PUBLISHER: M14 Intelligence Research Pvt. Ltd. | PRODUCT CODE: 1694052

PUBLISHER: M14 Intelligence Research Pvt. Ltd. | PRODUCT CODE: 1694052

Global Electric Vehicle (EV) Battery Technology Market and Supply Chain Analysis, 2025-2035

Lithium-ion (LFP and NMC) and Emerging Battery Technology (Solid-state and Sodium-ion) Market Sizing, Regional breakdown, Regulatory Policies, Battery-as-a-Service Model (BaaS), Gigafactories, Trends & Dynamic, Supply Chain Analysis, Competition.

Key Highlights:

This comprehensive study examines the -

- Strategic Implications and Actionable Insights on EV Battery Technology for Automotive Players

- Battery technology trends, supply chain risks, and future outlook.

- Raw material price spikes and supply chain distribution

- China's market dominance and potential new tariffs impacting the growth of EV Battery industry

- Gigafactory constructions, battery swapping networks, and Batter-as0a Service model (BaaS)

- EV Battery Market Sizing and forecasting, 2025-2035

- Market breakdown by Technology- LPF, NMC, Solid-state, and Sodium-Ion

- Research & Development Analysis

- Partnership between OEMs and Start-ups, Cross-Industry Partnerships

- Market Analysis from perspective of OEMs, Battery Manufacturers, and Investors

Exhaustive Coverage:

- Global EV Car Sales Forecast - Breakdown by Vehicle Type and Region

- EV Battery Production Statistics, by Region

- Gigafactory Capacity- Planned Vs Operational

- EV Battery Market Sizing and Forecast, 2025-2035

- EV Batteries Installed Capacity, GWh in 2024, Estimated in 0225, Forecasted to 2035

- EV Batteries Market Breakdown- By Technology Type , 2025-2035

- Lithium-ion including LFP AND NMC

- Emerging Tech including Solid-State and Sodium-ion

- EV Batteries Market Size- Regional Breakdown, 2025-2035

- North America Market, 2025-2035

- Europe Market, 2025-2035

- China Market, 2025-2035

- Asia-Pacific (except China) Market, 2025-2035

- Key Market Challenges

- Geopolitical Tensions (China-West Decoupling)

- Raw Material Price Volatility

- Solid-Sate Delays

- Changing Subsidy policies

- Competition Assessment

- Competitor Benchmarking

- Market Share Analysis

- Top Battery Makers

- OEM In-housed Vs Outsourced

- Joint Ventures for Gigafactories

- Start-up and OEM partnerships

- Cross-industry collaborations

- Company Profiles

WHAT SHOULD YOU LOOK AT ?

THE SHIFTING DYNAMICS OF EV BATTERY INDUSTRY

- RAW MATERIAL SHORTAGE AND RECYCLING BRIDGING THE GAP BY 2023

- CHINA'S DOMINANCE FLOODING GLOBAL MARKET WITH LFP BATTERIES

- POTENTIAL NEW TARIFFS BY US AND EU ON CHINESE BATTERIES BOOMING THE DOMESTIC

- GIGAFACTORY CONSTRUCTIONS ON RISE - TELSA, GM FORD ON LEAD

- AI DRIVEN BATTERY MANAGEMENT SYSTEM (BMS)

- BATTERY SWAPPING NETWORKS GAINING TRACTION

- BATTERY AS A SERVICE (BAAS) MODEL

Market Overview

Charging the Future: The Explosive Rise of EV Batteries

Electric vehicles (EVs) are steering the world toward a greener tomorrow, and their batteries are the beating heart of this revolution. With demand skyrocketing, the next decade promises seismic shifts in technology, markets, and competition.

This report unpacks the electrifying future of EV batteries-where we're headed, who's leading the charge, and how manufacturers can stay ahead in this high-voltage race.

The Electric Horizon: Where EVs Are Headed in 10 Years

The EV industry is gearing up for a massive leap over the next 5 to 10 years. Sales are expected to surge, with EVs potentially claiming 20-30% of global new car sales by 2030, a steep climb from 4% in 2020. This boom hinges on shrinking battery costs, sprawling charging networks, and government policies slamming the brakes on fossil-fuel vehicles. Battery energy density could double, pushing ranges beyond 500 miles, while ultra-fast charging slashes wait times to mere minutes. Countries like those in the EU are eyeing 2035 to phase out internal combustion engines, turbocharging EV adoption.

"The EV tipping point is near-by 2030, one in three new cars could be electric, driven by cheaper batteries and a global push to ditch gas guzzlers."

Battery Breakthroughs: Powering Tomorrow's Drives

Today, lithium-ion batteries reign supreme, with Nickel-Manganese-Cobalt (NMC) delivering long ranges and Lithium Iron Phosphate (LFP) slashing costs and boosting safety.

