 6.2.7 Dimerco

- 6.2.8 CEVA Logistics

- 6.2.9 HOYER Group

- 6.2.10 MAERSK

- 6.2.11 Dintec Shipping Express*

7 FUTURE OF THE MARKET

8 APPENDIX