PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1811735

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1811735

Medical Polymer Market by Type (Medical Plastics, Medical Elastomers), Application (Medical Disposables, Medical Instruments and Devices, Prosthetics, Diagnostics Instruments and Tools), Manufacturing Technology, and Region - Global Forecast to 2030

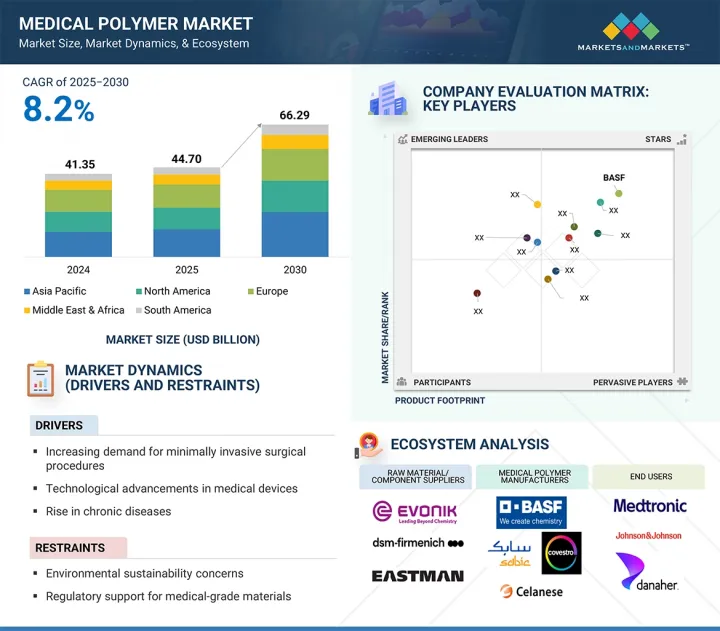

The medical polymer market is projected to reach USD 66.29 billion by 2030 from USD 44.70 billion in 2025, at a CAGR of 8.2% during the forecast period. The medical polymer market is experiencing rapid growth as a result of continual progress in healthcare, materials engineering, and patient-focused innovation. Major factors driving include need for materials that are lightweight, durable, and suitable for use in situations involving biocompatible materials, like implants or catheters, diagnostic equipment, and even surgical instruments.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kiloton) |

| Segments | Type, Application, Manufacturing Technology, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Middle East & Africa |

The increased prevalence of chronic diseases, aging population, and the need for minimally invasive procedures is creating preference for advanced polymers that provide flexibility, security, and accuracy. The considerable shift in the use of disposable medical products, where possible, for sanitation and fewer contaminants has contributed to the proliferation of components made from polymers. The science of polymers is advancing to create polymers and materials with superior mechanical strength, durability, antimicrobial properties, and compatibility with active-sterilization techniques. Advances in knowledge and developments have resulted in breakthroughs in polymers that can hold shapes, or bioresorbable, that offer opportunities in the areas of drug delivery devices and tissue engineering. Proliferation of medical-grade 3D printing has revolutionized this area because custom-designed implants and devices can now be developed rapidly. There has increased attention on sustainable practices, leading to interest in recyclable and biodegradable polymers.

"Medical elastomers to account for the second-largest type in the medical polymer market during the forecast period."

Medical elastomers account for the second-largest type in the medical polymer market based on unique combinations of characteristics, such as flexibility, durability, and biocompatibility, allowing them to be used for hundreds of precise applications for critical healthcare. Many of the devoted elastomer applications are products used to contain fluids or products that need to be manipulated with constant movement, stretching, or compression, like seals, gaskets, tubing, syringes, plungers, and catheter components. Medical elastomer products are best known because of their chemical resistance, resistance to temperature swings, and resistance to sterilization techniques, which enables reliable products in high-stress medical applications. Because silicone elastomers, thermoplastic elastomers (TPE), and rubber materials are often specifically mentioned in literature due to increased comfort above conventional or hard polymers, they are favored for wearable medical devices and skin-contact applications. In addition, the influence of minimization continues to drive performance elastomeric materials, as do the advanced design aspects influencing drug delivery systems, automated enclosed testing systems, and lifestyle diagnostic devices. Furthermore, elastomeric materials are especially amenable to automated manufacturing and/or molding with E-modulus and tensile strength decreases, enabling cost-effective production in considerably large amounts. Combined with supporting and allowing innovation and safety in modern healthcare, these ultimately contribute to the fast-growing and extremely important category of medical elastomers in the medical polymer market.

"Medical disposables to account for the second-largest share of the medical polymer market during the forecast period."

