PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708181

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708181

Immunotoxins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

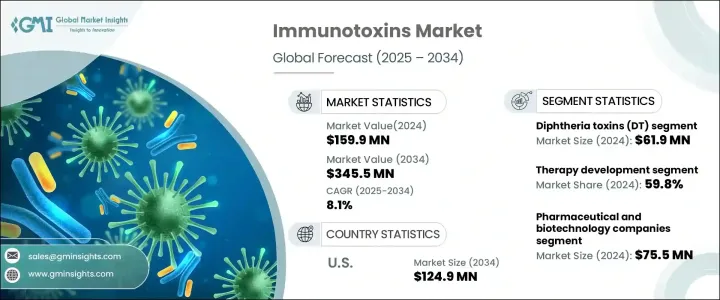

The Global Immunotoxins Market reached USD 159.9 million in 2024 and is expected to grow at a CAGR of 8.1% from 2025 to 2034. Immunotoxins are therapeutic agents that combine a monoclonal antibody or a targeting molecule with a potent toxin. Their mechanism involves binding the antibody to antigens present on the surface of target cells, such as cancerous or diseased cells. The toxin component then kills the targeted cells by disrupting essential cellular processes. The increasing adoption of targeted therapies for chronic conditions is a major driver of market growth. Targeted therapies, including immunotoxins, specifically attack disease-causing cells, reducing adverse reactions and improving patient outcomes. These benefits are driving the increased use of immunotoxin-based treatments in cancer and chronic disease management, fueling market expansion.

The market is segmented by toxin type into diphtheria toxins (DT), anthrax-based toxins, pseudomonas exotoxins (PE), ribosome-inactivating protein-based immunotoxins, and other immunotoxins. The diphtheria toxins (DT) segment accounted for USD 61.9 million in 2024 and is expected to grow at a CAGR of 8.1% during the forecast period. This growth is attributed to the strong therapeutic potential of diphtheria toxins, which work by inhibiting protein synthesis in targeted cells, leading to cell death. Denileukin diftitox, a fusion protein that combines diphtheria toxin with an IL-2 receptor-targeting fragment, exemplifies the cytocidal action that reinforces the growth of the DT segment. Ongoing research and regulatory approvals, particularly for diphtheria toxin-based immunotoxins, further contribute to the expansion of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $159.9 Million |

| Forecast Value | $345.5 Million |

| CAGR | 8.1% |

By application, the market is categorized into biomedical research and therapy development. The therapy development segment led the market with a 59.8% share in 2024. Its dominance is driven by the increasing prevalence of cancer and the rising use of immunotoxins in clinical settings. The growing incidence of hematological malignancies such as leukemia, lymphoma, and multiple myeloma is boosting the demand for immunotoxin-based therapies, further propelling market growth.

Based on end use, the market is divided into pharmaceutical and biotechnology companies, CROs and CMOs, academic and research institutes, and other end users. Pharmaceutical and biotechnology companies dominated the segment with USD 75.5 million in 2024. These companies invest extensively in research and development to create advanced immunotoxin therapies for cancer and chronic diseases, focusing on targeting diseased cells while preserving healthy ones. Their collaborations with CROs, CMOs, and academic institutions accelerate product commercialization and development, contributing significantly to market growth.

The U.S. immunotoxins market is expected to witness substantial growth, reaching USD 124.9 million by 2034. The increasing prevalence of cancer and rising mortality rates are driving demand for targeted immunotoxin-based therapies, further strengthening the country's market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer and chronic diseases

- 3.2.1.2 Expanding regulatory approvals for new immunotoxin therapies

- 3.2.1.3 Growing focus on targeted therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges related to cytotoxicity and manufacturing in the development of immunotoxins

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Toxin Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diphtheria toxins (DT)

- 5.3 Anthrax based toxins

- 5.4 Pseudomonas exotoxins (PE)

- 5.5 Ribosomes inactivating protein based immunotoxins

- 5.6 Other toxin types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Biomedical research

- 6.3 Therapy development

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 CROs and CMOs

- 7.4 Academic and research institutes

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abcam

- 9.2 Bio-Techne

- 9.3 Cayman Chemical

- 9.4 Creative Biolabs

- 9.5 Enzo Biochem

- 9.6 List Biological Labs

- 9.7 Merck KGaA

- 9.8 Quadratech Diagnostics

- 9.9 Santa Cruz Biotechnology

- 9.10 The Native Antigen Company

- 9.11 Thermo Fisher Scientific