PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1819090

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1819090

Generative AI Cybersecurity Market by Generative AI-based Cybersecurity (SIEM, Risk Assessment, Threat Intelligence), Cybersecurity Software for Generative AI (AI Model Security), Security Type (Data Encryption, Access Control) - Global Forecast to 2031

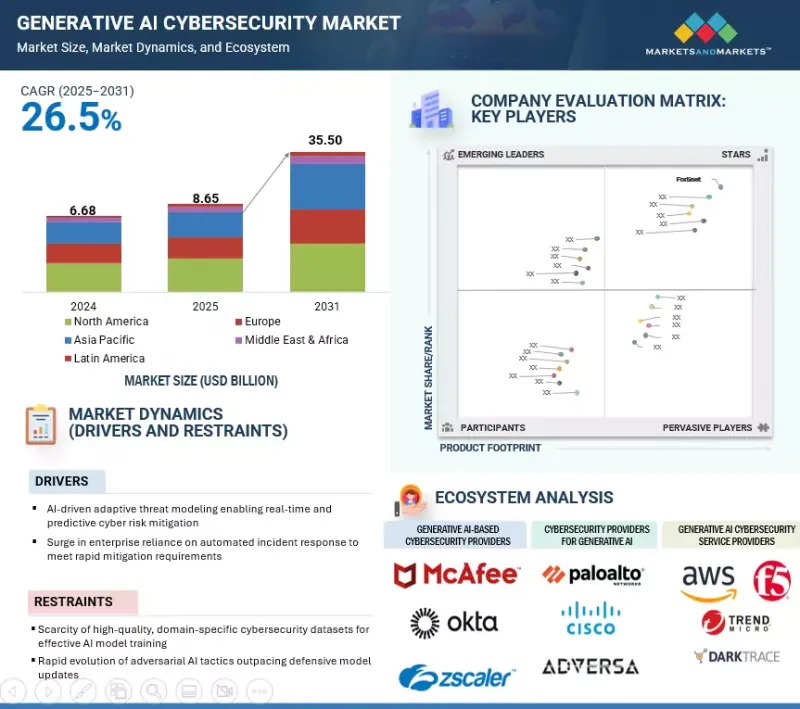

The generative AI cybersecurity market is anticipated to witness a compound annual growth rate (CAGR) of 26.5% over the forecast period, reaching USD 35.50 billion by 2031 from an estimated USD 8.65 billion in 2025. The market is driven by the rise in AI supply chain attacks targeting third-party model repositories, APIs, and plugins, which is pushing enterprises to adopt model provenance verification and code signing to secure AI assets.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | USD (Million) |

| Segments | Offering, Generative AI-based Cybersecurity Software, Cybersecurity Software for Generative AI, Security Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Additionally, the growing use of model-as-a-service in multi-tenant cloud environments is increasing demand for confidential computing and secure enclave execution to protect sensitive AI workloads. However, the market also faces a significant restraint as malicious actors exploit generative AI to automate phishing campaigns, create deepfakes, and develop advanced malware. This dual-use challenge forces vendors to continually evolve defensive strategies to stay ahead of adversarial AI threats while balancing innovation and security.

"Risk assessment software leads growth, driving proactive threat mitigation"

Risk assessment software within the generative AI cybersecurity ecosystem is projected to record the highest CAGR over the forecast period, fueled by its critical role in proactive threat prevention and compliance-driven decision-making. Generative AI enhances traditional risk assessment by simulating complex attack scenarios, predicting cascading impacts across interconnected systems, and identifying latent vulnerabilities that conventional tools may overlook. The technology enables continuous, adaptive scoring of cyber risks based on real-time telemetry, threat intelligence feeds, and contextual business impact, allowing enterprises to prioritize remediation efforts with precision. Industries with stringent compliance frameworks, such as BFSI, healthcare, and critical infrastructure, are accelerating adoption to meet evolving regulatory expectations like the US SEC's cyber incident disclosure rules and the EU Digital Operational Resilience Act (DORA). Moreover, AI-driven risk assessment platforms are being integrated with Security Orchestration, Automation, and Response (SOAR) systems to automate policy enforcement and reduce decision latency during incidents. By leveraging generative models to evaluate risks in dynamic environments, vendors can offer predictive insights that materially improve security posture and operational resilience. The combination of regulatory pressure, operational efficiency gains, and the ability to quantify and communicate cyber risk in business terms positions this software segment for sustained high-growth momentum.

"Static application security testing to hold largest market as AI-centric code security becomes mission-critical"

Static Application Security Testing (SAST) is estimated to capture the largest market share within application security types in 2025, driven by its critical role in securing AI-integrated software development pipelines and ensuring code integrity before deployment. The increasing adoption of secure-by-design principles in enterprise AI initiatives has elevated SAST from a compliance-focused measure to a strategic necessity, especially as regulatory bodies tighten oversight on AI-enabled applications handling sensitive data. Unlike dynamic testing, SAST enables early detection of vulnerabilities at the source code level, significantly reducing remediation costs and minimizing the risk of exploited flaws reaching production environments. In sectors such as BFSI, healthcare, and government, where AI applications process high-value and regulated data, SAST adoption is accelerating in parallel with generative AI deployments, ensuring robust protection against injection attacks, insecure dependencies, and code-level data leaks. Moreover, the growing integration of AI coding assistants and automated DevSecOps pipelines is expanding the demand for SAST tools capable of handling AI-generated code, addressing unique vulnerabilities introduced by large language model-assisted programming. Leading security vendors are embedding AI-driven analytics into SAST platforms to improve vulnerability prioritization and reduce false positives, further enhancing operational efficiency and developer adoption. These combined factors position SAST as the dominant force in the 2025 application security landscape.

"Asia Pacific to witness rapid market growth fueled by innovation and emerging technologies, while North America leads in market size"

North America is estimated to account for the largest share of the generative AI cybersecurity market in 2025, underpinned by its mature technology ecosystem, strong enterprise adoption rates, and early regulatory engagement in AI governance. The region benefits from the presence of leading cybersecurity vendors, robust venture capital activity, and a concentration of high-value industries such as BFSI, healthcare, and defense, where AI-driven security solutions are rapidly embedded into operational frameworks. Government-backed initiatives, such as the US Executive Order on AI and sector-specific compliance mandates, are accelerating investment in advanced AI threat detection, incident response automation, and AI-assisted risk assessment platforms. In parallel, Asia Pacific is poised to record the fastest CAGR during the forecast period, driven by rapid digital transformation, large-scale cloud adoption, and a growing need to counter evolving cyber threats targeting expanding digital infrastructures. Countries such as China, India, Japan, and South Korea are investing heavily in AI R&D, supported by government programs and strategic public-private partnerships. The region's expanding base of SMEs and startups is leveraging generative AI for both offensive and defensive cybersecurity innovation, while hyperscale cloud providers are localizing AI security services to address diverse compliance environments. This combination of high-growth adoption patterns in the Asia Pacific and entrenched market dominance in North America is shaping a dual-center growth model for the global generative AI cybersecurity landscape.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the generative AI cybersecurity market.