Medical disposables are the second-largest application in the medical polymer market because of their importance in cleanliness, patient safety, and infection control in healthcare settings. Items such as syringes, gloves, IV bags, tubing and connections, surgical drapes, and masks are designed for single-use to prevent cross-contamination and maintain sterile environments. The emphasis on infection prevention and regulations supporting infection control have increased demand for disposable medical items. Due to their excellent processability, low cost, and compatibility with sterilizing processes, the polymers used in medical disposables are primarily polypropylene, polyethylene, and PVC. The increase in hospital stays, enhanced surgical procedures, and outpatient care, especially in emerging regions, are driving demand for good quality disposables. Convenience of ready-to-use pre-sterilized items can add efficiency in busy medical settings. As healthcare continues to focus on safety, cost-effective practices, and efficiencies, polymer medical disposables will be an important future growth area going forward.

"Injection molding is projected to be the second-largest manufacturing technology in the medical polymer market during the forecast period."

Injection molding is the second-largest manufacturing technology in the medical polymer space because it can produce highly precise and complex components at scale with good reliability and efficiency. Injection molding is used to produce a wide variety of medical products, for example, housing for diagnostic equipment, surgical instrument handles, syringes, connectors, components of implantable devices, and so forth. Injection molding is compatible with many medical-grade polymers, for example, it can be made from polycarbonate, polypropylene, and ABS. With injection molding, the manufacture of components that must have strength, biocompatibility, chemical resistance, and washability is possible. Injection molding can be made to tight tolerances with complex geometries; all of which are relevant in meeting the safety and performance requirements of the medical device industry. Injection molding is also compatible with automation and is conducive to produce items in large volumes while being cost-effective along with high quality output. Recent advancements in multi-shot and micro fabrication further enhances the application range as well. With all of these advantages it is easy to see how injection molding plays a critical role in the medical polymer market which supports product innovations and continues to aid the demand for sophisticated and reliable medical products.

"North America is projected to be the second-fastest growing region in the medical polymer market during the forecast period."

North America is the second-fastest growing region in the medical polymer market, due largely to strong healthcare dynamics, and innovated demand. Per capita healthcare expenses are rising, initiated by expanding insurance coverage in the US and strong public and private healthcare investments in Canada. The medical devices, packaging, and wound care categories are projected to account for greater growth in North America than any other region as healthcare advances. However, the US has one of the most innovative healthcare environments in the world based on a developed healthcare infrastructure, a strong Research and Development (R&D) ecosystem, and a strong partnership with the polymer industry, leading to the creation of a broad and expanding array of high-performance polymers. Many of these polymers have properties that are biocompatible and even biodegradable (resins and fibers) for surgical devices, diagnostics, and drug delivery systems. The healthcare industry relies on new product designs and innovative ideas regarding the use of new products developments (e.g., PEEK and other engineering plastics), to ensure successful product introduction that will also meet patients' preferences for disposable, minimally invasive, and home care solutions. While the Asia Pacific region is leading with the highest CAGR, North America is the second-fastest growing region, due to its regulatory strength (and US regulation innovation), established healthcare system, and leading region with polymer manufacturers serving patients and the medical sector without sacrificing innovation in the development of polymer technologies.

Extensive interviews with experts were conducted to determine and verify the market size for several segments and subsegments and the information gathered through secondary research.

The break-up of interviews with experts is given below:

- By Department: Tier 1: 40%, Tier 2: 25%, and Tier 3: 35%

- By Designation: C Level: 35%, Director Level: 30%, and Executives: 35%

- By Region: North America: 25%, Europe: 45%, Asia Pacific: 20%, South America: 5%, Middle East & Africa 5%

BASF SE (Germany), SABIC (Saudi Arabia), Covestro AG (Germany), Celanese corporation (US), Evonik Industries (Germany), Arkema (France), Solvay (Belgium), Kuraray Co., Ltd. (Japan), Momentive Performance Materials Inc. (US), and DuPont (US), among others are some of the key players in the medical polymer market.

The study includes an in-depth competitive analysis of these key players in the medical polymer market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The market study covers the medical polymer market across various segments. It aims to estimate the market size and the growth potential of this market across different segments based on type, application, manufacturing technology, and region. The study also includes an in-depth competitive analysis of key players in the market, their company profiles, key observations related to their products and business offerings, recent developments undertaken by them, and key growth strategies adopted by them to enhance their positions in the medical polymer market.

