PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1858529

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1858529

Agriculture Drones Market by Offering Type (Hardware, Software, Drone-as-a-Service), Technology Type, Payload Capacity, Component, Farm Produce, Farm Size, Range, Application, Farming Environment, and Region - Global Forecast to 2030

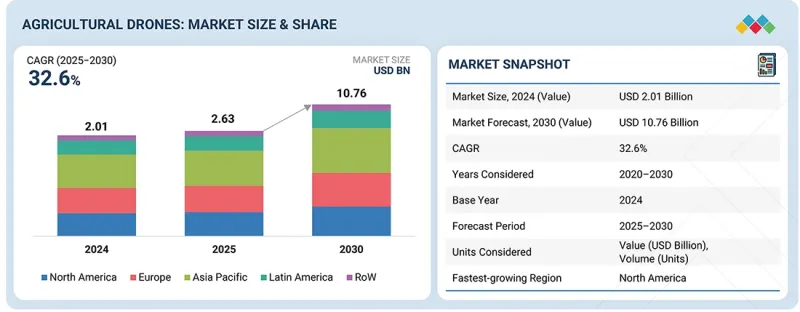

The agriculture drones market is estimated to be USD 2.63 billion in 2025 and is projected to reach USD 10.76 billion by 2030, at a CAGR of 32.6% from 2025 to 2030. The FAA's approval of drones for agricultural use has led to an increase in their adoption. This will open a huge opportunity in the market for agricultural drones. With fewer regulatory hurdles, stakeholders may adopt drone technology with minimal compliance requirements, thereby opening the market to wider penetration. The use of drones and data analytics platforms will enable effective decision-making, optimizing resources, and leading to improved productivity. The focus on sustainability in agriculture makes it possible to use drones for environmentally friendly practices, and the FAA's waiver of exemption has made the use of drones easier. Lastly, the changed outlook in terms of rules means training programs and consultancy services for the smooth running of drone operations, thereby increasing demand. In conclusion, this exemption significantly contributes to creating a favorable environment for the growth of the agriculture drone market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Units) |

| Segments | By Offering, Technology Type, Payload Capacity, Component, Farm Produce, Farm Size, Range, Application, Farming Environment, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World (RoW) |

Security and safety concerns associated with civil and commercial application of drones: Security and safety concerns due to civil and commercial use of drones can be a significant restraint for the agriculture drones market in the following ways. The first concern is the invasion of privacy; a camera- and sensor-equipped drone is likely to capture images or data from private properties, which can lead to legal challenges and public backlash, thus dissuading adoption among farmers who fear possible cases of infringement. Further risks include the possibility of accidents and collisions with other aircraft. Drones will occupy agricultural airspace, so any accident could potentially result in injury or property damage, increasing regulation and liability that may burden farmers from using drone technology.

"By application, precision farming segment to dominate agriculture drones market"

With several compelling reasons for the precision farming segment to dominate the agriculture drones market, the demand in this segment is strong. Growing populations worldwide have generated an imperative need for food security, and optimal agricultural productivity has become crucial. In turn, precision farming allows farmers to make data-driven decisions that increase crop yields and optimize resource usage. Drones are essential in the process, providing real-time data and detailed analytics that optimize the operations. Other technological advancements include the enhanced capabilities of drones, featuring high-resolution imaging, multispectral sensors, and integration with AI, which enables sophisticated crop and soil analysis to track growth patterns and assess health. Again, these types of operations align with environmental regulations and consumer preferences for sustainably sourced products. Government funding for contemporary agricultural techniques, by encouraging farmers to invest in drones and precision farming solutions, is thus spearheading the segment.

"Asia Pacific to witness significant CAGR during the forecast period"

The agriculture drones market is expected to grow significantly in the Asia Pacific region. The rate of adoption of precision agriculture is very high, as farmers increasingly find drones useful for crop monitoring, soil analysis, and targeted pesticide application. Government initiatives aimed at modernizing agriculture also further support this growth, as many Asian governments promote advanced technologies through funding, subsidies, and training programs to improve food security and sustainability.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the agriculture drones market:

- By Company Type: Tier 1 - 55%, Tier 2 - 35%, and Tier 3 - 10%

- By Designation: CXO's - 33%, Managers - 25%, Executives- 42%

- By Region: North America - 30%, Europe - 35%, Asia Pacific - 20%, South America - 10% and Rest of the World -5%

Prominent companies in the market include DJI (China), Trimble Inc. (US), Parrot Drone Sas (France), Yamaha Motor Co., Ltd. (Japan), Ageagle Aerial Systems Inc. (US), Dronedeploy (US), XAG Co., Ltd. (China), Sentera (US), Autel Robotics (China), Yuneec (US), Microdrones (Germany), Gamaya (Brazil), Aerialtronics Dv B.V. (Netherlands), Hiphen (France), and Hylio (US).

Other players include Jouav (China), Shenzhen GC Electronics Co., Ltd. (China), Aries Solutions (India), Wingtra AG (Switzerland), Sky-Drones Technologies Ltd. (UK), Delair (France), Shenzhen Grepow Battery Co., Ltd. (China), Applied Aeronautics (US), and Vision Aerial, Inc. (US)

Research Coverage:

This research report categorizes the agriculture drones market by payload capacity (small payload drones (up to 2 kg), medium payload drones, large payload drones, and heavy payload drones), farm size (small-sized farms, middle-sized farms, large-sized farms, and super large farms), component (frames, controller systems, propulsion systems, sensors and camera systems, navigation systems, batteries, other components), offering type (hardware, software, and drone-as-a-services), technology type (thermal imaging, multispectral imaging, hyperspectral imaging, light detection and ranging (LIDAR), RGB imaging, synthetic aperture radar (SAR), near-infrared (NIR) imaging, global navigation satellite system (GNSS)), farm produce (cereals and grains, oilseeds and pulses, fruits and vegetables, other crop types), range (visual line of sight (VLOS), beyond visual line of sight (BVLOS)),application (precision farming, livestock monitoring, precision fish farming, smart greenhouses, other applications), farming environment (outdoor, indoor), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the agriculture drones market. A detailed analysis of the key industry players has been done to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the agriculture drones market. This report covers the competitive analysis of upcoming startups in the agriculture drones market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem and market mapping, patent analysis, and regulatory landscape, among others.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall agriculture drones and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (government initiatives to promote water conservation), restraints (high initial investment costs of agriculture drones), opportunities (increasing adoption of precision agriculture and sustainable practices), and challenges (lack of training and awareness among farmers) influencing the growth of the agriculture drones market.

- New product launch/Innovation: Detailed insights on research & development activities and new product launches in the agriculture drones market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the agriculture drones across varied regions.