- By Company: Tier I - 35%, Tier II - 45%, and Tier III - 20%

- By Designation: C Level - 35%, Director Level - 25%, and others - 40%

- By Region: North America - 42%, Europe - 20%, Asia Pacific - 25%, Middle East & Africa - 8%, and Latin America - 5%

The report includes the study of key players offering generative AI cybersecurity solutions and services. It profiles major vendors in the generative AI cybersecurity market. The major market players include Microsoft (US), IBM (US), Google (US), SentinelOne (US), AWS (US), NVIDIA (US), Cisco (US), CrowdStrike (US), Fortinet (US), Zscaler (US), Trend Micro (Japan), Palo Alto Networks (US), BlackBerry (Canada), Darktrace (UK), F5 (US), Okta (US), Sangfor (China), SecurityScorecard (US), Sophos (UK), Broadcom (US), Trellix (US), Veracode (US), LexisNexis (US), Abnormal Security (US), Adversa AI (Israel), Aquasec (US), BigID (US), Checkmarx (US), Cohesity (US), Credo AI (US), NeuralTrust (Spain), Cybereason (US), DeepKeep (Israel), Elastic NV (US), Flashpoint (US), Lakera (US), MOSTLY AI (Austria), Recorded Future (US), Secureframe (US), Skyflow (US), SlashNext (US), Snyk (US), Tenable (US), TrojAI (Canada), VirusTotal (Spain), XenonStack (UAE), and Zerofox (US).

Research Coverage

This research report covers the generative AI cybersecurity market, which has been segmented based on offering, generative AI-based cybersecurity software, cybersecurity software for generative AI, security type, and end user. The offering segment consists of software and services. The generative AI-based cybersecurity solutions segment consists of threat detection & intelligence software, risk assessment software, exposure management software, phishing simulation & prevention software, remediation guidance software, threat hunting platforms, and code analysis software. The cybersecurity solutions for the generative AI segment include generative AI training data security software, generative AI model security software, generative AI infrastructure security software, and generative AI application security software. The security type segment consists of generative AI training data security software, generative AI model security software, generative AI infrastructure security software, and generative AI application security software. The end user segment consists of generative AI-based cybersecurity end users and cybersecurity for generative AI end users. The regional analysis of the generative AI cybersecurity market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall generative AI cybersecurity market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Rising frequency and sophistication of AI-driven cyberattacks accelerating adoption of AI-powered defense tools, Operational efficiency gains through AI-assisted Security Operations Centers (AI-SOC) reducing alert fatigue and response times, Escalating zero-day vulnerabilities necessitating rapid AI-enabled detection and remediation, and Growing demand for AI-powered behavioral anomaly detection to combat insider threats), restraints (Lack of standardized benchmarks for evaluating AI cybersecurity solutions, and Uncertainty around liability in AI-led automated security actions), opportunities (Adoption of Zero Trust for AI frameworks for validating AI-generated outputs, Leveraging AI for real-time detection of adversarial AI attacks on critical infrastructure, and Development of AI-driven penetration testing and vulnerability assessment platforms), and challenges (Exploitation of prompt injection and model manipulation techniques to bypass safeguards, and Growth of AI-enabled deepfake fraud targeting enterprises and critical infrastructure).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the generative AI cybersecurity market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the generative AI cybersecurity market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the generative AI cybersecurity market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and offerings of leading players like Microsoft (US), IBM (US), Google (US), SentinelOne (US), AWS (US), NVIDIA (US), Cisco (US), CrowdStrike (US), Fortinet (US), Zscaler (US), Trend Micro (Japan), Palo Alto Networks (US), BlackBerry (Canada), Darktrace (UK), F5 (US), Okta (US), Sangfor (China), SecurityScorecard (US), Sophos (UK), Broadcom (US), Trellix (US), Veracode (US), LexisNexis (US), Abnormal Security (US), Adversa AI (Israel), Aquasec (US), BigID (US), Checkmarx (US), Cohesity (US), Credo AI (US), NeuralTrust (Spain), Cybereason (US), DeepKeep (Israel), Elastic NV (US), Flashpoint (US), Lakera (US), MOSTLY AI (Austria), Recorded Future (US), Secureframe (US), Skyflow (US), SlashNext (US), Snyk (US), Tenable (US), TrojAI (Canada), VirusTotal (Spain), XenonStack (UAE), and Zerofox (US), among others, in the generative AI cybersecurity market. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION AND SCOPE

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN GENERATIVE AI CYBERSECURITY MARKET

- 4.2 GENERATIVE AI CYBERSECURITY MARKET: TOP THREE SECURITY TYPES

- 4.3 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING AND SECURITY TYPE

- 4.4 GENERATIVE AI CYBERSECURITY MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising frequency and sophistication of AI-driven cyberattacks

- 5.2.1.2 Operational efficiency gains through AI-assisted Security Operations Centers (AI-SOC), reducing alert fatigue and response times

- 5.2.1.3 Escalating zero-day vulnerabilities, necessitating rapid AI-enabled detection and remediation

- 5.2.1.4 Growing demand for AI-powered behavioral anomaly detection to combat insider threats

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of standardized benchmarks for evaluation of AI cybersecurity solutions

- 5.2.2.2 Uncertainty around liability in AI-led automated security actions

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Adoption of Zero Trust for AI frameworks to validate AI-generated outputs

- 5.2.3.2 Leveraging AI for real-time detection of adversarial AI attacks on critical infrastructure

- 5.2.3.3 Development of AI-driven penetration testing and vulnerability assessment platforms

- 5.2.4 CHALLENGES

- 5.2.4.1 Exploitation of prompt injection and model manipulation techniques to bypass safeguards

- 5.2.4.2 Proliferation of AI-enabled deepfake fraud targeting enterprises and critical infrastructure

- 5.2.1 DRIVERS

- 5.3 EVOLUTION OF GENERATIVE AI CYBERSECURITY

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 GENERATIVE AI-BASED CYBERSECURITY PROVIDERS

- 5.5.2 CYBERSECURITY PROVIDERS FOR GENERATIVE AI

- 5.5.3 GENERATIVE AI CYBERSECURITY SERVICE PROVIDERS

- 5.5.4 SECURITY TYPES

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 ZEROFOX PROVIDES ACTIONABLE INTELLIGENCE TO SHORE UP SIMPLY BUSINESS'S INFORMATION SECURITY