Key Benefits of Buying the Report

The report is expected to help the market leaders/new entrants in this market share the closest approximations of the revenue numbers of the overall medical polymer market and its segments and subsegments. This report is projected to help stakeholders understand the competitive landscape of the market, gain insights to improve the positions of their businesses, and plan suitable go-to-market strategies. The report also aims to help stakeholders understand the pulse of the market and provides them with information on the key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing demand for biocompatible materials, Growing aging population globally, Advancements in medical technology, Regulatory support for medical-grade materials), restraints (Regulatory complexities and approvals, High competition from alternative materials, Environmental sustainability concerns), opportunities (Growth in regenerative medicine, Demand for minimally invasive devices, Advancements in biodegradable polymers), challenges (Cost constraints for novel materials, Long term durability and degradation control)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the medical polymer market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the medical polymer market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the medical polymer market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like BASF SE (Germany), SABIC (Saudi Arabia), Covestro AG (Germany), Celanese corporation (US), Evonik Industries (Germany), Arkema (France), Solvay (Belgium), Kuraray Co., Ltd. (Japan), Momentive Performance Materials Inc. (US), and DuPont (US), among others are covered in the medical polymer market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of primary interview participants-demand and supply side

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 FACTOR ANALYSIS

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 LIMITATIONS AND RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MEDICAL POLYMER MARKET

- 4.2 MEDICAL POLYMER MARKET, BY TYPE

- 4.3 MEDICAL POLYMER MARKET, BY APPLICATION

- 4.4 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY

- 4.5 MEDICAL POLYMER MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand for biocompatible materials

- 5.2.1.2 Surge in global aging population

- 5.2.1.3 Advancements in medical technology

- 5.2.1.4 Rise in chronic diseases

- 5.2.1.5 Regulatory support for medical-grade materials

- 5.2.2 RESTRAINTS

- 5.2.2.1 Regulatory complexities and approvals

- 5.2.2.2 High competition from alternative materials

- 5.2.2.3 Environmental sustainability concerns

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growth in regenerative medicine

- 5.2.3.2 Demand for minimally invasive devices

- 5.2.3.3 Advancements in biodegradable polymers

- 5.2.4 CHALLENGES

- 5.2.4.1 Cost constraints for novel materials

- 5.2.4.2 Long-term durability and degradation control

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT FROM NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF BUYERS

- 5.3.4 BARGAINING POWER OF SUPPLIERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 MACROECONOMIC INDICATORS

- 5.4.1 GLOBAL GDP TRENDS

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 VALUE CHAIN ANALYSIS

- 6.3.1 RAW MATERIAL SUPPLIERS

- 6.3.2 MANUFACTURERS

- 6.3.3 DISTRIBUTORS

- 6.3.4 END CONSUMERS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 CASE STUDY ANALYSIS

- 6.5.1 EVONIK INDUSTRIES PROVIDES MEDICAL POLYMERS TO JENACELL GMBH FOR WOUND DRESSINGS, IMPLANTABLE MATERIALS, AND DRUG DELIVERY SYSTEMS

- 6.5.2 ENSINGER OFFERS HIGH-PERFORMANCE, MEDICAL-GRADE POLYMERS FOR HIGH-FREQUENCY SURGERY

- 6.6 REGULATORY LANDSCAPE

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 KEY TECHNOLOGY

- 6.7.1.1 Biocompatible polymers

- 6.7.1.2 Thermoplastic elastomers

- 6.7.2 COMPLEMENTARY TECHNOLOGY

- 6.7.2.1 Thermoplastic elastomers

- 6.7.2.2 Surface modification techniques

- 6.7.1 KEY TECHNOLOGY

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.9 TRADE ANALYSIS

- 6.9.1 IMPORT SCENARIO

- 6.9.2 EXPORT SCENARIO

- 6.10 KEY CONFERENCES & EVENTS, 2025-2026

- 6.11 PRICING ANALYSIS

- 6.11.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 6.11.2 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2022-2024

- 6.11.3 AVERAGE SELLING PRICE OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