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the agriculture drones market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product food prints of leading players such as DJI (China), Trimble Inc. (US), Parrot Drone Sas (France), Yamaha Motor Co., Ltd. (Japan), Ageagle Aerial Systems Inc. (US), XAG Co., Ltd. (China), Autel Robotics (China), and other players in the agriculture drones market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 UNIT CONSIDERED

- 1.4.1 CURRENCY/VALUE UNIT

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key insights from industry experts

- 2.1.2.3 Breakdown of primary profiles

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.2.2 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AGRICULTURE DRONES MARKET

- 4.2 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY OFFERING TYPE AND COUNTRY

- 4.3 AGRICULTURE DRONES MARKET, BY OFFERING TYPE

- 4.4 AGRICULTURE DRONES MARKET, BY FARM SIZE

- 4.5 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY

- 4.6 AGRICULTURE DRONES MARKET, BY FARM PRODUCE

- 4.7 AGRICULTURE DRONES MARKET, BY APPLICATION

- 4.8 AGRICULTURE DRONES MARKET, BY RANGE AND REGION

- 4.9 AGRICULTURE DRONES MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 REDUCTION IN ARABLE LAND

- 5.2.2 RAPID DIGITALIZATION

- 5.3 MARKET DYNAMICS

- 5.3.1 DRIVERS

- 5.3.1.1 Demand for smart farm optimization and resource usage efficiency optimization using agricultural drones

- 5.3.1.2 Favorable government policies, subsidies, and regulations

- 5.3.1.3 Availability of software solutions for field surveys and data analytics

- 5.3.1.4 Growing concerns regarding change in diet and climate patterns

- 5.3.1.5 Increasing labor shortages

- 5.3.2 RESTRAINTS

- 5.3.2.1 Security and safety concerns associated with civil and commercial applications of drones

- 5.3.2.2 Large number of fragmented lands in developing countries

- 5.3.2.3 Lack of technical knowledge and training activities

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Exemptions by US FAA for use of agriculture drones

- 5.3.3.2 High adoption of aerial data collection tools in agriculture

- 5.3.3.3 Increase in use of agricultural-based software via smartphones

- 5.3.3.4 Need for early detection of crop diseases and ease of farm management

- 5.3.4 CHALLENGES

- 5.3.4.1 Management of data collected by agriculture drones

- 5.3.4.2 Lack of standardization of communication interfaces and protocols for precision agriculture

- 5.3.4.3 Lack of technical knowledge among farmers

- 5.3.4.4 Scarcity of trained pilots

- 5.3.4.5 High upfront costs of agricultural drones

- 5.3.1 DRIVERS

- 5.4 IMPACT OF GEN AI ON AGRICULTURE DRONES

- 5.4.1 INTRODUCTION

- 5.4.2 USE OF GEN AI ON AGRICULTURE DRONES

- 5.4.3 CASE STUDY ANALYSIS

- 5.4.3.1 AI drone revolutionizes weed control in Canadian agriculture

- 5.4.3.2 Gayama enhanced agricultural productivity and sustainability through innovative AI technologies

- 5.4.4 IMPACT ON AGRICULTURE DRONES MARKET

- 5.4.5 ADJACENT ECOSYSTEM WORKING ON GENERATIVE AI

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 VALUE CHAIN ANALYSIS

- 6.2.1 RESEARCH & DEVELOPMENT EXECUTIVES

- 6.2.2 DEVICE & COMPONENT MANUFACTURERS

- 6.2.3 SYSTEM INTEGRATORS

- 6.2.4 SERVICE PROVIDERS

- 6.2.5 END USERS

- 6.2.6 POST-SALES SERVICE PROVIDERS

- 6.3 TRADE ANALYSIS

- 6.3.1 EXPORT SCENARIO OF HS CODE 8806

- 6.3.2 IMPORT SCENARIO OF HS CODE 8806

- 6.4 SUPPLY CHAIN ANALYSIS

- 6.5 TECHNOLOGY ANALYSIS

- 6.5.1 KEY TECHNOLOGIES

- 6.5.1.1 Internet of Things (IoT)

- 6.5.1.2 Artificial Intelligence and Machine Learning

- 6.5.1.3 Machine Learning (ML)

- 6.5.2 COMPLEMENTARY TECHNOLOGIES

- 6.5.2.1 Remote sensing technology

- 6.5.2.2 Crop management software

- 6.5.3 ADJACENT TECHNOLOGIES

- 6.5.3.1 Robotics

- 6.5.1 KEY TECHNOLOGIES

- 6.6 PRICING ANALYSIS

- 6.6.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PAYLOAD CAPACITY, 2024

- 6.6.2 AVERAGE SELLING PRICE TREND, BY PAYLOAD CAPACITY, 2020-2024

- 6.6.3 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024

- 6.7 ECOSYSTEM ANALYSIS

- 6.7.1 DEMAND SIDE

- 6.7.2 SUPPLY SIDE

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.9 PATENT ANALYSIS

- 6.9.1 LIST OF MAJOR PATENTS

- 6.10 KEY CONFERENCES & EVENTS, 2025-2026

- 6.11 REGULATORY LANDSCAPE

- 6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11.2 REGULATORY FRAMEWORK

- 6.11.2.1 North America

- 6.11.2.1.1 US

- 6.11.2.1.2 Canada

- 6.11.2.1.3 Mexico

- 6.11.2.2 Europe

- 6.11.2.3 Asia Pacific

- 6.11.2.3.1 India

- 6.11.2.3.2 China

- 6.11.2.3.3 Australia

- 6.11.2.4 South America

- 6.11.2.4.1 Brazil

- 6.11.2.5 Rest of the World (RoW)

- 6.11.2.1 North America

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS & BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.13.2 BUYING CRITERIA