- 5.7.2 POMELO STAYS SECURE AMIDST RAPID GROWTH WITH SNYK

- 5.7.3 EVOCABANK HELPS NOKIA PROTECT MILLIONS OF FOLLOWERS

- 5.7.4 CARNIVAL CORPORATION CHARTS A SAFER COURSE WITH CYBERARK

- 5.7.5 IBM USES PALO ALTO TO PROTECTS ITS AI SYSTEMS

- 5.7.6 OPENAI USES OKTA TO SAFEGUARD ITSELF

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Adversarial machine learning

- 5.8.1.2 Federated learning security

- 5.8.1.3 Differential privacy

- 5.8.1.4 Homomorphic encryption

- 5.8.1.5 Secure multi-party computation

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Blockchain

- 5.8.2.2 Zero trust architecture

- 5.8.2.3 Endpoint detection & response

- 5.8.2.4 Vulnerability management

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Quantum computing

- 5.8.3.2 DevSecOps

- 5.8.3.3 Forensics & incident response

- 5.8.3.4 Big data analytics

- 5.8.1 KEY TECHNOLOGIES

- 5.9 REGULATORY LANDSCAPE

- 5.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.2 KEY REGULATIONS

- 5.9.2.1 North America

- 5.9.2.1.1 Executive Order on AI (US)

- 5.9.2.1.2 NIST AI Risk Management Framework (under the NDAA)

- 5.9.2.1.3 National AI Risk Management Framework

- 5.9.2.1.4 Artificial Intelligence and Data Act (AIDA)

- 5.9.2.1.5 Kids Online Safety Act (KOSA)

- 5.9.2.1.6 Canadian Centre for Cyber Security

- 5.9.2.1.7 Privacy Guidelines

- 5.9.2.2 Europe

- 5.9.2.2.1 Regulation (EU) 2024/1689 - Artificial Intelligence Act (AI Act)

- 5.9.2.2.2 Directive (EU) 2022/2555 - NIS 2 Directive

- 5.9.2.2.3 Regulation (EU) 2024/2847 - Cyber Resilience Act (CRA)

- 5.9.2.2.4 Regulation (EU) 2024/903 - Cyber Solidarity Act (CSA)

- 5.9.2.3 Asia Pacific

- 5.9.2.3.1 Model AI Governance Framework (Singapore)

- 5.9.2.3.2 AI Guidelines for Business Version 1.0 (Japan)

- 5.9.2.3.3 Basic Law for Promoting Responsible AI (Japan, proposed)

- 5.9.2.3.4 Act on Promotion of the AI Industry and Framework for Establishing Trustworthy AI (South Korea)

- 5.9.2.4 Middle East & Africa

- 5.9.2.4.1 UAE Strategy for Artificial Intelligence 2031

- 5.9.2.4.2 National AI Programme

- 5.9.2.4.3 African Union Convention on Cyber Security and Personal Data Protection (Malabo Convention)

- 5.9.2.4.4 National Strategy for Data and AI (NSDAI)

- 5.9.2.4.5 Saudi Data and Artificial Intelligence Authority (SDAIA)

- 5.9.2.5 Latin America

- 5.9.2.5.1 Bill No. 2,338/2023 - Proposed Law on Artificial Intelligence (Brazil)

- 5.9.2.5.2 National Artificial Intelligence Strategy (EBIA) (Brazil)

- 5.9.2.5.3 National Policy on Exploitation of Data (Big Data) (Colombia)

- 5.9.2.5.4 AI Regulation Bill (Colombia)

- 5.9.2.1 North America

- 5.10 PATENT ANALYSIS

- 5.10.1 METHODOLOGY

- 5.10.2 PATENTS FILED, BY DOCUMENT TYPE

- 5.10.3 INNOVATION AND PATENT APPLICATIONS

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY OFFERING, 2025

- 5.11.2 AVERAGE SELLING PRICE, BY SECURITY TYPE, 2025

- 5.12 KEY CONFERENCES AND EVENTS (2025-2026)

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF NEW ENTRANTS

- 5.13.2 THREAT OF SUBSTITUTES

- 5.13.3 BARGAINING POWER OF SUPPLIERS

- 5.13.4 BARGAINING POWER OF BUYERS

- 5.13.5 INTENSITY OF COMPETITION RIVALRY

- 5.14 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.15 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.15.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6 GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 6.2 SOFTWARE, BY TYPE