- 6.12 INVESTMENT AND FUNDING SCENARIO

- 6.13 PATENT ANALYSIS

- 6.13.1 METHODOLOGY

- 6.13.2 PATENTS GRANTED WORLDWIDE, 2015-2024

- 6.13.3 PUBLICATION TRENDS

- 6.13.4 INSIGHTS

- 6.13.5 LEGAL STATUS OF PATENTS

- 6.13.6 JURISDICTION ANALYSIS

- 6.13.7 TOP APPLICANTS

- 6.14 IMPACT OF AI/GEN AI ON MEDICAL POLYMER MARKET

- 6.15 IMPACT OF 2025 US TARIFF ON MEDICAL POLYMER MARKET

- 6.15.1 INTRODUCTION

- 6.15.2 KEY TARIFF RATES

- 6.15.3 PRICE IMPACT ANALYSIS

- 6.15.4 IMPACT ON KEY COUNTRIES/REGIONS

- 6.15.4.1 North America

- 6.15.4.2 Europe

- 6.15.4.3 Asia Pacific

- 6.15.5 IMPACT ON END-USE INDUSTRIES

7 MEDICAL POLYMER MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 MEDICAL PLASTICS

- 7.2.1 ADVANCEMENTS IN MATERIAL SCIENCE AND MANUFACTURING TECHNOLOGIES TO DRIVE MARKET

- 7.2.2 POLYPROPYLENE

- 7.2.3 POLYVINYL CHLORIDE

- 7.2.4 POLYETHYLENE

- 7.2.5 POLYSTYRENE

- 7.2.6 ENGINEERING & HIGH-PERFORMANCE PLASTICS

- 7.2.6.1 Polyether ether ketone

- 7.2.6.2 Nylon/polyamide

- 7.2.6.3 Polyphenylsulfone

- 7.2.6.4 Polysulfones

- 7.2.6.5 Polymethyl methacrylate

- 7.2.6.6 Polycarbonate

- 7.2.6.7 Acrylonitrile butadiene styrene

- 7.2.6.8 Other Engineering & high-performance plastics

- 7.2.7 OTHER MEDICAL PLASTICS

- 7.3 MEDICAL ELASTOMERS

- 7.3.1 FLEXIBILITY, DURABILITY, AND BIOCOMPATIBILITY TO DRIVE MARKET

- 7.3.2 SILICONE

- 7.3.3 THERMOPLASTIC ELASTOMERS

- 7.3.3.1 Thermoplastic polyurethane

- 7.3.3.2 Thermoplastic vulcanizates

- 7.3.3.3 Thermoplastic styrenic elastomers

- 7.3.3.3.1 Poly(styrene-butadiene-styrene)

- 7.3.3.3.2 Styrene-ethylene-butylene-styrene

- 7.3.3.4 Thermoplastic copolyester elastomers

- 7.4 OTHER MEDICAL ELASTOMERS

8 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 EXTRUSION TUBING

- 8.2.1 INCREASING USE IN INTRAVENOUS DELIVERY SYSTEMS, CATHETERS, AND SURGICAL INSTRUMENTS TO DRIVE MARKET

- 8.3 COMPRESSION MOLDING

- 8.3.1 INCREASING USE IN PROSTHETICS, ORTHOPEDIC IMPLANTS, AND DENTAL COMPONENTS TO DRIVE MARKET

- 8.4 INJECTION MOLDING

- 8.4.1 INCREASING USE OF SYRINGES, SURGICAL INSTRUMENTS, AND IMPLANTABLE DEVICES TO DRIVE MARKET

- 8.5 OTHER MANUFACTURING TECHNOLOGIES

9 MEDICAL POLYMER MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 MEDICAL DISPOSABLES

- 9.2.1 INCREASING DEMAND FOR CATHETERS AND SYRINGES TO DRIVE MARKET

- 9.2.2 GLOVES

- 9.2.3 SYRINGES

- 9.2.4 MEDICAL BAGS

- 9.2.5 OTHER MEDICAL DISPOSABLES

- 9.3 MEDICAL INSTRUMENTS & DEVICES

- 9.3.1 INCREASING SURGICAL AND PROCEDURAL APPLICATIONS TO DRIVE MARKET

- 9.3.2 MEDICAL TUBES

- 9.3.3 CATHETERS

- 9.3.4 DRUG DELIVERY INSTRUMENTS

- 9.3.5 OTHER MEDICAL INSTRUMENTS & DEVICES

- 9.4 PROSTHETICS

- 9.4.1 RISING DEMAND FOR ADVANCED LIMB PROSTHESES AND IMPLANTS TO DRIVE MARKET

- 9.4.2 IMPLANTS

- 9.4.3 LIMB PROSTHESIS

- 9.4.4 OTHER PROSTHETICS APPLICATIONS

- 9.5 DIAGNOSTIC INSTRUMENTS & TOOLS

- 9.5.1 INCREASING DEMAND IN SURGICAL AND PROCEDURAL APPLICATIONS TO DRIVE MARKET

- 9.5.2 DENTAL TOOLS

- 9.5.3 SURGICAL INSTRUMENTS

- 9.5.4 OTHER DIAGNOSTIC INSTRUMENTS & TOOLS

- 9.6 OTHER APPLICATIONS

10 MEDICAL POLYMER MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 High R&D investments in medical sector to drive market

- 10.2.2 CANADA

- 10.2.2.1 Emerging demand for dental implants to drive market

- 10.2.3 MEXICO

- 10.2.3.1 Expansion of manufacturing facilities to drive market

- 10.2.1 US

- 10.3 ASIA PACIFIC

- 10.3.1 CHINA

- 10.3.1.1 Establishment of medical device manufacturing units and investment in other healthcare-related sectors to drive market

- 10.3.2 INDIA

- 10.3.2.1 Rapid economic growth and growing population to drive market

- 10.3.3 SOUTH KOREA

- 10.3.3.1 Advanced healthcare and medical technologies to boost market

- 10.3.4 JAPAN

- 10.3.4.1 Developments in minimally invasive treatment and robotic surgery to support market growth

- 10.3.5 AUSTRALIA

- 10.3.5.1 Regulatory compliance and strategic collaborations to support market growth