- 6.14 CASE STUDY ANALYSIS

- 6.14.1 EAVISION LAUNCHED NEW INTELLIGENT AGRICULTURAL SPRAYING DRONE IN CHINA

- 6.14.2 PARROT LAUNCHED ANAFI THERMAL FOR BETTER CROP SCOUTING, FIELD MONITORING, AND DATA ANALYTICS

- 6.14.3 ENHANCING TEA PLANTATION PRODUCTIVITY AND SUSTAINABILITY THROUGH DRONE INTEGRATION

- 6.15 INVESTMENT AND FUNDING SCENARIO

- 6.15.1 INTRODUCTION

- 6.16 IMPACT OF 2025 US TARIFF ON AGRICULTURE DRONES MARKET

- 6.16.1 INTRODUCTION

- 6.16.2 KEY TARIFF RATES

- 6.16.3 DISRUPTIONS IN AGRICULTURE DRONES MARKET

- 6.16.4 PRICE IMPACT ANALYSIS

- 6.16.5 KEY IMPACTS ON VARIOUS REGIONS

- 6.16.5.1 North America

- 6.16.5.2 Europe

- 6.16.5.3 Asia Pacific

- 6.16.5.4 South America

- 6.16.5.5 ROW

- 6.16.6 END-USE INDUSTRY-LEVEL IMPACT

7 AGRICULTURE DRONES MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 PRECISION FARMING

- 7.2.1 GOVERNMENT INITIATIVES TO PROMOTE SMART FARMING TO BOOST DEMAND FOR AGRICULTURE DRONES

- 7.2.2 FIELD MAPPING

- 7.2.2.1 Weed Detection

- 7.2.2.2 Plant Counting

- 7.2.2.3 Crop Health Monitoring

- 7.2.2.4 Harvest Season Monitoring

- 7.2.2.5 Other Field Mapping Applications

- 7.2.3 VARIABLE RATE APPLICATION

- 7.2.4 CROP SCOUTING

- 7.2.5 CROP SPRAYING

- 7.2.6 OTHER PRECISION FARMING APPLICATIONS

- 7.3 LIVESTOCK MONITORING

- 7.3.1 GROWTH OF LIVESTOCK MONITORING TO DRIVE ADVANCEMENTS IN DRONE TECHNOLOGY

- 7.4 PRECISION FISH FARMING

- 7.4.1 REAL-TIME DATA AND NON-INVASIVE MONITORING TO BOOST DRONE DEMAND IN FISH FARMING

- 7.5 SMART GREENHOUSE

- 7.5.1 IMPROVED CROP QUALITY AND INCREASED OPERATIONAL EFFICIENCY TO BOOST DEMAND IN SMART GREENHOUSES

- 7.6 OTHER APPLICATIONS

8 AGRICULTURE DRONES MARKET, BY COMPONENT

- 8.1 INTRODUCTION

- 8.2 FRAMES

- 8.2.1 HIGH VERSATILITY OF FIBERGLASS TO DRIVE USE OF FRAMES IN AGRICULTURE DRONES

- 8.3 CONTROLLER SYSTEMS

- 8.3.1 ADVANCEMENTS IN REMOTE CONTROLLER SYSTEMS TO DRIVE USAGE IN AUTOMATION

- 8.4 PROPULSION SYSTEMS

- 8.4.1 PROPULSIONS SYSTEMS TO EXHIBIT HIGHEST ADOPTION IN HYBRID DRONES IN NEXT FIVE YEARS

- 8.5 SENSORS & CAMERA SYSTEMS

- 8.5.1 BOOSTING CROP MONITORING AND YIELD OPTIMIZATION VIA PRECISION DRONE IMAGING

- 8.5.2 RADAR SENSORS

- 8.5.3 LIDAR SENSORS

- 8.5.4 MULTISPECTRAL SYSTEMS

- 8.5.5 IR CAMERAS

- 8.5.6 THERMAL CAMERAS

- 8.5.7 OTHER SENSORS & CAMERA SYSTEMS

- 8.6 NAVIGATION SYSTEMS

- 8.6.1 REDUCE NEED FOR HUMAN INTERVENTION AND ENHANCE OPERATIONAL EFFICIENCY

- 8.6.2 GLOBAL POSITIONING SYSTEM

- 8.6.3 GEOGRAPHIC INFORMATION SYSTEM

- 8.7 BATTERIES

- 8.7.1 LONGER CAPACITY AND LOWER DISCHARGE RATE TO DRIVE USAGE IN SURVEYING AGRICULTURE DRONES

- 8.8 OTHER COMPONENTS

9 AGRICULTURE DRONES MARKET, BY FARM SIZE

- 9.1 INTRODUCTION

- 9.2 SMALL-SIZED FARMS (LESS THAN 180 ACRES)

- 9.2.1 GOVERNMENT INITIATIVES TO PROMOTE DRONE ADOPTION AMONG SMALLHOLDER FARMERS

- 9.3 MID-SIZED FARMS (MORE THAN 180 ACRES AND LESS THAN 500 ACRES)

- 9.3.1 ENHANCED OPERATIONAL EFFICIENCY AND IMPROVED YIELD MANAGEMENT TO DRIVE ADOPTION OF AGRICULTURE DRONES IN MID-SIZED FARMS

- 9.4 LARGE-SIZED FARMS (MORE THAN 500 ACRES AND LESS THAN 2000 ACRES)

- 9.4.1 INCREASED LABOR COSTS AND LABOR SHORTAGES IN AGRICULTURE SECTOR TO DRIVE ADOPTION OF AGRICULTURE DRONES

- 9.5 SUPER LARGE FARMS (MORE THAN 2,000 ACRES)

- 9.5.1 NECESSITY FOR ENHANCED EFFICIENCY AND URGENCY TO INCREASE CROP YIELDS AMID GLOBAL FOOD INSECURITY TO DRIVE ADOPTION

10 AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT

- 10.1 INTRODUCTION

- 10.2 OUTDOOR

- 10.2.1 NEED FOR LARGE-SCALE CROP SPRAYING ACROSS EXPANSIVE FIELDS TO DRIVE MARKET

- 10.3 INDOOR

- 10.3.1 INCREASING USE OF DRONES IN POLLINATION TO BOOST DEMAND

11 AGRICULTURE DRONE MARKET, BY OFFERING TYPE

- 11.1 INTRODUCTION

- 11.2 HARDWARE

- 11.2.1 INCREASING DEMAND FOR PRECISION AGRICULTURE PRACTICES IN HARDWARE TECHNOLOGY TO DRIVE DEMAND

- 11.2.2 FIXED-WING DRONES

- 11.2.3 ROTARY-BLADE DRONES

- 11.2.4 HYBRID DRONES

- 11.3 SOFTWARE

- 11.3.1 GROWING NEED FOR REAL-TIME DATA ANALYSIS AND ACTIONABLE INSIGHTS FOR DECISION-MAKING TO DRIVE DEMAND

- 11.3.2 DATA MANAGEMENT SOFTWARE

- 11.3.3 IMAGING SOFTWARE

- 11.3.4 DATA ANALYTICS SOFTWARE

- 11.3.5 OTHER SOFTWARE

- 11.4 DRONE-AS-A-SERVICE (DAAS)

- 11.4.1 ADOPTION OF ADVANCED DRONE TECHNOLOGIES WITHOUT HIGH CAPITAL INVESTMENT TO BOOST DEMAND

- 11.4.2 DRONE PLATFORM SERVICES

- 11.4.3 DRONE MAINTENANCE, REPAIR, AND OVERHAUL SERVICES

- 11.4.4 DRONE TRAINING & SIMULATION SERVICES

12 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY

- 12.1 INTRODUCTION

- 12.2 SMALL PAYLOAD DRONES (UP TO 2 KG)

- 12.2.1 INCREASING ADOPTION OF PRECISION AGRICULTURE AMONG SMALL-SCALE FARMS AND USER-FRIENDLY OPERATION TO DRIVE DEMAND

- 12.3 MEDIUM PAYLOAD DRONES (2-20 KG)

- 12.3.1 VERSATILITY AND ADVANCED DATA COLLECTION CAPABILITIES TO DRIVE DEMAND

- 12.4 LARGE PAYLOAD DRONES (20-50 KG)

- 12.4.1 WIDER AREA COVERAGE AND ABILITY TO CARRY HEAVY LOADS TO BOOST ADOPTION OF LARGE PAYLOAD DRONES

- 12.5 HEAVY PAYLOAD DRONES (ABOVE 50 KG)

- 12.5.1 SCALABILITY ADVANTAGES FOR LARGER AGRICULTURAL ENTERPRISES TO DRIVE ADOPTION OF HEAVY PAYLOAD DRONES

13 AGRICULTURE DRONES MARKET, BY RANGE

- 13.1 INTRODUCTION

- 13.2 VISUAL LINE OF SIGHT (VLOS)

- 13.2.1 LENIENT REGULATORY FRAMEWORKS AND LESS RESTRICTIVE OPERATIONAL GUIDELINES TO FUEL ADOPTION

- 13.3 BEYOND VISUAL LINE OF SIGHT (BVLOS)

