PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708185

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708185

Lymphoma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

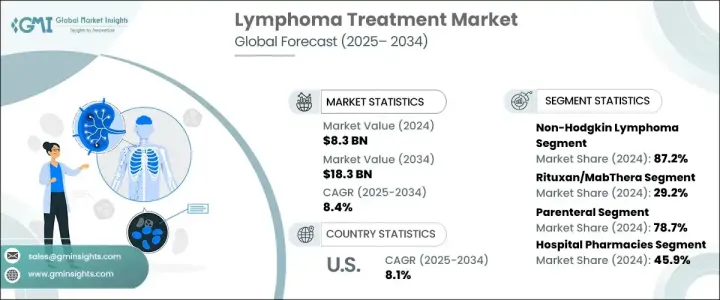

The Global Lymphoma Treatment Market reached USD 8.3 billion in 2024 and is projected to exhibit a CAGR of 8.4% from 2025 to 2034. Lymphoma, a type of cancer affecting the lymphatic system, arises from abnormal proliferation of lymphocytes, a form of white blood cell. It primarily manifests in lymph nodes and can also affect other tissues. There are two primary types non-Hodgkin lymphoma and Hodgkin lymphoma-distinguished by the presence of Reed-Sternberg cells in Hodgkin lymphoma. Symptoms often include lymphadenopathy, fever, fatigue, and appetite loss. The burden of Hodgkin lymphoma remains high, especially among young populations, while inadequate healthcare infrastructure in some regions contributes to lower survival rates. This disparity emphasizes the need for improved treatment approaches, particularly in low-income regions.

Non-Hodgkin lymphoma (NHL) dominates the market due to its higher prevalence and multiple subtypes, resulting in a larger patient population worldwide. Increasing incidence rates continue to propel the market's growth. The use of monoclonal antibody therapies, such as Rituximab, has revolutionized lymphoma treatment. Rituximab targets the CD20 molecule on B lymphocytes and has proven effective in managing both NHL and nodular lymphocyte predominant Hodgkin lymphoma (NLPHL). The therapy enhances response rates, prolongs remission duration, and boosts survival rates, reinforcing its position as a cornerstone in lymphoma treatment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $18.3 Billion |

| CAGR | 8.4% |

Parenteral administration accounted for 78.7% of the market share in 2024, underscoring its dominance. This method, which involves injecting medication directly into the bloodstream, ensures rapid drug absorption, making it ideal for aggressive lymphomas requiring immediate intervention. Parenteral routes allow for precise dosing and controlled delivery, which is critical for advanced therapies such as immunotherapy, CAR T-cell therapy, and high-dose chemotherapy. Patients who are unable to tolerate oral medications due to severe symptoms or bowel issues benefit from this approach. Furthermore, parenteral administration remains the preferred method for relapsed or refractory lymphoma cases that do not respond well to oral treatments.

Hospital pharmacies held the largest market share at 45.9% in 2024, driven by the widespread use of hospital-administered therapies such as chemotherapy, immunotherapy, and CAR T-cell therapies. These specialized treatments require careful preparation and monitoring, which is best handled within a hospital setting. Hospital pharmacies remain the primary source for these tailored medications and high-cost biologics. The growing volume of hospital admissions for specialized oncology care further reinforces the segment's substantial market share.

In the United Kingdom, the lymphoma treatment market is expected to witness consistent growth between 2025 and 2034. The increasing prevalence of lymphoma in the region is driving demand for innovative treatment solutions. Advancements in precision medicine, immunotherapy, and CAR T-cell therapies are meeting this demand. Additionally, initiatives such as the Life Sciences Industrial Strategy and Brexit-driven devolution efforts are strengthening the UK's capacity to innovate and produce domestic treatments, boosting the region's overall market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of lymphoma

- 3.2.1.2 Advancements in treatment options

- 3.2.1.3 Growing approval of novel targeted therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Delayed diagnosis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hodgkin lymphoma

- 5.3 Non-Hodgkin lymphoma

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Rituxan/MabThera

- 6.3 Revlimid

- 6.4 Imbruvica

- 6.5 Adcetris

- 6.6 Keytruda

- 6.7 Opdivo

- 6.8 Other drug types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Bayer

- 10.3 Biogen

- 10.4 BioGene

- 10.5 Bristol-Myers Squibb

- 10.6 Celgene

- 10.7 Eli Lilly and Company

- 10.8 F. Hoffmann-La Roche

- 10.9 Gilead Sciences

- 10.10 Incyte

- 10.11 Johnson & Johnson

- 10.12 Juno Therapeutics

- 10.13 Merck

- 10.14 Novartis

- 10.15 Seattle Genetics

- 10.16 Takeda Pharmaceutical