- 6.2.1 STRENGTHENING OF GENERATIVE AI SECURITY WITH PURPOSE-BUILT SOFTWARE

- 6.2.2 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE

- 6.2.3 CYBERSECURITY SOFTWARE FOR GENERATIVE AI

- 6.3 SOFTWARE, BY DEPLOYMENT MODE

- 6.3.1 OPTIMIZING CYBER DEFENSE WITH FLEXIBLE DEPLOYMENT MODES

- 6.3.2 CLOUD

- 6.3.3 ON-PREMISES

- 6.4 SERVICES

- 6.4.1 RESILIENT GENERATIVE AI CYBERSECURITY ENABLED THROUGH COMPREHENSIVE SERVICES

- 6.4.2 PROFESSIONAL SERVICES

- 6.4.2.1 Training & consulting

- 6.4.2.2 System integration & implementation

- 6.4.2.3 Support & maintenance

- 6.4.3 MANAGED SERVICES

7 CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE

- 7.1 INTRODUCTION

- 7.1.1 CYBERSECURITY SOFTWARE FOR GENERATIVE AI: MARKET DRIVERS

- 7.2 GENERATIVE AI TRAINING DATA SECURITY SOFTWARE

- 7.2.1 ENSURING RELIABILITY AND COMPLIANCE WITH TRAINING DATA SECURITY

- 7.2.2 DATA INTEGRITY VERIFICATION

- 7.2.3 SECURE DATA AUGMENTATION

- 7.2.4 AUTOMATED DATA CLEANING

- 7.2.5 DATA QUALITY MONITORING

- 7.2.6 DATA ANONYMIZATION

- 7.3 GENERATIVE AI MODEL SECURITY SOFTWARE

- 7.3.1 SHIELDING GENERATIVE AI MODELS AGAINST EVOLVING THREATS

- 7.3.2 MODEL INTEGRITY

- 7.3.3 ADVERSARIAL TRAINING & TESTING

- 7.3.4 SECURE MODEL TRAINING ENVIRONMENTS

- 7.3.5 MODEL DRIFT & BIAS DETECTION

- 7.3.6 ROBUSTNESS TESTING

- 7.4 GENERATIVE AI INFRASTRUCTURE SECURITY SOFTWARE

- 7.4.1 ENSURING RESILIENT FOUNDATIONS FOR LARGE-SCALE GENERATIVE AI OPERATIONS

- 7.4.2 CONTINUOUS MONITORING

- 7.4.3 AUTOMATED SECURITY PATCHING

- 7.4.4 SECURE API MANAGEMENT

- 7.4.5 REAL-TIME THREAT DETECTION

- 7.4.6 SECURITY AUDITS

- 7.5 GENERATIVE AI APPLICATION SECURITY SOFTWARE

- 7.5.1 DEFENDING GENERATIVE AI APPLICATIONS FROM ATTACK VECTORS

- 7.5.2 PROMPT INJECTION SECURITY

- 7.5.3 DATA LEAKAGE PREVENTION

- 7.5.4 USER AUTHENTICATION & ACCESS CONTROL

- 7.5.5 MONITORING & ANOMALY DETECTION

- 7.5.6 ETHICAL AI GOVERNANCE

8 GENERATIVE AI CYBERSECURITY MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.1.1 END USERS: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 8.2 END USERS: GENERATIVE AI-BASED CYBERSECURITY

- 8.2.1 DRIVING ADVANCED THREAT MITIGATION WITH GENERATIVE AI

- 8.2.2 GOVERNMENT & DEFENSE

- 8.2.3 BFSI

- 8.2.4 IT & ITES

- 8.2.5 HEALTHCARE & LIFE SCIENCES

- 8.2.6 RETAIL & ECOMMERCE

- 8.2.7 MANUFACTURING

- 8.2.8 ENERGY & UTILITIES

- 8.2.9 TELECOMMUNICATIONS

- 8.2.10 AUTOMOTIVE, TRANSPORTATION, AND LOGISTICS

- 8.2.11 MEDIA & ENTERTAINMENT

- 8.2.12 OTHER END USERS

- 8.3 END USERS: CYBERSECURITY FOR GENERATIVE AI

- 8.3.1 PROTECTING GENERATIVE AI SERVICES TO SAFEGUARD END USERS

- 8.3.2 CLOUD HYPERSCALERS

- 8.3.3 MANAGED SECURITY SERVICE PROVIDERS

- 8.3.4 GENERATIVE AI PROVIDERS

- 8.3.4.1 Foundation model/LLM developers

- 8.3.4.2 Data annotators

- 8.3.4.3 Content creation platform providers

- 8.3.4.4 Generative AI-as-a-service provider

9 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET DRIVERS

- 9.2 THREAT DETECTION & INTELLIGENCE SOFTWARE

- 9.2.1 OFFERS ENHANCED CYBERSECURITY PRECISION AND SPEED

- 9.2.2 AUTOMATED THREAT ANALYSIS

- 9.2.3 SECURITY INFORMATION & EVENT MANAGEMENT

- 9.2.4 AI-NATIVE SECURITY ANALYSIS

- 9.2.5 THREAT CORRELATION

- 9.2.6 THREAT INTELLIGENCE

- 9.3 RISK ASSESSMENT SOFTWARE

- 9.3.1 PREDICTIVE RISK ASSESSMENT STRENGTHENS GENERATIVE AI CYBERSECURITY POSTURE

- 9.3.2 AUTOMATED RISK INSIGHTS

- 9.3.3 IMPACT ANALYSIS

- 9.3.4 RISK INTELLIGENCE

- 9.3.5 COMPLIANCE AUTOMATION

- 9.3.6 OTHER RISK ASSESSMENT SOFTWARE

- 9.4 EXPOSURE MANAGEMENT SOFTWARE

- 9.4.1 OFFERS AI-POWERED VULNERABILITY OVERSIGHT FOR STRONGER CYBERSECURITY

- 9.4.2 VULNERABILITY ANALYSIS

- 9.4.3 EXPOSURE PRIORITIZATION

- 9.4.4 AUTOMATED EXPOSURE DETECTION

- 9.4.5 INCIDENT RESPONSE

- 9.4.6 OTHER EXPOSURE MANAGEMENT SOFTWARE

- 9.5 PHISHING SIMULATION & PREVENTION SOFTWARE

- 9.5.1 SIMULATES REALISTIC PHISHING SCENARIOS WITH GENERATIVE AI

- 9.5.2 PHISHING SIMULATION CAMPAIGNS

- 9.5.3 PHISHING ATTACK ANALYSIS

- 9.5.4 DEEPFAKE DETECTION

- 9.5.5 FRAUD PREVENTION

- 9.5.6 SOCIAL ENGINEERING DETECTION

- 9.6 REMEDIATION GUIDANCE SOFTWARE

- 9.6.1 ENABLES QUICK AND INFORMED RESPONSE WITH GENERATIVE AI REMEDIATION GUIDANCE

- 9.6.2 AUTOMATED REMEDIATION

- 9.6.3 INTERACTIVE REMEDIATION SUPPORT

- 9.6.4 PROACTIVE THREAT MANAGEMENT

- 9.6.5 COMPLIANCE REMEDIATION

- 9.6.6 OTHER REMEDIATION GUIDANCE SOFTWARE

- 9.7 THREAT HUNTING PLATFORMS

- 9.7.1 CYBER DEFENSE ENHANCED BY PREDICTING AND NEUTRALIZING STEALTH ATTACKS

- 9.7.2 REAL-TIME THREAT ANALYSIS

- 9.7.3 NATURAL LANGUAGE QUERY INTERFACE

- 9.7.4 BEHAVIOR ANALYSIS

- 9.7.5 RESPONSE AUTOMATION

- 9.7.6 OTHER THREAT HUNTING PLATFORMS

- 9.8 CODE ANALYSIS SOFTWARE

- 9.8.1 SECURES DEVELOPMENT PIPELINES WITH GENERATIVE AI PRECISION

- 9.8.2 CODE SNIPPET ANALYSIS

- 9.8.3 SOURCE CODE PROTECTION

- 9.8.4 VULNERABILITY DETECTION

- 9.8.5 AUTOMATED CODE REVIEW

- 9.8.6 COMPLIANCE CHECKS

10 GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE

- 10.1 INTRODUCTION

- 10.1.1 SECURITY TYPE: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 10.2 DATABASE SECURITY