- 13.3.1 GROWING NEED FOR LARGE-SCALE FARMING SOLUTIONS AND ONGOING LABOR SHORTAGE TO BOOST ADOPTION

14 AGRICULTURE DRONES MARKET, BY FARM PRODUCE

- 14.1 INTRODUCTION

- 14.2 CEREALS & GRAINS

- 14.2.1 INNOVATION AND TECHNOLOGICAL ADVANCEMENTS TO DRIVE DEMAND FOR AGRICULTURE DRONES IN CEREALS & GRAINS

- 14.2.2 CORN

- 14.2.3 WHEAT

- 14.2.4 RICE

- 14.2.5 OTHER CEREALS & GRAINS

- 14.3 OILSEEDS & PULSES

- 14.3.1 AGRICULTURE DRONES WITH INFRARED, MULTISPECTRAL, AND HYPERSPECTRAL SENSORS TO DRIVE DEMAND

- 14.3.2 SOYBEAN

- 14.3.3 SUNFLOWER

- 14.3.4 OTHER OILSEEDS & PULSES

- 14.4 FRUITS & VEGETABLES

- 14.4.1 GROWING USE OF DATA ANALYTICS FOR OPTIMIZING CROP HEALTH AND NUTRIENT MANAGEMENT TO BOOST DEMAND

- 14.4.2 POME FRUITS

- 14.4.3 CITRUS FRUITS

- 14.4.4 BERRIES

- 14.4.5 ROOT & TUBER VEGETABLES

- 14.4.6 LEAFY VEGETABLES

- 14.4.7 OTHER FRUITS & VEGETABLES

- 14.5 OTHER CROP TYPES

15 AGRICULTURE DRONES MARKET, BY TECHNOLOGY TYPE

- 15.1 INTRODUCTION

- 15.2 THERMAL IMAGING

- 15.3 MULTISPECTRAL IMAGING

- 15.4 HYPERSPECTRAL IMAGING

- 15.5 LIGHT DETECTION AND RANGING

- 15.6 RGB IMAGING

- 15.7 SYNTHETIC APERTURE RADAR

- 15.8 NEAR-INFRARED IMAGING

- 15.9 GLOBAL NAVIGATION SATELLITE SYSTEM

16 AGRICULTURE DRONES MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Labor shortages and high agricultural production to drive market

- 16.2.2 CANADA

- 16.2.2.1 Constant enhancements and developments in precision farming practices to drive market

- 16.2.3 MEXICO

- 16.2.3.1 Financial support for digital agriculture to drive growth

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 SPAIN

- 16.3.1.1 Rising adoption of agriculture drones to create weed infestation maps for farmers

- 16.3.2 ITALY

- 16.3.2.1 Rising integration of precision agriculture, robots, and agriculture drones to drive market

- 16.3.3 FRANCE

- 16.3.3.1 Application of drones in crop mapping to boost demand

- 16.3.4 GERMANY

- 16.3.4.1 High adoption rate of agriculture drones for livestock monitoring to drive growth

- 16.3.5 UK

- 16.3.5.1 Availability of user-friendly technologies to drive growth

- 16.3.6 REST OF EUROPE

- 16.3.1 SPAIN

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Increasing government spending to drive market

- 16.4.2 INDIA

- 16.4.2.1 Adoption of agriculture drones in surveying farms and assessing crop losses

- 16.4.3 JAPAN

- 16.4.3.1 Increasing adoption of precision farming technology to drive growth

- 16.4.4 AUSTRALIA & NEW ZEALAND

- 16.4.4.1 Different applications and use of agriculture drones to boost demand

- 16.4.5 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.5.1.1 Growth in agricultural activities to boost market for digital advancements

- 16.5.2 ARGENTINA

- 16.5.2.1 Increase in public-private partnerships for agricultural innovations to drive growth

- 16.5.3 REST OF SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.6 REST OF THE WORLD

- 16.6.1 AFRICA

- 16.6.1.1 Increase in investments for agriculture innovations to drive growth

- 16.6.2 MIDDLE EAST

- 16.6.2.1 Surge in agricultural monitoring activities to boost market for digital agriculture

- 16.6.1 AFRICA

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 17.3 REVENUE ANALYSIS, 2020-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.5.1 STARS

- 17.5.2 EMERGING LEADERS

- 17.5.3 PERVASIVE PLAYERS

- 17.5.4 PARTICIPANTS

- 17.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.5.5.1 Company footprint

- 17.5.5.2 Regional footprint

- 17.5.5.3 Offering type footprint

- 17.5.5.4 Application footprint

- 17.5.5.5 Component footprint

- 17.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 17.6.1 PROGRESSIVE COMPANIES

- 17.6.2 RESPONSIVE COMPANIES

- 17.6.3 DYNAMIC COMPANIES

- 17.6.4 STARTING BLOCKS

- 17.6.5 COMPETITIVE BENCHMARKING, START-UPS/SMES, 2024

- 17.6.5.1 Detailed list of key start-ups/SMEs

- 17.6.5.2 Competitive benchmarking of key start-ups/SMEs

- 17.7 COMPANY VALUATION AND FINANCIAL METRICS

- 17.8 BRAND/PRODUCT COMPARISON

- 17.9 COMPETITIVE SCENARIO AND TRENDS

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 DJI

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches

- 18.1.1.3.2 Deals

- 18.1.1.4 MnM view

- 18.1.1.4.1 Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 TRIMBLE INC.

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches

- 18.1.2.3.2 Deals

- 18.1.2.4 MnM view

- 18.1.2.4.1 Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 PARROT DRONE SAS

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 MnM view

- 18.1.3.3.1 Right to win

- 18.1.3.3.2 Strategic choices

- 18.1.3.3.3 Weaknesses and competitive threats

- 18.1.4 YAMAHA MOTOR CO., LTD.

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Expansions

- 18.1.4.4 MnM view

- 18.1.4.4.1 Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 AGEAGLE AERIAL SYSTEMS INC.

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches

- 18.1.5.3.2 Deals

- 18.1.5.4 MnM view

- 18.1.5.4.1 Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 DRONEDEPLOY

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Deals

- 18.1.6.4 MnM view

- 18.1.7 SENTERA

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches

- 18.1.7.3.2 Deals

- 18.1.7.4 MnM view

- 18.1.8 XAG CO., LTD.

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches

- 18.1.8.3.2 Deals

- 18.1.8.4 MnM view

- 18.1.9 AUTEL ROBOTICS

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches

- 18.1.9.4 MnM view

- 18.1.10 YUNEEC

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Deals

- 18.1.10.4 MnM view

- 18.1.11 MICRODRONES

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches

- 18.1.11.3.2 Deals

- 18.1.11.3.3 Expansions

- 18.1.11.4 MnM view

- 18.1.12 DESTINUS

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions/Services offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Deals

- 18.1.12.4 MnM view

- 18.1.13 GAMAYA

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions/Services offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.13.4 MnM view

- 18.1.14 HYLIO

- 18.1.14.1 Business overview

- 18.1.14.2 Products/Solutions/Services offered

- 18.1.14.3 Recent developments

- 18.1.14.3.1 Product launches

- 18.1.14.3.2 Deals

- 18.1.14.3.3 Expansions

- 18.1.14.3.4 Other developments

- 18.1.14.4 MnM view

- 18.1.15 HIPHEN

- 18.1.15.1 Business overview

- 18.1.15.2 Products/Solutions/Services offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 Deals

- 18.1.15.4 MnM view

- 18.1.1 DJI

- 18.2 OTHER PLAYERS

- 18.2.1 JOUAV

- 18.2.2 SHENZHEN GC ELECTRONICS CO., LTD.

