PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708150

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708150

Cranial Implant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

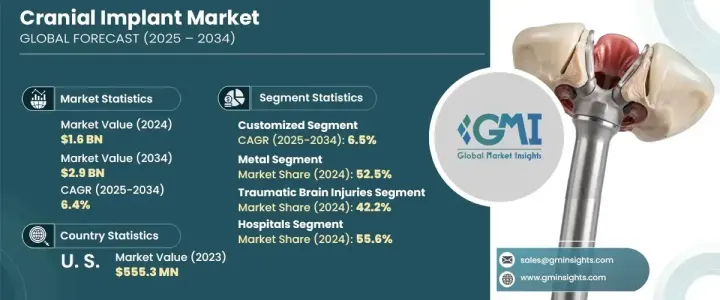

The Global Cranial Implant Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 6.4% between 2025 and 2034. The market is experiencing steady growth, driven by the rising prevalence of neurological disorders, traumatic brain injuries, and the increasing adoption of advanced surgical techniques. A growing number of patients worldwide require cranial reconstruction due to conditions such as strokes, epilepsy, Alzheimer's disease, and congenital skull deformities. With an aging global population and an uptick in accident-related head injuries, demand for high-quality cranial implants is expected to surge. Continuous advancements in 3D printing and biomaterials are revolutionizing the industry, making implants more precise, durable, and biocompatible. Furthermore, favorable regulatory policies in developed markets are accelerating product approvals, allowing companies to introduce innovative solutions more efficiently. Increasing healthcare investments and improved accessibility to neuro and trauma care in emerging economies also contribute to market expansion.

The market is divided into customized and non-customized products. In 2024, customized cranial implants generated USD 1 billion and are set for notable growth, with a projected CAGR of 6.5% over the next decade. These implants are gaining popularity due to their ability to provide a precise fit, enhancing both reconstructive outcomes and functional performance. Using advanced imaging techniques such as CT scans and MRIs, medical professionals can create patient-specific implants that align seamlessly with an individual's skull structure. This personalized approach significantly improves post-surgical recovery and aesthetic results, fueling the demand for customized solutions across the healthcare sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.4% |

Cranial implants are primarily made from metal, polymer, or ceramic materials. The metal segment dominated the market in 2024, holding a 52.5% share and generating USD 830.9 million in revenue. Titanium and its alloys remain the preferred choice due to their exceptional strength, biocompatibility, and long-term durability. Metal implants offer superior protection to the brain, making them ideal for patients recovering from traumatic injuries or complex skull surgeries. Compared to polymer-based implants, metal options provide enhanced longevity and lower failure rates, driving their widespread adoption in medical procedures.

North America Cranial Implant Market generated USD 640.6 million in 2024 and is projected to reach USD 1.2 billion by 2034. This growth is largely driven by the increasing incidence of traumatic brain injuries (TBI) and the region's advanced healthcare infrastructure. The United States, in particular, benefits from a supportive regulatory environment that encourages the development and commercialization of cutting-edge medical technologies. The adoption of AI-assisted imaging, 3D printing, and bioengineered materials is reshaping the landscape of cranial implants, enabling more efficient and customized treatment options. These technological advancements, combined with strong healthcare spending and high awareness of neurosurgical solutions, position North America as a key contributor to global market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing cases of traumatic brain injuries (TBI)

- 3.2.1.2 Growing prevalence of neurological disorders and skull deformities

- 3.2.1.3 Advancements in 3D printing and custom implant technologies

- 3.2.1.4 Increasing adoption of biocompatible and smart materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cranial implants and surgical procedures

- 3.2.2.2 Stringent regulatory approvals and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Customized

- 5.3 Non-customized

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Polymer

- 6.3.1 Polyetheretherketone (PEEK)

- 6.3.2 Polymethylmethacrylate (PMMA)

- 6.3.3 Other polymers

- 6.4 Ceramic

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Traumatic brain injuries

- 7.3 Tumor resection cases

- 7.4 Neurosurgical reconstructive procedures

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Neurosurgery centers

- 8.4 Academic and research institute

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3D Systems

- 10.2 Acumed LLC

- 10.3 Anatomics Pty Ltd

- 10.4 B. Braun SE

- 10.5 Brainlab

- 10.6 evonos GmbH & Co. KG

- 10.7 Integra LifeSciences

- 10.8 Johnson & Johnson

- 10.9 Kelyniam Global Inc.

- 10.10 KLS Martin

- 10.11 Medartis AG

- 10.12 Medtronic

- 10.13 Matrix Surgical USA

- 10.14 Renishaw plc.

- 10.15 Stryker Corporation

- 10.16 Zimmer Biomet