- 10.3.6 REST OF ASIA PACIFIC

- 10.3.1 CHINA

- 10.4 MIDDLE EAST & AFRICA

- 10.4.1 GCC COUNTRIES

- 10.4.1.1 Saudi Arabia

- 10.4.1.1.1 Surge in aging population to drive demand for medical polymers

- 10.4.1.2 UAE

- 10.4.1.2.1 Population growth and changing epidemiology to drive market

- 10.4.1.3 Rest of GCC

- 10.4.1.1 Saudi Arabia

- 10.4.2 SOUTH AFRICA

- 10.4.2.1 Increased government spending on healthcare to drive market

- 10.4.3 REST OF MIDDLE EAST & AFRICA

- 10.4.1 GCC COUNTRIES

- 10.5 EUROPE

- 10.5.1 GERMANY

- 10.5.1.1 Rising demand in dental implant application to drive market

- 10.5.2 FRANCE

- 10.5.2.1 Aging population and sedentary lifestyle to boost demand for polymers

- 10.5.3 UK

- 10.5.3.1 Growing incidences of chronic diseases and government support for innovation to drive market

- 10.5.4 ITALY

- 10.5.4.1 Strong production facilities with presence of global players to propel market growth

- 10.5.5 SPAIN

- 10.5.5.1 Surge in government funding for healthcare sector to support market

- 10.5.6 REST OF EUROPE

- 10.5.1 GERMANY

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Growing aging population, expanding economy, and increasing health awareness to drive market

- 10.6.2 ARGENTINA

- 10.6.2.1 Availability of highly trained specialists and low cost of medical services boosting medical tourism industry

- 10.6.3 REST OF SOUTH AMERICA

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES

- 11.3 REVENUE ANALYSIS, 2022-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Type footprint

- 11.7.5.4 Application footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 MAJOR PLAYERS

- 12.1.1 BASF

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Services/Solutions offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 SABIC

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Services/Solutions offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 COVESTRO AG

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Services/Solutions offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Expansions

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 CELANESE CORPORATION

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Services/Solutions offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.3.2 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 EVONIK INDUSTRIES

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Services/Solutions offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Expansions

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 ARKEMA

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Services/Solutions offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Expansions

- 12.1.6.4 MnM view

- 12.1.6.4.1 Key strengths

- 12.1.7 SOLVAY

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Services/Solutions offered

- 12.1.7.3 MnM view

- 12.1.7.3.1 Key strengths

- 12.1.8 KURARAY CO., LTD.

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Services/Solutions offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Expansions

- 12.1.8.4 MnM view

- 12.1.9 MOMENTIVE PERFORMANCE MATERIALS INC.

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Services/Solutions offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.9.3.2 Expansions

- 12.1.9.4 MnM view

- 12.1.10 DUPONT

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Services/Solutions offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.10.3.2 Expansions

- 12.1.10.4 MnM view

- 12.1.1 BASF

- 12.2 OTHER PLAYERS

- 12.2.1 TRINSEO

- 12.2.2 KRATON CORPORATION

- 12.2.3 TOTAL PLASTICS

- 12.2.4 SIMONA AMERICA

- 12.2.5 DSM

- 12.2.6 INVIBIO

- 12.2.7 AVIENT CORPORATION

- 12.2.8 RTP COMPANY

- 12.2.9 TEKNIPLEX

- 12.2.10 TEKNOR APEX

- 12.2.11 MITSUBISHI CHEMICALS ADVANCED MATERIALS

- 12.2.12 WACKER CHIMIE

- 12.2.13 HARDIE POLYMERS

- 12.2.14 ELIX POLYMERS

- 12.2.15 INNOVATIVE POLYMER COMPOUNDS

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 MEDICAL POLYMER MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 MEDICAL POLYMER MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2018-2025

- TABLE 4 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP FOUR APPLICATIONS

- TABLE 5 KEY BUYING CRITERIA IN MAJOR APPLICATIONS

- TABLE 6 MEDICAL POLYMER MARKET: ROLE IN ECOSYSTEM

- TABLE 7 GLOBAL: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 MEDICAL POLYMER MARKET: CONFERENCES & EVENTS, 2025-2026

- TABLE 12 AVERAGE SELLING PRICE OF MEDICAL POLYMER, BY REGION, 2022-2024 (USD/KG)

- TABLE 13 AVERAGE SELLING PRICE OF MEDICAL POLYMER OFFERED BY KEY PLAYERS, BY APPLICATION, 2024 (USD/KG)