- 18.2.3 ARIES SOLUTIONS

- 18.2.4 WINGTRA AG

- 18.2.5 SKY-DRONES TECHNOLOGIES LTD

- 18.2.6 DELAIR

- 18.2.7 SHENZHEN GREPOW BATTERY CO., LTD.

- 18.2.8 APPLIED AERONAUTICS

- 18.2.9 VISION AERIAL, INC.

- 18.2.10 QUANTUM-SYSTEMS GMBH

19 ADJACENT AND RELATED MARKETS

- 19.1 INTRODUCTION

- 19.2 LIMITATIONS

- 19.3 DIGITAL AGRICULTURE MARKET

- 19.3.1 MARKET DEFINITION

- 19.3.2 MARKET OVERVIEW

- 19.4 PRECISION FARMING MARKET

- 19.4.1 MARKET DEFINITION

- 19.4.2 MARKET OVERVIEW

- 19.5 SMART AGRICULTURE MARKET

- 19.5.1 MARKET DEFINITION

- 19.5.2 MARKET OVERVIEW

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES CONSIDERED, 2020-2024

- TABLE 2 GLOBAL AGRICULTURE DRONES MARKET SNAPSHOT, 2025 VS. 2030 (USD MILLION)

- TABLE 3 EXPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- TABLE 4 EXPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (UNIT/TONS)

- TABLE 5 IMPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- TABLE 6 IMPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (UNIT)

- TABLE 7 AVERAGE SELLING PRICE OF AGRICULTURE DRONES OFFERED BY KEY PLAYERS, 2024 (USD/UNIT)

- TABLE 8 AVERAGE SELLING PRICE TREND OF AGRICULTURE DRONES, BY PAYLOAD CAPACITY, 2020-2024 (USD/UNIT)

- TABLE 9 AVERAGE SELLING PRICE TREND OF AGRICULTURE DRONES, BY REGION, 2020-2024 (USD MILLION)

- TABLE 10 ROLE OF PLAYERS IN AGRICULTURE DRONES ECOSYSTEM

- TABLE 11 LIST OF MAJOR PATENTS PERTAINING TO AGRICULTURE DRONES MARKET, 2020-2025

- TABLE 12 AGRICULTURE DRONES MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 US: ROBOTICS FOR AGRICULTURAL AND INDUSTRIAL USE

- TABLE 19 CANADA: ROBOTIC MACHINERY AND ROBOT USAGE

- TABLE 20 MEXICO: DRONE CATEGORIES

- TABLE 21 EU: DRONE FLYING BASED ON INTENDED OPERATIONS

- TABLE 22 EUROPE: AGRICULTURAL MACHINERY AND ROBOT PRODUCTION STANDARDS

- TABLE 23 CHINA: ARTICLES REGARDING AGRICULTURAL TECHNOLOGIES

- TABLE 24 CHINA: DRONE CLASSIFICATION BASED ON WEIGHT

- TABLE 25 IMPACT OF PORTER'S FIVE FORCES ON AGRICULTURE DRONES MARKET

- TABLE 26 INFLUENCE OF STAKEHOLDERS 0N BUYING PROCESS FOR TOP THREE OFFERINGS (%)

- TABLE 27 KEY BUYING CRITERIA FOR TOP THREE OFFERINGS

- TABLE 28 US: ADJUSTED RECIPROCAL TARIFF RATES, 2024

- TABLE 29 EXPECTED IMPACT LEVEL ON TARGET INGREDIENTS WITH RELEVANT HS CODES DUE TO TRUMP TARIFFS

- TABLE 30 EXPECTED TARIFF IMPACT ON END-USE INDUSTRIES: AGRICULTURE DRONES MARKET

- TABLE 31 AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 32 AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 33 PRECISION FARMING: AGRICULTURE DRONES MARKET, BY SUB-APPLICATION, 2020-2024 (USD MILLION)

- TABLE 34 PRECISION FARMING: AGRICULTURE DRONES MARKET, BY SUB-APPLICATION, 2025-2030 (USD MILLION)

- TABLE 35 PRECISION FARMING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 PRECISION FARMING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 FIELD MAPPING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 38 FIELD MAPPING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39 VARIABLE RATE APPLICATION: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 VARIABLE RATE APPLICATION: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 CROP SCOUTING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 42 CROP SCOUTING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 43 CROP SPRAYING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 44 CROP SPRAYING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45 OTHER PRECISION FARMING APPLICATIONS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 46 OTHER PRECISION FARMING APPLICATIONS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47 LIVESTOCK MONITORING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 48 LIVESTOCK MONITORING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 49 PRECISION FISH FARMING: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 50 PRECISION FISH FARMING: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 51 SMART GREENHOUSE: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 SMART GREENHOUSE: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53 OTHER APPLICATIONS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 54 OTHER APPLICATIONS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55 AGRICULTURE DRONES MARKET, BY COMPONENT, 2020-2024 (USD MILLION)

- TABLE 56 AGRICULTURE DRONES MARKET, BY COMPONENT, 2025-2030 (USD MILLION)

- TABLE 57 AGRICULTURE DRONES MARKET, BY SENSOR & CAMERA SYSTEMS, 2020-2024 (USD MILLION)

- TABLE 58 AGRICULTURE DRONES MARKET, BY SENSOR & CAMERA SYSTEMS, 2025-2030 (USD MILLION)

- TABLE 59 AGRICULTURE DRONES MARKET, BY NAVIGATION SYSTEMS, 2020-2024 (USD MILLION)

- TABLE 60 AGRICULTURE DRONES MARKET, BY NAVIGATION SYSTEMS, 2025-2030 (USD MILLION)

- TABLE 61 AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 62 AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 63 SMALL-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 64 SMALL-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 65 MID-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 66 MID-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 67 LARGE-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 LARGE-SIZED FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69 SUPER LARGE FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 70 SUPER LARGE FARMS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 71 AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 72 AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 73 OUTDOOR: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 74 OUTDOOR: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 75 INDOOR: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 76 INDOOR: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 77 AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 78 AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 79 AGRICULTURE DRONES MARKET, BY HARDWARE, 2020-2024 (USD MILLION)

- TABLE 80 AGRICULTURE DRONES MARKET, BY HARDWARE, 2025-2030 (USD MILLION)