Lithium-Ion Variants: NMC batteries, using lithium nickel manganese cobalt oxides, are common for high energy density, while LFP batteries, with 41% global market share by capacity in 2023, are cheaper and more sustainable. <>LFP's adoption is driven by its lower cost, despite lower energy density

Emerging Technologies: Sodium-ion batteries, announced for mass production by companies like BYD and CATL in 2023, could cost 20% less, suitable for urban EVs and stationary storage. Solid-state batteries, pioneered by <>Toyota and QuantumScape, promise higher energy density and safety but are not yet commercial.

Innovations: Dual-ion batteries (DIB) and bipolar LFP batteries are emerging, offering quick charging and higher voltage, though cycle life remains a challenge.

"Solid-state batteries could zap EV ranges past 600 miles, but their high costs mean lithium-ion will hold the wheel for another decade."

The Global Battery Battle: Who's Winning?

Regional leadership in the EV battery market is evident, with distinct roles:

- China: Dominates with over 51% market share in 2022, driven by low production costs and firms like CATL (37.9% global share in 2024) and BYD (17.2%). LFP batteries, cheaper to produce, are prevalent, with two-thirds of EV sales using this chemistry in 2023.

- North America: Growing, with the US attracting $210 billion in investments since 2021, led by Tesla and partnerships like Ford with SK On. However, production costs are 20% higher than in China.

- Europe: Faces challenges with higher costs (50% more than China) and supply chain weaknesses, with Northvolt's bankruptcy highlighting difficulties. Efforts to build local capacity include gigafactory projects, aiming for 35-40 by 2030.

- Asia Pacific: Emerging markets like India and South Korea are growing, with India seeing 70% year-on-year EV registration growth in 2023, supported by schemes like FAME II .

The EV battery market is a geopolitical chessboard. China commands over 70% of global production, with giants like CATL and BYD flexing muscle through scale and subsidies. Japan and South Korea follow, with Panasonic and LG Chem powering brands like Tesla and Hyundai. Europe's scrambling to catch up, pumping funds into the European Battery Alliance to build its own supply chain. North America, led by Tesla's Nevada Gigafactory, is revving up domestic production to cut reliance on Asia.

Here's a snapshot of regional capacities:

| Type | Advantages | Disadvantages | Adoption |

|---|---|---|---|

| NMC | High energy density (~250 Wh/kg) | Expensive (cobalt reliance) | Declining (Tesla, GM phasing out) |

| LFP | Cheap, long lifespan, cobalt-free | Lower energy density (~180 Wh/kg) | Dominating (Tesla, BYD, Ford) |

| Solid-State | Ultra-high energy density (~500 Wh/kg) | Not yet commercialized | Toyota, QuantumScape targeting 2026–2030 |

| Region | Current capacity(GWh) | Projected 2030(GWh) | Projected 2035(GWh) |

|---|---|---|---|

| Asia | 500 | 1500 | 3000 |

| Europe | 50 | 400 | 800 |

| North America | 100 | 300 | 600 |

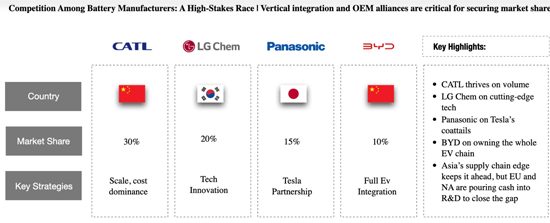

Battery Giants Face Off: The Heavyweight Showdown

Competition among battery makers is fierce. Here's how the big players stack up:

CATL thrives on volume, LG Chem on cutting-edge tech, Panasonic on Tesla's coattails, and BYD on owning the whole EV chain. Asia's supply chain edge keeps it ahead, but Europe and North America are pouring cash into R&D to close the gap.

Highlights:

- Leaders: China leads, with CATL and BYD dominating, benefiting from integrated supply chains and lower costs. CATL's 339.3 GWh installations in 2024 underscore its lead.

- Followers: North American firms like LG Energy Solution and European players like Northvolt face challenges, with Europe's higher costs (50% more than China) and supply chain weaknesses. Northvolt's bankruptcy in 2024 highlights these difficulties.

OEM Competition and New Entrants

- OEM Strategies: Companies like Tesla, BYD, and traditional OEMs (GM, Volkswagen) compete on pricing, innovation, and supply chain control. Tesla's market share fell from 17% in 2019 to 13% in 2022 due to competition. Vertical integration, like Tesla's gigafactories, provides cost advantages.

- New Entrants: Asian firms, especially Chinese, find space through niche markets (e.g., affordable small cars) and government subsidies, disrupting Europe's market. They leverage online sales and community-building strategies.

Established automotive manufacturers and emerging players are engaged in intense competition within the electric vehicle (EV) market. Industry leaders such as Tesla, Volkswagen, and General Motors (GM) are pursuing aggressive strategies to strengthen their positions. Tesla is vertically integrating its battery production to enhance self-sufficiency, Volkswagen is collaborating with Northvolt to ensure a reliable battery supply, and GM is focusing on the development of mass-market EVs to broaden its customer base.

Concurrently, new entrants such as Rivian, which specializes in electric trucks, and Lucid Motors, which targets the luxury EV segment, are entering the market by leveraging innovative designs and advanced technology to capture market share. A critical determinant of success in this competitive landscape is the ability to secure a stable and sufficient supply of batteries.