- 10.2.1 SECURES GENERATIVE AI PIPELINES WITH ADVANCED DATABASE PROTECTION

- 10.2.2 DATA LOSS PREVENTION

- 10.2.3 DATA USAGE MONITORING

- 10.2.4 DATA COMPLIANCE & GOVERNANCE

- 10.2.5 DATA ENCRYPTION

- 10.2.6 DATA MASKING & TOKENIZATION

- 10.2.7 ACCESS CONTROL

- 10.3 NETWORK SECURITY

- 10.3.1 OPTIMIZING SECURE CONNECTIVITY FOR GENERATIVE AI WORKLOADS

- 10.3.2 NETWORK TRAFFIC ANALYSIS

- 10.3.3 SECURE ACCESS SERVICE EDGE

- 10.3.4 ZERO TRUST NETWORK ACCESS

- 10.3.5 FIREWALLS

- 10.3.6 INTRUSION DETECTION/PREVENTION SYSTEMS

- 10.3.7 VPNS & SECURE TUNNELING

- 10.4 ENDPOINT SECURITY

- 10.4.1 OPTIMIZING THREAT DETECTION AND RESPONSE ACROSS GENERATIVE AI ENDPOINTS

- 10.4.2 ENDPOINT DETECTION & RESPONSE

- 10.4.3 ENDPOINT PROTECTION PLATFORMS

- 10.5 APPLICATION SECURITY

- 10.5.1 SECURING GENERATIVE AI WORKFLOWS WITH END-TO-END APPLICATION PROTECTION

- 10.5.2 STATIC APPLICATION SECURITY TESTING

- 10.5.3 DYNAMIC APPLICATION SECURITY TESTING

- 10.5.4 LLM SECURITY

- 10.5.5 RUNTIME PROTECTION

- 10.5.6 INCIDENT RESPONSE & RECOVERY

- 10.5.7 GOVERNANCE, RISK, AND COMPLIANCE

11 GENERATIVE AI CYBERSECURITY MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.3 US

- 11.2.3.1 Market driven by robust technological infrastructure and culture of innovation

- 11.2.4 CANADA

- 11.2.4.1 Recent advancements and presence of leading companies to drive market

- 11.3 EUROPE

- 11.3.1 EUROPE: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 Commitment to leveraging AI to tackle evolving cyber threats to fuel growth

- 11.3.4 GERMANY

- 11.3.4.1 Active government promotion of AI research to boost market

- 11.3.5 FRANCE

- 11.3.5.1 Emphasis on R&D to drive market

- 11.3.6 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 AI-driven cybersecurity solutions that offer robust defense against digital threats - key market driver

- 11.4.4 INDIA

- 11.4.4.1 Market trajectory characterized by significant investment in research and development

- 11.4.5 JAPAN

- 11.4.5.1 International regulatory framework and promotion of safe and trustworthy AI usage - key drivers

- 11.4.6 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 SAUDI ARABIA

- 11.5.3.1 Evolving to support growth of generative AI and cybersecurity

- 11.5.4 UAE

- 11.5.4.1 Focus on establishment of cutting-edge AI and cybersecurity infrastructure

- 11.5.5 REST OF MIDDLE EAST

- 11.5.6 AFRICA

- 11.5.6.1 Development of new AI models and technologies tailored to unique cybersecurity challenges to drive market

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: GENERATIVE AI CYBERSECURITY MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Companies continue to invest in generative AI solutions and push boundaries of innovation

- 11.6.4 MEXICO

- 11.6.4.1 Government proactively addressing data privacy and security concerns

- 11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.4.1 MARKET RANKING ANALYSIS

- 12.5 PRODUCT COMPARATIVE ANALYSIS

- 12.5.1 PRODUCT COMPARATIVE ANALYSIS: GENERATIVE AI-BASED CYBERSECURITY

- 12.5.1.1 Purple AI (SentinelOne)

- 12.5.1.2 Prevent (Darktrace)

- 12.5.1.3 ZDX Copilot (Zscaler)

- 12.5.1.4 FortiAI (Fortinet)

- 12.5.1.5 Precision AI (Palo Alto)

- 12.5.2 PRODUCT COMPARATIVE ANALYSIS: CYBERSECURITY FOR GENERATIVE AI

- 12.5.2.1 QRadar (IBM)

- 12.5.2.2 AI Runtime Security (Palo Alto)

- 12.5.2.3 Nitro Enclaves (AWS)

- 12.5.2.4 Zero Trust Exchange (Zscaler)

- 12.5.2.5 Nemo LLM Guardrails (NVIDIA)

- 12.5.1 PRODUCT COMPARATIVE ANALYSIS: GENERATIVE AI-BASED CYBERSECURITY

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 KEY PLAYERS OFFERING GENERATIVE AI-BASED CYBERSECURITY

- 12.7.2 STARS

- 12.7.3 EMERGING LEADERS

- 12.7.4 PERVASIVE PLAYERS

- 12.7.5 PARTICIPANTS

- 12.7.6 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.6.1 Company Footprint

- 12.7.6.2 Region Footprint

- 12.7.6.3 Offering footprint

- 12.7.6.4 Security type footprint

- 12.7.6.5 End user footprint

- 12.7.7 KEY PLAYERS OFFERING CYBERSECURITY SOLUTIONS FOR GENERATIVE AI

- 12.7.8 STARS

- 12.7.9 EMERGING LEADERS

- 12.7.10 PERVASIVE PLAYERS

- 12.7.11 PARTICIPANTS

- 12.7.12 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.12.1 Company Footprint

- 12.7.12.2 Regional footprint

- 12.7.12.3 Offering footprint

- 12.7.12.4 Security type footprint

- 12.7.12.5 End user footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 STARTUPS/SMES OFFERING GENERATIVE AI-BASED CYBERSECURITY

- 12.8.1.1 Progressive companies

- 12.8.1.2 Responsive companies

- 12.8.1.3 Dynamic companies

- 12.8.1.4 Starting blocks

- 12.8.2 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.2.1 Detailed List of Key Startups/SMEs

- 12.8.2.2 Competitive Benchmarking of Key Startups/SMEs

- 12.8.3 STARTUPS/SMES OFFERING CYBERSECURITY SOLUTIONS FOR GENERATIVE AI

- 12.8.3.1 Progressive companies

- 12.8.3.2 Responsive companies

- 12.8.3.3 Dynamic companies

- 12.8.3.4 Starting blocks

- 12.8.4 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.4.1 Detailed List of Key Startups/SMEs