- TABLE 81 AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 82 AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 83 FIXED-WING DRONES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 84 FIXED-WING DRONES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 85 ROTARY DRONE BLADES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 86 ROTARY DRONE BLADES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 87 HYBRID DRONES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 88 HYBRID DRONES: AGRICULTURE DRONES HARDWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 89 AGRICULTURE DRONES SOFTWARE MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 90 AGRICULTURE DRONES SOFTWARE MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 91 AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 92 AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 93 DATA MANAGEMENT SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 94 DATA MANAGEMENT SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 95 IMAGING SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 96 IMAGING SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 97 DATA ANALYTICS SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 98 DATA ANALYTICS SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 99 OTHER SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 100 OTHER SOFTWARE: AGRICULTURE DRONES SOFTWARE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 101 DRONE-AS-A-SERVICE: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 102 DRONE-AS-A-SERVICE: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 103 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 104 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 105 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 106 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 107 SMALL PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 108 SMALL PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 109 SMALL PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (UNITS)

- TABLE 110 SMALL PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (UNITS)

- TABLE 111 MEDIUM PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 112 MEDIUM PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 113 MEDIUM PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (UNITS)

- TABLE 114 MEDIUM PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (UNITS)

- TABLE 115 LARGE PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 116 LARGE PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 117 LARGE PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (UNITS)

- TABLE 118 LARGE PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (UNITS)

- TABLE 119 HEAVY PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 120 HEAVY PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 121 HEAVY PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (UNITS)

- TABLE 122 HEAVY PAYLOAD DRONES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (UNITS)

- TABLE 123 AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 124 AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 125 VISUAL LINE OF SIGHT (VLOS): AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 126 VISUAL LINE OF SIGHT (VLOS): AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 127 BEYOND VISUAL LINE OF SIGHT (BVLOS): AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 128 BEYOND VISUAL LINE OF SIGHT (BVLOS): AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 129 AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 130 AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 131 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY CEREALS & GRAINS, 2020-2024 (USD MILLION)

- TABLE 132 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY CEREALS & GRAINS, 2025-2030 (USD MILLION)

- TABLE 133 CEREALS & GRAINS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 134 CEREALS & GRAINS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 135 CORN: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 136 CORN: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 137 WHEAT: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 138 WHEAT: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 139 RICE: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 140 RICE: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 141 OTHER CEREALS & GRAINS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 142 OTHER CEREALS & GRAINS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 143 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY OILSEEDS & PULSES, 2020-2024 (USD MILLION)

- TABLE 144 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY OILSEEDS & PULSES, 2025-2030 (USD MILLION)

- TABLE 145 OILSEEDS & PULSES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 146 OILSEEDS & PULSES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 147 SOYBEAN: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 148 SOYBEAN: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 149 SUNFLOWER: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 150 SUNFLOWER: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 151 OTHER OILSEEDS & PULSES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 152 OTHER OILSEEDS & PULSES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 153 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY FRUITS & VEGETABLES, 2020-2024 (USD MILLION)

- TABLE 154 FARM PRODUCE: AGRICULTURE DRONES MARKET, BY FRUITS & VEGETABLES, 2025-2030 (USD MILLION)

- TABLE 155 FRUITS & VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 156 FRUITS & VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 157 POME FRUITS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 158 POME FRUITS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 159 CITRUS FRUITS: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 160 CITRUS FRUITS: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 161 BERRIES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 162 BERRIES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 163 ROOTS & TUBER VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 164 ROOTS & TUBER VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 165 LEAFY VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 166 LEAFY VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 167 OTHER FRUITS & VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 168 OTHER FRUITS & VEGETABLES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 169 OTHER CROP TYPES: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 170 OTHER CROP TYPES: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 171 GLOBAL AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 172 GLOBAL AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 173 GLOBAL AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (UNITS)

- TABLE 174 GLOBAL AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (UNITS)

- TABLE 175 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 176 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 177 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 178 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 179 HARDWARE TYPE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 180 HARDWARE TYPE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 181 HARDWARE TYPE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 182 HARDWARE TYPE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 183 SOFTWARE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 184 SOFTWARE: NORTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 185 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 186 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 187 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 188 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 189 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 190 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 191 PRECISION FARMING: NORTH AMERICA AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 192 PRECISION FARMING: NORTH AMERICA AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 193 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 194 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 195 CEREALS & GRAINS: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 196 CEREALS & GRAINS: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 197 OILSEEDS & PULSES: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 198 OILSEEDS & PULSES: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 199 FRUITS & VEGETABLES: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 200 FRUITS & VEGETABLES: NORTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 201 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 202 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 203 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 204 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 205 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 206 NORTH AMERICA: AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 207 US: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 208 US: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 209 CANADA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 210 CANADA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 211 MEXICO: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 212 MEXICO: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 213 EUROPE: AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 214 EUROPE: AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 215 EUROPE: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 216 EUROPE: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 217 HARDWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 218 HARDWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 219 HARDWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 220 HARDWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 221 SOFTWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 222 SOFTWARE TYPE: EUROPE AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 223 EUROPE: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 224 EUROPE: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 225 EUROPE: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 226 EUROPE: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 227 EUROPE: AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 228 EUROPE: AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 229 PRECISION FARMING: EUROPE AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 230 PRECISION FARMING: EUROPE AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 231 EUROPE: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 232 EUROPE: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 233 CEREALS & GRAINS: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 234 CEREALS & GRAINS: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 235 OILSEEDS & PULSES: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 236 OILSEEDS & PULSES: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 237 FRUITS & VEGETABLES: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 238 FRUITS & VEGETABLES: EUROPE AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 239 EUROPE: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 240 EUROPE: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 241 EUROPE: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 242 EUROPE: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 243 EUROPE: AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 244 EUROPE: AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 245 SPAIN: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 246 SPAIN: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 247 ITALY: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 248 ITALY: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 249 FRANCE: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 250 FRANCE: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 251 GERMANY: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 252 GERMANY: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 253 UK: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 254 UK: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 255 REST OF EUROPE: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 256 REST OF EUROPE: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 257 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 258 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 259 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 260 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 261 HARDWARE TYPE: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 262 HARDWARE TYPE: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY COUNTRY 2025-2030 (USD MILLION)

- TABLE 263 HARDWARE TYPE: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 264 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY HARDWARE, 2025-2030 (USD MILLION)

- TABLE 265 SOFTWARE TYPE: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 266 SOFTWARE TYPE: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 267 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 268 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 269 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 270 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 271 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 272 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 273 PRECISION FARMING: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 274 PRECISION FARMING: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 275 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 276 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 277 CEREALS & GRAINS: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 278 CEREALS & GRAINS: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 279 OILSEEDS & PULSES: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 280 OILSEEDS & PULSES: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 281 FRUITS & VEGETABLES: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 282 FRUITS & VEGETABLES: ASIA PACIFIC AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 283 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 284 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 285 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 286 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 287 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 288 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 289 CHINA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 290 CHINA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 291 INDIA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 292 INDIA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 293 JAPAN: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 294 JAPAN: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 295 AUSTRALIA & NEW ZEALAND: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 296 AUSTRALIA & NEW ZEALAND: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 297 REST OF ASIA PACIFIC: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 298 REST OF ASIA PACIFIC: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 299 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 300 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 301 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 302 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 303 HARDWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 304 HARDWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 305 HARDWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 306 HARDWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 307 SOFTWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 308 SOFTWARE TYPE: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 309 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 310 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 311 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 312 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 313 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 314 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 315 PRECISION FARMING: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 316 PRECISION FARMING: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 317 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 318 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 319 CEREALS & GRAINS: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 320 CEREALS & GRAINS: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 321 OILSEEDS & PULSES: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 322 OILSEEDS & PULSES: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 323 FRUITS & VEGETABLES: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 324 FRUITS & VEGETABLES: SOUTH AMERICA AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 325 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 326 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 327 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 328 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 329 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 330 SOUTH AMERICA: AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 331 BRAZIL: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 332 BRAZIL: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 333 ARGENTINA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 334 ARGENTINA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 335 REST OF SOUTH AMERICA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 336 REST OF SOUTH AMERICA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 337 ROW: AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 338 ROW: AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 339 HARDWARE TYPE: ROW AGRICULTURE DRONES MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 340 HARDWARE TYPE: ROW AGRICULTURE DRONES MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 341 ROW: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2020-2024 (USD MILLION)