- TABLE 14 TOP 10 PATENT OWNERS, 2015-2024

- TABLE 15 TABLE 1: US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 16 MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 17 MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 18 MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 19 MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 20 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 21 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 22 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 23 MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 24 MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 25 MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 26 MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 27 MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 28 MEDICAL POLYMER MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 29 MEDICAL POLYMER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 30 MEDICAL POLYMER MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 31 MEDICAL POLYMER MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 32 NORTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 33 NORTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 34 NORTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 35 NORTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 36 NORTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 37 NORTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 38 NORTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 39 NORTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 40 NORTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 41 NORTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 42 NORTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 43 NORTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 44 NORTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 45 NORTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 46 NORTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 47 NORTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 48 US: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 49 US: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 50 US: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 51 US: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 52 US: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 53 US: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 54 US: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 55 US: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 56 CANADA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 57 CANADA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 58 CANADA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 59 CANADA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 60 CANADA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 61 CANADA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 62 CANADA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 63 CANADA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 64 MEXICO: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 65 MEXICO: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 66 MEXICO: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 67 MEXICO: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 68 MEXICO: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 69 MEXICO: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 70 MEXICO: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 71 MEXICO: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 72 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 73 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 74 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 75 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 76 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 77 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 78 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 79 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 80 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 81 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 82 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 83 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 84 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 85 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 86 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 87 ASIA PACIFIC: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 88 CHINA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 89 CHINA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 90 CHINA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 91 CHINA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 92 CHINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 93 CHINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 94 CHINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 95 CHINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 96 INDIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 97 INDIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 98 INDIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 99 INDIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 100 INDIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 101 INDIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 102 INDIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 103 INDIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 104 SOUTH KOREA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 105 SOUTH KOREA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 106 SOUTH KOREA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 107 SOUTH KOREA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 108 SOUTH KOREA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 109 SOUTH KOREA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 110 SOUTH KOREA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 111 SOUTH KOREA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 112 JAPAN: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 113 JAPAN: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 114 JAPAN: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 115 JAPAN: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 116 JAPAN: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 117 JAPAN: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 118 JAPAN: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 119 JAPAN: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 120 AUSTRALIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 121 AUSTRALIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 122 AUSTRALIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 123 AUSTRALIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 124 AUSTRALIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 125 AUSTRALIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 126 AUSTRALIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 127 AUSTRALIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 128 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 129 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 130 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 131 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 132 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 133 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 134 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 135 REST OF ASIA PACIFIC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 136 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 137 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 138 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 139 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 140 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 141 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 142 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 143 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 144 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 146 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 147 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 148 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 150 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 151 MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 152 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 153 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 154 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 155 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 156 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 157 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 158 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 159 SAUDI ARABIA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 160 UAE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 161 UAE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 162 UAE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 163 UAE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 164 UAE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 165 UAE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 166 UAE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 167 UAE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 168 REST OF GCC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 169 REST OF GCC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 170 REST OF GCC: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 171 REST OF GCC: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 172 REST OF GCC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 173 REST OF GCC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 174 REST OF GCC: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 175 REST OF GCC: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 176 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 177 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 178 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 179 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 180 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 181 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 182 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 183 SOUTH AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 184 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 185 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 186 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 187 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 188 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 189 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 190 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 191 REST OF MIDDLE EAST & AFRICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 192 EUROPE: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 193 EUROPE: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 194 EUROPE: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 195 EUROPE: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 196 EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 197 EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 198 EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 199 EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 200 EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 201 EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 202 EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 203 EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 204 EUROPE: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 205 EUROPE: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 206 EUROPE: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 207 EUROPE: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 208 GERMANY: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 209 GERMANY: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 210 GERMANY: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 211 GERMANY: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 212 GERMANY: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 213 GERMANY: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 214 GERMANY: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 215 GERMANY: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 216 FRANCE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 217 FRANCE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 218 FRANCE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 219 FRANCE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 220 FRANCE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 221 FRANCE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 222 FRANCE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 223 FRANCE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 224 UK: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 225 UK: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 226 UK: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 227 UK: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 228 UK: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 229 UK: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 230 UK: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 231 UK: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 232 ITALY: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 233 ITALY: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 234 ITALY: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 235 ITALY: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 236 ITALY: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 237 ITALY: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 238 ITALY: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 239 ITALY: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 240 SPAIN: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 241 SPAIN: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 242 SPAIN: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 243 SPAIN: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 244 SPAIN: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 245 SPAIN: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 246 SPAIN: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 247 SPAIN: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 248 REST OF EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 249 REST OF EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 250 REST OF EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 251 REST OF EUROPE: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 252 REST OF EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 253 REST OF EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 254 REST OF EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 255 REST OF EUROPE: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 256 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 257 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 258 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 259 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 260 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 261 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 262 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 263 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 264 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 265 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 266 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 267 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 268 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (USD MILLION)

- TABLE 269 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 270 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2022-2024 (KILOTON)