- 12.8.4.2 Competitive Benchmarking of Key Startups/SMEs

- 12.8.1 STARTUPS/SMES OFFERING GENERATIVE AI-BASED CYBERSECURITY

- 12.9 COMPETITIVE SCENARIO AND TRENDS

- 12.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 GENERATIVE AI-BASED CYBERSECURITY SOLUTION PROVIDERS

- 13.2.1 MICROSOFT

- 13.2.1.1 Business overview

- 13.2.1.2 Products/Solutions/Services offered

- 13.2.1.3 Recent developments

- 13.2.1.3.1 Product launches and enhancements

- 13.2.1.3.2 Deals

- 13.2.1.4 MnM view

- 13.2.1.4.1 Right to win

- 13.2.1.4.2 Strategic choices

- 13.2.1.4.3 Weaknesses and competitive threats

- 13.2.2 IBM

- 13.2.2.1 Business overview

- 13.2.2.2 Products/Solutions/Services offered

- 13.2.2.3 Recent developments

- 13.2.2.3.1 Product launches and enhancements

- 13.2.2.3.2 Deals

- 13.2.2.4 MnM view

- 13.2.2.4.1 Right to win

- 13.2.2.4.2 Strategic choices

- 13.2.2.4.3 Weaknesses and competitive threats

- 13.2.3 GOOGLE

- 13.2.3.1 Business overview

- 13.2.3.2 Products/Solutions/Services offered

- 13.2.3.3 Recent developments

- 13.2.3.3.1 Product launches and enhancements

- 13.2.3.3.2 Deals

- 13.2.3.4 MnM view

- 13.2.3.4.1 Right to win

- 13.2.3.4.2 Strategic choices

- 13.2.3.4.3 Weaknesses and competitive threats

- 13.2.4 SENTINELONE

- 13.2.4.1 Business overview

- 13.2.4.2 Products/Solutions/Services offered

- 13.2.4.3 Recent developments

- 13.2.4.3.1 Product launches and enhancements

- 13.2.4.3.2 Deals

- 13.2.4.4 MnM view

- 13.2.4.4.1 Right to win

- 13.2.4.4.2 Strategic choices

- 13.2.4.4.3 Weaknesses and competitive threats

- 13.2.5 NVIDIA

- 13.2.5.1 Business overview

- 13.2.5.2 Products/Solutions/Services offered

- 13.2.5.3 Recent developments

- 13.2.5.3.1 Product launches and enhancements

- 13.2.5.3.2 Deals

- 13.2.6 NEURALTRUST

- 13.2.6.1 Business overview

- 13.2.6.2 Products/Solutions/Services offered

- 13.2.7 TREND MICRO

- 13.2.8 BLACKBERRY

- 13.2.9 OKTA

- 13.2.10 SANGFOR TECHNOLOGIES

- 13.2.11 VERACODE

- 13.2.12 LEXISNEXIS

- 13.2.13 SECURITYSCORECARD

- 13.2.14 BROADCOM

- 13.2.15 COHESITY

- 13.2.16 ELASTIC NV

- 13.2.17 CYBEREASON

- 13.2.18 FLASHPOINT

- 13.2.19 MOSTLY AI

- 13.2.20 RECORDED FUTURE

- 13.2.21 SECUREFRAME

- 13.2.22 SLASHNEXT

- 13.2.23 VIRUSTOTAL

- 13.2.24 XENONSTACK

- 13.2.25 ZEROFOX

- 13.2.1 MICROSOFT

- 13.3 PROVIDERS OF CYBERSECURITY SOLUTIONS FOR GENERATIVE AI

- 13.3.1 AWS

- 13.3.1.1 Business overview

- 13.3.1.2 Products/Solutions/Services offered

- 13.3.1.3 Recent developments

- 13.3.1.3.1 Deals

- 13.3.1.4 MnM view

- 13.3.1.4.1 Right to win

- 13.3.1.4.2 Strategic choices

- 13.3.1.4.3 Weaknesses and competitive threats

- 13.3.2 CISCO

- 13.3.2.1 Business overview

- 13.3.2.2 Products/Solutions/Services offered

- 13.3.2.3 Recent developments

- 13.3.2.3.1 Product launches and enhancements

- 13.3.2.3.2 Deals

- 13.3.3 CROWDSTRIKE

- 13.3.3.1 Business overview

- 13.3.3.2 Products/Solutions/Services offered

- 13.3.3.3 Recent developments

- 13.3.3.3.1 Product launches and enhancements

- 13.3.3.3.2 Deals

- 13.3.4 FORTINET

- 13.3.4.1 Business overview

- 13.3.4.2 Products/Products/Solutions/Services offered

- 13.3.4.3 Recent developments

- 13.3.4.3.1 Product launches and enhancements

- 13.3.4.3.2 Deals

- 13.3.5 ZSCALER

- 13.3.5.1 Business overview

- 13.3.5.2 Products/Solutions/Services offered

- 13.3.5.3 Recent developments

- 13.3.5.3.1 Product launches and enhancements

- 13.3.5.3.2 Deals

- 13.3.6 PALO ALTO NETWORKS

- 13.3.7 DARKTRACE

- 13.3.8 F5

- 13.3.9 SOPHOS

- 13.3.10 TRELLIX

- 13.3.11 TENABLE

- 13.3.12 SNYK

- 13.3.13 ABNORMAL SECURITY

- 13.3.14 ADVERSA AI

- 13.3.15 AQUA SECURITY

- 13.3.16 BIGID

- 13.3.17 CHECKMARX

- 13.3.18 CREDO AI

- 13.3.19 DEEPKEEP

- 13.3.20 LAKERA

- 13.3.21 SKYFLOW

- 13.3.22 TROJAI

- 13.3.1 AWS

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 GENERATIVE AI MARKET - GLOBAL FORECAST TO 2032

- 14.2.1 MARKET DEFINITION

- 14.2.2 MARKET OVERVIEW

- 14.2.2.1 Generative AI market, by offering

- 14.2.2.2 Generative AI market, by data modality

- 14.2.2.3 Generative AI market, by application

- 14.2.2.4 Generative AI market, by end user

- 14.2.2.5 Generative AI market, by region

- 14.3 ARTIFICIAL INTELLIGENCE IN CYBERSECURITY MARKET - GLOBAL FORECAST TO 2028

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.3.2.1 Artificial intelligence in cybersecurity market, by offering

- 14.3.2.2 Artificial intelligence in cybersecurity market, by security type

- 14.3.2.3 Artificial intelligence in cybersecurity market, by technology

- 14.3.2.4 Artificial intelligence in cybersecurity market, by application

- 14.3.2.5 Artificial intelligence in cybersecurity market, by vertical

- 14.3.2.6 Artificial intelligence in cybersecurity market, by region

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD DOLLAR EXCHANGE RATE, 2020-2024

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 GLOBAL GENERATIVE AI CYBERSECURITY MARKET SIZE AND GROWTH RATE, 2020-2024 (USD MILLION, Y-O-Y %)

- TABLE 4 GLOBAL GENERATIVE AI CYBERSECURITY MARKET SIZE AND GROWTH RATE, 2025-2031 (USD MILLION, Y-O-Y %)

- TABLE 5 GENERATIVE AI CYBERSECURITY MARKET: ECOSYSTEM

- TABLE 6 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 PATENTS FILED, 2019-2025