- TABLE 342 ROW: AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025-2030 (USD MILLION)

- TABLE 343 HARDWARE TYPE: ROW AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 344 HARDWARE TYPE: ROW AGRICULTURE DRONES MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 345 SOFTWARE TYPE: ROW AGRICULTURE DRONES MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 346 ROW: AGRICULTURE DRONES MARKET, BY SOFTWARE, 2025-2030 (USD MILLION)

- TABLE 347 ROW: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2020-2024 (USD MILLION)

- TABLE 348 ROW: AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025-2030 (USD MILLION)

- TABLE 349 ROW: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2020-2024 (USD MILLION)

- TABLE 350 ROW: AGRICULTURE DRONES MARKET, BY FARM SIZE, 2025-2030 (USD MILLION)

- TABLE 351 ROW: AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 352 ROW: AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 353 PRECISION FARMING: ROW AGRICULTURE DRONES MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 354 PRECISION FARMING: ROW AGRICULTURE DRONES MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 355 ROW: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 356 ROW: AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 357 CEREALS & GRAINS: ROW DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 358 CEREALS & GRAINS: ROW DRONES MARKET, BY FARM PRODUCE 2025-2030 (USD MILLION)

- TABLE 359 OILSEEDS & PULSES: ROW AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 360 OILSEEDS & PULSES: ROW AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025-2030 (USD MILLION)

- TABLE 361 FRUITS & VEGETABLES: ROW AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2020-2024 (USD MILLION)

- TABLE 362 ROW: AGRICULTURE DRONES MARKET, BY FRUITS & VEGETABLES, 2025-2030 (USD MILLION)

- TABLE 363 ROW: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (USD MILLION)

- TABLE 364 ROW: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (USD MILLION)

- TABLE 365 ROW: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2020-2024 (UNITS)

- TABLE 366 ROW: AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY, 2025-2030 (UNITS)

- TABLE 367 ROW: AGRICULTURE DRONES MARKET, BY RANGE, 2020-2024 (USD MILLION)

- TABLE 368 ROW: AGRICULTURE DRONES MARKET, BY RANGE, 2025-2030 (USD MILLION)

- TABLE 369 AFRICA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 370 AFRICA: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 371 MIDDLE EAST: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 372 MIDDLE EAST: AGRICULTURE DRONES HARDWARE MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 373 OVERVIEW OF STRATEGIES DEPLOYED BY KEY MARKET PLAYERS

- TABLE 374 AGRICULTURE DRONES MARKET: DEGREE OF COMPETITION, 2024

- TABLE 375 AGRICULTURE DRONES MARKET: REGIONAL FOOTPRINT

- TABLE 376 AGRICULTURE DRONES MARKET: OFFERING TYPE FOOTPRINT

- TABLE 377 AGRICULTURE DRONES MARKET: APPLICATION FOOTPRINT

- TABLE 378 AGRICULTURE DRONES MARKET: COMPONENT FOOTPRINT

- TABLE 379 AGRICULTURE DRONES MARKET: KEY START-UPS/SMES

- TABLE 380 AGRICULTURE DRONES MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES, 2024

- TABLE 381 AGRICULTURE DRONES MARKET: PRODUCT LAUNCHES, JANUARY 2020-OCTOBER 2025

- TABLE 382 AGRICULTURE DRONES MARKET: DEALS, JANUARY 2020-OCTOBER 2025

- TABLE 383 AGRICULTURE DRONES MARKET: EXPANSIONS, JANUARY 2020-OCTOBER 2025

- TABLE 384 DJI: COMPANY OVERVIEW

- TABLE 385 DJI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 386 DJI: PRODUCT LAUNCHES

- TABLE 387 DJI.: DEALS

- TABLE 388 TRIMBLE INC.: COMPANY OVERVIEW

- TABLE 389 TRIMBLE INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 390 TRIMBLE INC.: PRODUCT LAUNCHES

- TABLE 391 TRIMBLE INC.: DEALS

- TABLE 392 PARROT DRONE SAS: COMPANY OVERVIEW

- TABLE 393 PARROT DRONE SAS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 394 YAMAHA MOTOR CO., LTD.: COMPANY OVERVIEW

- TABLE 395 YAMAHA MOTOR CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 396 YAMAHA MOTOR CO., LTD.: PRODUCT LAUNCHES

- TABLE 397 YAMAHA MOTOR CO., LTD.: DEALS

- TABLE 398 YAMAHA MOTOR CO., LTD.: EXPANSIONS

- TABLE 399 AGEAGLE AERIAL SYSTEMS INC.: COMPANY OVERVIEW

- TABLE 400 AGEAGLE AERIAL SYSTEMS INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 401 AGEAGLE AERIAL SYSTEMS INC: PRODUCT LAUNCHES

- TABLE 402 AGEAGLE AERIAL SYSTEMS INC: DEALS

- TABLE 403 DRONEDEPLOY: COMPANY OVERVIEW

- TABLE 404 DRONEDEPLOY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 405 DRONEDEPLOY: DEALS

- TABLE 406 SENTERA: COMPANY OVERVIEW

- TABLE 407 SENTERA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 408 SENTERA: PRODUCT LAUNCHES

- TABLE 409 SENTERA: DEALS

- TABLE 410 XAG CO., LTD.: COMPANY OVERVIEW

- TABLE 411 XAG CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 412 XAG CO., LTD.: PRODUCT LAUNCHES

- TABLE 413 XAG CO., LTD.: DEALS

- TABLE 414 AUTEL ROBOTICS: COMPANY OVERVIEW

- TABLE 415 AUTEL ROBOTICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 416 AUTEL ROBOTICS: PRODUCT LAUNCHES

- TABLE 417 YUNEEC: COMPANY OVERVIEW

- TABLE 418 YUNEEC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 419 YUNEEC: DEALS

- TABLE 420 MICRODRONES: COMPANY OVERVIEW

- TABLE 421 MICRODRONES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 422 MICRODRONES: PRODUCT LAUNCHES

- TABLE 423 MICRODRONES: DEALS

- TABLE 424 MICRODRONES: EXPANSIONS

- TABLE 425 DESTINUS: COMPANY OVERVIEW

- TABLE 426 DESTINUS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 427 DESTINUS: DEALS

- TABLE 428 GAMAYA: COMPANY OVERVIEW

- TABLE 429 GAMAYA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 430 GAMAYA: DEALS