- TABLE 271 SOUTH AMERICA: MEDICAL POLYMER MARKET, BY MANUFACTURING TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 272 BRAZIL: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 273 BRAZIL: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 274 BRAZIL: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 275 BRAZIL: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 276 BRAZIL: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 277 BRAZIL: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 278 BRAZIL: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 279 BRAZIL: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 280 ARGENTINA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 281 ARGENTINA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 282 ARGENTINA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 283 ARGENTINA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 284 ARGENTINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 285 ARGENTINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 286 ARGENTINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 287 ARGENTINA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 288 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (USD MILLION)

- TABLE 289 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 290 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2022-2024 (KILOTON)

- TABLE 291 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY TYPE, 2025-2030 (KILOTON)

- TABLE 292 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 293 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 294 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 295 REST OF SOUTH AMERICA: MEDICAL POLYMER MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 296 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MEDICAL POLYMER MARKET BETWEEN 2021 AND 2025

- TABLE 297 MEDICAL POLYMER MARKET: DEGREE OF COMPETITION

- TABLE 298 MEDICAL POLYMER MARKET: REGION FOOTPRINT

- TABLE 299 MEDICAL POLYMER MARKET: TYPE FOOTPRINT

- TABLE 300 MEDICAL POLYMER MARKET: APPLICATION FOOTPRINT

- TABLE 301 MEDICAL POLYMER MARKET: KEY STARTUPS/SMES

- TABLE 302 MEDICAL POLYMER MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 303 MEDICAL POLYMER MARKET: PRODUCT LAUNCHES, JANUARY 2021-JULY 2025

- TABLE 304 MEDICAL POLYMER MARKET: DEALS, JANUARY 2021-JULY 2025

- TABLE 305 MEDICAL POLYMER MARKET: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 306 BASF: COMPANY OVERVIEW

- TABLE 307 BASF: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 308 BASF: PRODUCT LAUNCHES, JANUARY 2021-JULY 2025

- TABLE 309 BASF: DEALS, JANUARY 2021-JULY 2025

- TABLE 310 SABIC: COMPANY OVERVIEW

- TABLE 311 SABIC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 312 SABIC: DEALS, JANUARY 2021-JULY 2025

- TABLE 313 COVESTRO AG: COMPANY OVERVIEW

- TABLE 314 COVESTRO AG: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 315 COVESTRO AG: PRODUCT LAUNCHES, JANUARY 2021-JULY 2025

- TABLE 316 COVESTRO AG: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 317 CELANESE CORPORATION: COMPANY OVERVIEW

- TABLE 318 CELANESE CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 319 CELANESE CORPORATION: DEALS, JANUARY 2021-JULY 2025

- TABLE 320 CELANESE CORPORATION: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 321 EVONIK INDUSTRIES: COMPANY OVERVIEW

- TABLE 322 EVONIK INDUSTRIES: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 323 EVONIK INDUSTRIES: PRODUCT LAUNCHES, JANUARY 2021-JULY 2025

- TABLE 324 EVONIK INDUSTRIES: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 325 ARKEMA: COMPANY OVERVIEW

- TABLE 326 ARKEMA: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 327 ARKEMA: PRODUCT LAUNCHES, JANUARY 2021-JULY 2025

- TABLE 328 ARKEMA: DEALS, JANUARY 2021-JULY 2025

- TABLE 329 ARKEMA: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 330 SOLVAY: COMPANY OVERVIEW

- TABLE 331 SOLVAY: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 332 KURARAY CO., LTD.: COMPANY OVERVIEW

- TABLE 333 KURARAY CO., LTD.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 334 KURARAY CO., LTD.: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 335 MOMENTIVE PERFORMANCE MATERIALS INC.: COMPANY OVERVIEW

- TABLE 336 MOMENTIVE PERFORMANCE MATERIALS INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 337 MOMENTIVE PERFORMANCE MATERIALS INC.: DEALS, JANUARY 2021-JULY 2025

- TABLE 338 MOMENTIVE PERFORMANCE MATERIALS INC.: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 339 DUPONT: COMPANY OVERVIEW

- TABLE 340 DUPONT: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 341 DUPONT: DEALS, JANUARY 2021-JULY 2025