- TABLE 12 GENERATIVE AI CYBERSECURITY MARKET: KEY PATENTS, 2024-2025

- TABLE 13 AVERAGE SELLING PRICE OF KEY PLAYERS, BY OFFERING, 2025

- TABLE 14 AVERAGE SELLING PRICE, BY SECURITY TYPE, 2025

- TABLE 15 GENERATIVE AI CYBERSECURITY MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 16 PORTERS' FIVE FORCES' IMPACT ON GENERATIVE AI CYBERSECURITY MARKET

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE GENERATIVE AI-BASED CYBERSECURITY VERTICALS

- TABLE 18 KEY BUYING CRITERIA FOR TOP THREE GENERATIVE AI-BASED CYBERSECURITY VERTICALS

- TABLE 19 GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 20 GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 21 GENERATIVE AI CYBERSECURITY MARKET, SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 22 GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 23 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 24 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 25 CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY REGION, 2020-2024 (USD MILLION)

- TABLE 26 CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY REGION, 2025-2031 (USD MILLION)

- TABLE 27 GENERATIVE AI CYBERSECURITY SOFTWARE MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 28 GENERATIVE AI CYBERSECURITY SOFTWARE MARKET, BY DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 29 CLOUD: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 30 CLOUD: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 31 ON-PREMISES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 ON-PREMISES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 33 GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 34 GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 35 GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 36 GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 37 TRAINING & CONSULTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 38 TRAINING & CONSULTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 39 SYSTEM INTEGRATION & IMPLEMENTATION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 SYSTEM INTEGRATION & IMPLEMENTATION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 41 SUPPORT & MAINTENANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 42 SUPPORT & MAINTENANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 43 MANAGED SERVICES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 44 MANAGED SERVICES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 45 CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 46 CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 47 GENERATIVE AI TRAINING DATA SECURITY SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 48 GENERATIVE AI TRAINING DATA SECURITY SOFTWARE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 49 GENERATIVE AI MODEL SECURITY SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 50 GENERATIVE AI MODEL SECURITY SOFTWARE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 51 GENERATIVE AI INFRASTRUCTURE SECURITY SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 GENERATIVE AI INFRASTRUCTURE SECURITY SOFTWARE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 53 GENERATIVE AI APPLICATION SECURITY SOFTWARE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 54 GENERATIVE AI APPLICATION SECURITY SOFTWARE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 55 GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 56 GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 57 END USERS: GENERATIVE AI-BASED CYBERSECURITY MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 58 END USERS: GENERATIVE-BASED AI CYBERSECURITY MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 59 GOVERNMENT & DEFENSE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 60 GOVERNMENT & DEFENSE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 61 BFSI: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 62 BFSI: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 63 IT & ITES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 64 IT & ITES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 65 HEALTHCARE & LIFE SCIENCES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 66 HEALTHCARE & LIFE SCIENCES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 67 RETAIL & ECOMMERCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 RETAIL & ECOMMERCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 69 MANUFACTURING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 70 MANUFACTURING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 71 ENERGY & UTILITIES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 72 ENERGY & UTILITIES: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 73 TELECOMMUNICATIONS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 74 TELECOMMUNICATIONS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 75 AUTOMOTIVE, TRANSPORTATION, AND LOGISTICS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 76 AUTOMOTIVE, TRANSPORTATION, AND LOGISTICS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 77 MEDIA & ENTERTAINMENT: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 78 MEDIA & ENTERTAINMENT: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 79 OTHER END USERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 80 OTHER END USERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 81 END USERS: CYBERSECURITY FOR GENERATIVE AI MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 82 END USERS: CYBERSECURITY FOR GENERATIVE AI MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 83 CLOUD HYPERSCALERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 84 CLOUD HYPERSCALERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 85 MANAGED SECURITY SERVICE PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 86 MANAGED SECURITY SERVICE PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 87 GENERATIVE AI CYBERSECURITY MARKET, BY GENERATIVE AI PROVIDER, 2020-2024 (USD MILLION)

- TABLE 88 GENERATIVE AI CYBERSECURITY MARKET, BY GENERATIVE AI PROVIDER, 2025-2031 (USD MILLION)

- TABLE 89 FOUNDATION MODEL/LLM DEVELOPERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 90 FOUNDATION MODEL/LLM DEVELOPERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 91 DATA ANNOTATORS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 92 DATA ANNOTATORS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 93 CONTENT CREATION PLATFORM PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 94 CONTENT CREATION PLATFORM PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 95 GENERATIVE AI-AS-A-SERVICE PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 96 GENERATIVE AI-AS-A-SERVICE PROVIDERS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 97 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 98 GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 99 THREAT DETECTION & INTELLIGENCE SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 100 THREAT DETECTION & INTELLIGENCE SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 101 RISK ASSESSMENT SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 102 RISK ASSESSMENT SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 103 EXPOSURE MANAGEMENT SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 104 EXPOSURE MANAGEMENT SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 105 PHISHING SIMULATION & PREVENTION SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 106 PHISHING SIMULATION & PREVENTION SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 107 REMEDIATION GUIDANCE SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 108 REMEDIATION GUIDANCE SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 109 THREAT HUNTING PLATFORMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 110 THREAT HUNTING PLATFORMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 111 CODE ANALYSIS SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 112 CODE ANALYSIS SOFTWARE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 113 GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 114 GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 115 GENERATIVE AI CYBERSECURITY MARKET, BY DATABASE SECURITY, 2020-2024 (USD MILLION)

- TABLE 116 GENERATIVE AI CYBERSECURITY MARKET, BY DATABASE SECURITY, 2025-2031 (USD MILLION)

- TABLE 117 DATA LOSS PREVENTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 118 DATA LOSS PREVENTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 119 DATA USAGE MONITORING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 120 DATA USAGE MONITORING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 121 DATA COMPLIANCE & GOVERNANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 122 DATA COMPLIANCE & GOVERNANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 123 DATA ENCRYPTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 124 DATA ENCRYPTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 125 DATA MASKING & TOKENIZATION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 126 DATA MASKING & TOKENIZATION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 127 ACCESS CONTROL: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 128 ACCESS CONTROL: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 129 GENERATIVE AI CYBERSECURITY MARKET, BY NETWORK SECURITY, 2020-2024 (USD MILLION)

- TABLE 130 GENERATIVE AI CYBERSECURITY MARKET, BY NETWORK SECURITY, 2025-2031 (USD MILLION)