- TABLE 431 HYLIO: COMPANY OVERVIEW

- TABLE 432 HYLIO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 433 HYLIO: PRODUCT LAUNCHES

- TABLE 434 HYLIO: DEALS

- TABLE 435 HYLIO: EXPANSIONS

- TABLE 436 HYLIO: OTHER DEVELOPMENTS

- TABLE 437 HIPHEN: COMPANY OVERVIEW

- TABLE 438 HIPHEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 439 HIPHEN: DEALS

- TABLE 440 JOUAV: COMPANY OVERVIEW

- TABLE 441 SHENZHEN GC ELECTRONICS CO., LTD.: COMPANY OVERVIEW

- TABLE 442 ARIES SOLUTIONS: COMPANY OVERVIEW

- TABLE 443 WINGTRA AG: COMPANY OVERVIEW

- TABLE 444 SKY-DRONES TECHNOLOGIES LTD: COMPANY OVERVIEW

- TABLE 445 DELAIR: COMPANY OVERVIEW

- TABLE 446 SHENZHEN GREPOW BATTERY CO., LTD.: COMPANY OVERVIEW

- TABLE 447 APPLIED AERONAUTICS: COMPANY OVERVIEW

- TABLE 448 VISION AERIAL, INC.: COMPANY OVERVIEW

- TABLE 449 QUANTUM-SYSTEMS GMBH: COMPANY OVERVIEW

- TABLE 450 ADJACENT MARKETS TO AGRICULTURE DRONES MARKET

- TABLE 451 DIGITAL AGRICULTURE MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 452 DIGITAL AGRICULTURE MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 453 PRECISION FARMING MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 454 PRECISION FARMING MARKET, BY APPLICATION, 2023-2031 (USD MILLION)

- TABLE 455 SMART AGRICULTURE MARKET, BY OFFERING, 2019-2022 (USD MILLION)

- TABLE 456 SMART AGRICULTURE MARKET, BY OFFERING, 2023-2028 (USD MILLION)

List of Figures

- FIGURE 1 MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 AGRICULTURE DRONES MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 AGRICULTURE DRONES MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 5 AGRICULTURE DRONES MARKET SIZE ESTIMATION (DEMAND SIDE)

- FIGURE 6 AGRICULTURE DRONES MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 7 AGRICULTURE DRONES MARKET SIZE ESTIMATION, BY TYPE (SUPPLY SIDE)

- FIGURE 8 DATA TRIANGULATION

- FIGURE 9 AGRICULTURE DRONES MARKET, BY FARM PRODUCE, 2025 VS. 2030 (USD MILLION)

- FIGURE 10 AGRICULTURE DRONES MARKET, BY OFFERING TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 11 AGRICULTURE DRONES MARKET, BY PAYLOAD, 2025 VS. 2030 (USD MILLION)

- FIGURE 12 AGRICULTURE DRONES MARKET, BY RANGE, 2025 VS. 2030 (USD MILLION)

- FIGURE 13 AGRICULTURE DRONES MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 AGRICULTURE DRONES MARKET, BY COMPONENT, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 AGRICULTURE DRONES MARKET SHARE AND GROWTH RATE, BY REGION, 2024 (BY VALUE)

- FIGURE 17 INCREASING DEMAND FOR HIGH-QUALITY CROP YIELD TO DRIVE MARKET

- FIGURE 18 CHINA AND HARDWARE SEGMENT TO ACCOUNT FOR A SIGNIFICANT SHARE IN 2025

- FIGURE 19 HARDWARE SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 20 LARGE SIZED FARMS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 21 MEDIUM PAYLOAD SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 22 CEREALS & GRAINS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 23 PRECISION FARMING SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 24 VLOS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 25 CHINA TO DOMINATE AGRICULTURE DRONES MARKET IN 2025

- FIGURE 26 PER CAPITA ARABLE LAND, 2002-2022

- FIGURE 27 SMARTPHONE PENETRATION, BY REGION, 2019 VS. 2025

- FIGURE 28 GLOBAL GNSS DEMAND, 2021 VS. 2031 (EUR BILLION)

- FIGURE 29 AGRICULTURE DRONES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 30 ADOPTION OF GEN AI IN AGRICULTURE DRONES

- FIGURE 31 AGRICULTURE DRONES MARKET: VALUE CHAIN ANALYSIS

- FIGURE 32 EXPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- FIGURE 33 IMPORT VALUE OF HS CODE 8806, BY KEY COUNTRY, 2022-2024 (USD THOUSAND)

- FIGURE 34 AGRICULTURE DRONES MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 35 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PAYLOAD CAPACITY, 2024

- FIGURE 36 AVERAGE SELLING PRICE TREND, BY PAYLOAD CAPACITY, 2020-2024

- FIGURE 37 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024

- FIGURE 38 AGRICULTURE DRONES ECOSYSTEM

- FIGURE 39 TRENDS/DISRUPTING IMPACTING CUSTOMER BUSINESS

- FIGURE 40 NUMBER OF PATENTS GRANTED FOR AGRICULTURE DRONES MARKET, 2014-2025

- FIGURE 41 REGIONAL ANALYSIS OF PATENTS GRANTED FOR AGRICULTURE DRONE MARKET, 2014-2025

- FIGURE 42 AGRICULTURE DRONES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 43 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE OFFERINGS

- FIGURE 44 KEY BUYING CRITERIA FOR TOP THREE OFFERINGS

- FIGURE 45 INVESTMENT & FUNDING SCENARIO

- FIGURE 46 PRECISION FARMING TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 47 NAVIGATION SYSTEMS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 48 LARGE-SIZED FARMS TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 49 OUTDOOR SEGMENT TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 50 HARDWARE SEGMENT TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 51 MEDIUM PAYLOAD DRONES TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 52 VISUAL LINE OF SIGHT (VLOS) DRONES TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 53 CEREALS & GRAINS TO DOMINATE AGRICULTURE DRONES MARKET DURING FORECAST PERIOD

- FIGURE 54 MEXICO TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 55 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 56 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 57 REVENUE ANALYSIS FOR KEY COMPANIES IN LAST 5 YEARS, 2020-2024 (USD MILLION)

- FIGURE 58 SHARE OF LEADING PLAYERS IN AGRICULTURE DRONES MARKET, 2024

- FIGURE 59 AGRICULTURE DRONES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 60 AGRICULTURE DRONES MARKET: COMPANY FOOTPRINT

- FIGURE 61 AGRICULTURE DRONES MARKET: COMPANY EVALUATION MATRIX (START-UPS/SMES), 2024

- FIGURE 62 COMPANY VALUATION OF KEY VENDORS

- FIGURE 63 FINANCIAL METRICS OF KEY VENDORS

- FIGURE 64 BRAND/PRODUCT COMPARISON

- FIGURE 65 TRIMBLE INC.: COMPANY SNAPSHOT

- FIGURE 66 PARROT DRONE SAS: COMPANY SNAPSHOT

- FIGURE 67 YAMAHA MOTOR CO., LTD.: COMPANY SNAPSHOT

- FIGURE 68 AGEAGLE AERIAL SYSTEMS INC: COMPANY SNAPSHOT