- TABLE 342 DUPONT: EXPANSIONS, JANUARY 2021-JULY 2025

- TABLE 343 TRINSEO: COMPANY OVERVIEW

- TABLE 344 KRATON CORPORATION: COMPANY OVERVIEW

- TABLE 345 TOTAL PLASTICS: COMPANY OVERVIEW

- TABLE 346 SIMONA AMERICA: COMPANY OVERVIEW

- TABLE 347 DSM: COMPANY OVERVIEW

- TABLE 348 INVIBIO: COMPANY OVERVIEW

- TABLE 349 AVIENT CORPORATION: COMPANY OVERVIEW

- TABLE 350 RTP COMPANY: COMPANY OVERVIEW

- TABLE 351 TEKNIPLEX: COMPANY OVERVIEW

- TABLE 352 TEKNOR APEX: COMPANY OVERVIEW

- TABLE 353 MITSUBISHI CHEMICALS ADVANCED MATERIALS: COMPANY OVERVIEW

- TABLE 354 WACKER CHIMIE: COMPANY OVERVIEW

- TABLE 355 HARDIE POLYMERS: COMPANY OVERVIEW

- TABLE 356 ELIX POLYMERS: COMPANY OVERVIEW

- TABLE 357 INNOVATIVE POLYMER COMPOUNDS: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MEDICAL POLYMER MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 MEDICAL POLYMER MARKET: RESEARCH DESIGN

- FIGURE 3 MEDICAL POLYMER MARKET: BOTTOM-UP APPROACH

- FIGURE 4 MEDICAL POLYMER MARKET: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: MEDICAL POLYMER MARKET TOP-DOWN APPROACH

- FIGURE 6 DEMAND-SIDE FORECAST PROJECTIONS

- FIGURE 7 MEDICAL POLYMER MARKET: DATA TRIANGULATION

- FIGURE 8 MEDICAL PLASTICS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 9 MEDICAL INSTRUMENTS & DEVICES SEGMENT TO RECORD FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 10 EXTRUSION TUBING SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 11 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 12 INCREASING DEMAND FROM MEDICAL INSTRUMENTS & DEVICES APPLICATION TO DRIVE MARKET DURING FORECAST PERIOD

- FIGURE 13 MEDICAL PLASTICS SEGMENT TO LEAD MEDICAL POLYMER MARKET DURING FORECAST PERIOD

- FIGURE 14 MEDICAL INSTRUMENTS & DEVICES SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 EXTRUSION TUBING SEGMENT TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- FIGURE 16 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 17 MEDICAL POLYMER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 PORTER'S FIVE FORCES ANALYSIS: MEDICAL POLYMER MARKET

- FIGURE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP FOUR APPLICATIONS

- FIGURE 20 KEY BUYING CRITERIA IN MAJOR APPLICATIONS

- FIGURE 21 MEDICAL POLYMER MARKET: VALUE CHAIN ANALYSIS

- FIGURE 22 MEDICAL POLYMER ECOSYSTEM

- FIGURE 23 MEDICAL POLYMER MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 24 IMPORT OF MEDICAL POLYMERS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 25 EXPORT OF MEDICAL POLYMERS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 26 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- FIGURE 27 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2022-2024

- FIGURE 28 AVERAGE SELLING PRICE OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

- FIGURE 29 INVESTMENT AND FUNDING SCENARIO, 2019-2023 (USD MILLION)

- FIGURE 32 LEGAL STATUS OF PATENTS, 2015-2024

- FIGURE 35 MEDICAL PLASTICS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 36 EXTRUSION TUBING SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 37 MEDICAL INSTRUMENTS & DEVICES TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- FIGURE 38 MEDICAL POLYMER MARKET SNAPSHOT

- FIGURE 39 NORTH AMERICA: MEDICAL POLYMER MARKET SNAPSHOT

- FIGURE 40 ASIA PACIFIC: MEDICAL POLYMER MARKET SNAPSHOT

- FIGURE 41 EUROPE: MEDICAL POLYMER MARKET SNAPSHOT

- FIGURE 42 REVENUE ANALYSIS OF KEY COMPANIES IN MEDICAL POLYMER MARKET, 2022-2024

- FIGURE 43 SHARES OF TOP FIVE COMPANIES IN MEDICAL POLYMER MARKET, 2024

- FIGURE 44 VALUATION OF KEY COMPANIES IN MEDICAL POLYMER MARKET, 2024

- FIGURE 45 FINANCIAL METRICS OF KEY COMPANIES IN MEDICAL POLYMER MARKET, 2024

- FIGURE 46 MEDICAL POLYMER MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 47 MEDICAL POLYMER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 48 MEDICAL POLYMER MARKET: COMPANY FOOTPRINT

- FIGURE 49 MEDICAL POLYMER MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 50 BASF: COMPANY SNAPSHOT

- FIGURE 51 SABIC: COMPANY SNAPSHOT

- FIGURE 52 COVESTRO AG: COMPANY SNAPSHOT

- FIGURE 53 CELANESE CORPORATION: COMPANY SNAPSHOT

- FIGURE 54 EVONIK INDUSTRIES: COMPANY SNAPSHOT

- FIGURE 55 ARKEMA: COMPANY SNAPSHOT

- FIGURE 56 SOLVAY: COMPANY SNAPSHOT

- FIGURE 57 KURARAY CO., LTD.: COMPANY SNAPSHOT

- FIGURE 58 DUPONT: COMPANY SNAPSHOT