- TABLE 131 NETWORK TRAFFIC ANALYSIS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 132 NETWORK TRAFFIC ANALYSIS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 133 SECURE ACCESS SERVICE EDGE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 134 SECURE ACCESS SERVICE EDGE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 135 ZERO TRUST NETWORK ACCESS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 136 ZERO TRUST NETWORK ACCESS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 137 FIREWALLS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 138 FIREWALLS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 139 INTRUSION DETECTION/PREVENTION SYSTEMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 140 INTRUSION DETECTION/PREVENTION SYSTEMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 141 VPNS & SECURE TUNNELING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 142 VPNS & SECURE TUNNELING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 143 GENERATIVE AI CYBERSECURITY MARKET, BY ENDPOINT SECURITY, 2020-2024 (USD MILLION)

- TABLE 144 GENERATIVE AI CYBERSECURITY MARKET, BY ENDPOINT SECURITY, 2025-2031 (USD MILLION)

- TABLE 145 ENDPOINT DETECTION & RESPONSE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 146 ENDPOINT DETECTION & RESPONSE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 147 ENDPOINT PROTECTION PLATFORMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 148 ENDPOINT PROTECTION PLATFORMS: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 149 GENERATIVE AI CYBERSECURITY MARKET, BY APPLICATION SECURITY, 2020-2024 (USD MILLION)

- TABLE 150 GENERATIVE AI CYBERSECURITY MARKET, BY APPLICATION SECURITY, 2025-2031 (USD MILLION)

- TABLE 151 STATIC APPLICATION SECURITY TESTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 152 STATIC APPLICATION SECURITY TESTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 153 DYNAMIC APPLICATION SECURITY TESTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 154 DYNAMIC APPLICATION SECURITY TESTING: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 155 LLM SECURITY: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 156 LLM SECURITY: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 157 RUNTIME PROTECTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 158 RUNTIME PROTECTION: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 159 INCIDENT RESPONSE & RECOVERY: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 160 INCIDENT RESPONSE & RECOVERY: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 161 GOVERNANCE, RISK, AND COMPLIANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 162 GOVERNANCE, RISK, AND COMPLIANCE: GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 163 GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 164 GENERATIVE AI CYBERSECURITY MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 165 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 166 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 167 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 168 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 169 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 170 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 171 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 172 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 173 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 174 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 175 NORTH AMERICA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 176 NORTH AMERICA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 177 NORTH AMERICA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 178 NORTH AMERICA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 179 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 180 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 181 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 182 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 183 NORTH AMERICA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 184 NORTH AMERICA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 185 NORTH AMERICA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 186 NORTH AMERICA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 187 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 188 NORTH AMERICA: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 189 US: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 190 US: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 191 US: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 192 US: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 193 US: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 194 US: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 195 US: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 196 US: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 197 US: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 198 US: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 199 US: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 200 US: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 201 US: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 202 US: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 203 US: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 204 US: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 205 US: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 206 US: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 207 US: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 208 US: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 209 US: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 210 US: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 211 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 212 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 213 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 214 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 215 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 216 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 217 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 218 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 219 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 220 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 221 CANADA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 222 CANADA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 223 CANADA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 224 CANADA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 225 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 226 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 227 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 228 CANADA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 229 CANADA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 230 CANADA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 231 CANADA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 232 CANADA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 233 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 234 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 235 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 236 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 237 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 238 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 239 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 240 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 241 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 242 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 243 EUROPE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 244 EUROPE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE 2025-2031 (USD MILLION)

- TABLE 245 EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 246 EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 247 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 248 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 249 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 250 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 251 EUROPE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 252 EUROPE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 253 EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 254 EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 255 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 256 EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 257 UK: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 258 UK: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 259 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 260 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 261 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 262 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 263 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 264 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 265 UK: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 266 UK: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 267 UK: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 268 UK: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 269 UK: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 270 UK: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 271 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 272 UK: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 273 UK: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 274 UK: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 275 UK: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 276 UK: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 277 UK: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 278 UK: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 279 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 280 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 281 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 282 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 283 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 284 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 285 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 286 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 287 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 288 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 289 GERMANY: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 290 GERMANY: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 291 GERMANY: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 292 GERMANY: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 293 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 294 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 295 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 296 GERMANY: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 297 GERMANY: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 298 GERMANY: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 299 GERMANY: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 300 GERMANY: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 301 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 302 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 303 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 304 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 305 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 306 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 307 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 308 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 309 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 310 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 311 FRANCE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 312 FRANCE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 313 FRANCE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 314 FRANCE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 315 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 316 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 317 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 318 FRANCE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 319 FRANCE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 320 FRANCE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 321 FRANCE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 322 FRANCE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 323 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 324 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 325 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 326 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 327 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 328 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 329 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 330 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 331 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 332 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 333 REST OF EUROPE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 334 REST OF EUROPE: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 335 REST OF EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 336 REST OF EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 337 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 338 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 339 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 340 REST OF EUROPE: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 341 REST OF EUROPE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 342 REST OF EUROPE: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 343 REST OF EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 344 REST OF EUROPE: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 345 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 346 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 347 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 348 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 349 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 350 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 351 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 352 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 353 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 354 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 355 ASIA PACIFIC: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 356 ASIA PACIFIC: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 357 ASIA PACIFIC: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 358 ASIA PACIFIC: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 359 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 360 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 361 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 362 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 363 ASIA PACIFIC: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 364 ASIA PACIFIC: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 365 ASIA PACIFIC: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 366 ASIA PACIFIC: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 367 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 368 ASIA PACIFIC: GENERATIVE AI CYBERSECURITY MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 369 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 370 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)

- TABLE 371 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2020-2024 (USD MILLION)

- TABLE 372 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE TYPE, 2025-2031 (USD MILLION)

- TABLE 373 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 374 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SOFTWARE DEPLOYMENT MODE, 2025-2031 (USD MILLION)

- TABLE 375 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 376 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SERVICE, 2025-2031 (USD MILLION)

- TABLE 377 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 378 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY PROFESSIONAL SERVICE, 2025-2031 (USD MILLION)

- TABLE 379 CHINA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 380 CHINA: GENERATIVE AI-BASED CYBERSECURITY SOFTWARE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 381 CHINA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 382 CHINA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 383 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2020-2024 (USD MILLION)

- TABLE 384 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY SECURITY TYPE, 2025-2031 (USD MILLION)

- TABLE 385 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 386 CHINA: GENERATIVE AI CYBERSECURITY MARKET, BY END USER, 2025-2031 (USD MILLION)

- TABLE 387 CHINA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 388 CHINA: GENERATIVE AI-BASED CYBERSECURITY END USERS, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 389 CHINA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2020-2024 (USD MILLION)

- TABLE 390 CHINA: CYBERSECURITY SOFTWARE MARKET FOR GENERATIVE AI, BY END USER, 2025-2031 (USD MILLION)

- TABLE 391 INDIA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 392 INDIA: GENERATIVE AI CYBERSECURITY MARKET, BY OFFERING, 2025-2031 (USD MILLION)