New entrants like Rivian could disrupt the established automakers, but only if they lock down batteries in a supply-starved world.

Final conclusion:

What's Next for EV Batteries?

The EV battery market is set for exponential growth, with demand soaring as electrification takes hold. Asia leads today, but Europe and North America are closing the gap through investment and innovation. Price volatility and competition pose challenges, yet opportunities abound for those who innovate and adapt. For tier-1 suppliers and battery manufacturers, the path forward is clear: invest in technology, secure supply chains, and embrace sustainability to power the EVs of tomorrow.

Key Questions Answered:

- What battery technology shifts (solid-state, sodium-ion) will disrupt the market by 2035, and how should companies prepare?

- Which regulatory changes (EU Battery Regulation, IRA sourcing rules) will impact market access and profitability?

- Where should OEMs source critical materials to reduce China dependence while maintaining cost competitiveness?

- How can Tier 1 suppliers maintain relevance as OEMs like Tesla vertically integrate battery production?

- What R&D investments (solid-state, silicon anodes) offer the highest ROI for battery component suppliers?

- Which emerging markets (India's PLI scheme, Poland's recycling hub) present the best growth opportunities?

- How can Tier 2 suppliers protect margins against volatile lithium (300% price spikes) and cobalt prices?

- Which alternative chemistries (sodium-ion, LFP) will reshape raw material demand in next 5-10 years?

- How will recycling innovations (second-life batteries, 30% cost reductions) transform the supply chain?

- What strategic timelines (short/mid/long-term) should different players follow to maintain competitiveness?

Companies Mentioned:

|

|

|

TABLE OF CONTENTS

RESEARCH SCOPE

RESEARCH METHODOLOGY

BATTERY TECHNOLOGY TRENDS AND DYNAMIC

- RAW MATERIAL SHORTAGE AND RECYCLING BRIDGING THE GAP BY 2030

- CHINA'S DOMINANCE FLOODING GLOBAL MARKET WITH LFP BATTERIES

- POTENTIAL NEW TARIFFS BY US AND EU ON CHINESE BATTERIES BOOMING THE DOMESTIC MANUFACTURING

- GIGAFACTORY CONSTRUCTIONS ON RISE- TESLA, GM, FORD ON LEAD

- AI DRIVEN BATTERY MANAGEMENT SYSTEM (BMS)

- BATTERY SWAPPING NETWORKS GAINING TRACTION

- BATTERY AS A SERVICE (BAAS) MODEL

MARKET OUTLOOK AND FORECAST

- GLOBAL EV CAR SALES FORECAST - BREAKDOWN BY VEHICLE TYPE AND REGION

- EV BATTERY PRODUCTION STATISTICS BY REGION

- GIGAFACTORY CAPACITY- PLANNED VS OPERATIONAL

- EV BATTERY MARKET SIZING AND FORECAST, 2025-2035

- EV BATTERIES INSTALLED CAPACITY, GWH IN 2024, ESTIMATED IN 2025, FORCASTED TO 2035

- EV BATTERIES MARKET SIZE- BREAKDOWN BY TECHNOLOGY TYPE , 2025-2035

- LITHIUM-ION- LFP AND NMC

- EMERGING TECH- SOLID-STATE AND SODIUM-ION

- EV BATTERIES MARKET SIZE- REGIONAL BREAKDOWN, 2025-2035

- NORTH AMERICA MARKET, 2025-2035

- EUROPE MARKET, 2025-2035

- CHINA MARKET, 2025-2035

- ASIA-PACIFIC (EXCEPT CHINA) MARKET, 2025-2035

KEY MARKET CHALLENGES

- GEOPOLITICAL TENSIONS (CHINA-WEST DECOUPLING)

- RAW MATERIAL PRICE VOLATILITY

- SOLID-STATE DELAYS

- CHANGING SUBSIDY POLICIES

COMPETITION ASSESSMENT

- COMPETITOR BENCHMARKING

- MARKET SHARE ANALYSIS

- TOP BATTERY MAKERS

- OEM IN-HOUSED VS OUTSOURCED BATTERIES

- JOINT VENTURES FOR GIGAFACTORIES

- START-UPS AND OEM PARTENRSHIPS

- CROSS INDUSTRY COLLABORATIONS

COMPANY PROFILES

- Tesla

- Byd

- CaTL

- LG Energy Solution

- Panasonic

- SK On

- Northvolt

- Samsung SDI

- QuantumScape

- Solid Power

- Nio

- ChargePoint

- ABB

- StoreDot

- Freyr Battery

- ACC (Automotive Cells Co.)

- Farasis Energy

- Envision AESC

- Microvast

- Romeo Power

- ProLogium

- Nexeon

- Ample

- SparkCharge

- Electrify America

- Ionity

- Our Next Energy (ONE)

RECOMMENDATIONS FOR STAKEHOLDERS - OEMS, SUPPLIERS, AND INVESTORS

APPENDICES

LIST OF SECONDARY SOURCES

ABOUT M14 INTELLIGENCE