PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1699282

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1699282

Carbon Capture and Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

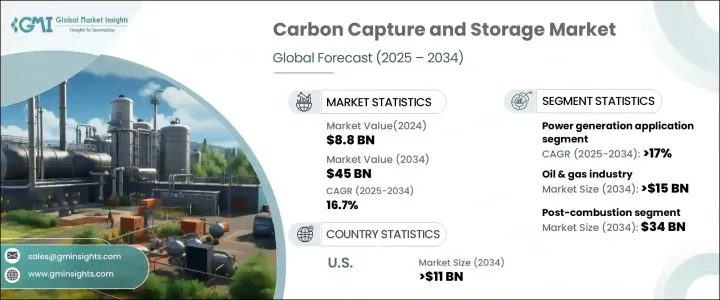

The Global Carbon Capture And Storage Market was valued at USD 8.8 billion in 2024 and is projected to grow at a CAGR of 16.7% between 2025 and 2034. The increasing urgency to curb greenhouse gas emissions and achieve decarbonization goals is driving significant investments in CCS technologies. Governments worldwide are implementing stringent environmental regulations, compelling industries to adopt advanced carbon capture solutions to meet compliance standards and mitigate their carbon footprint. Rising concerns over climate change, combined with the rapid industrial expansion and energy demands, are further propelling the need for cost-effective emission control technologies.

Companies across the energy, chemical, and manufacturing sectors are actively integrating CCS solutions into their operations to align with global sustainability initiatives. The growing focus on clean energy transition, coupled with advancements in carbon capture efficiency, is unlocking new opportunities for market expansion. Additionally, increasing research and development activities are fostering the innovation of next-generation CCS technologies that enhance scalability and operational feasibility. As industries strive to balance environmental responsibility with economic growth, CCS is emerging as a pivotal solution for achieving long-term carbon neutrality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $45 Billion |

| CAGR | 16.7% |

The market is segmented based on technology into pre-combustion, oxy-fuel combustion, and post-combustion. Post-combustion capture technology is expected to witness substantial growth, with forecasts indicating it will reach USD 34 billion by 2034. This technology is gaining traction due to its seamless integration with existing industrial setups, enabling large-scale adoption across power plants, refineries, and manufacturing facilities. As emission control becomes a priority, post-combustion systems are evolving with enhanced efficiency and cost-effectiveness, making them an attractive option for industries seeking viable carbon reduction strategies. The development of innovative absorbents and advanced filtration techniques is further boosting the performance and adoption of post-combustion technology, ensuring consistent market expansion.

In terms of application, the market spans power generation, chemical processing, and oil & gas, among other industries. The power generation segment captured a 36% share in 2024 and is expected to grow at a CAGR of 17% through 2034. The increasing deployment of CCS infrastructure to facilitate hydrogen production, storage, and distribution is a crucial factor fueling demand within this sector. As global energy consumption continues to rise, governments and utility providers are prioritizing CCS adoption to meet emission targets without compromising energy output. Power plants are leveraging CCS solutions to retrofit conventional energy systems, ensuring compliance with strict environmental policies while maintaining operational efficiency. The integration of CCS in renewable energy projects and carbon-negative initiatives is further solidifying its role in the evolving energy landscape.

The U.S. market generated USD 3.3 billion in 2024 and is projected to reach USD 11 billion by 2034. The nation's emphasis on reducing carbon emissions and modernizing energy infrastructure is accelerating CCS investments. Technological advancements in emission control systems, coupled with substantial funding for large-scale CCS projects, are driving market growth across the country. North America remains a key region for CCS expansion, with strategic partnerships and government incentives playing a vital role in fostering innovation and deployment. As industries strive for cleaner production methods, the U.S. market is set to experience robust growth, reinforcing its leadership in the global CCS landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (MTPA, USD Billion)

- 5.1 Key trends

- 5.2 Pre combustion

- 5.3 Post combustion

- 5.4 Oxy-Fuel combustion

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (MTPA, USD Billion)

- 6.1 Key trends

- 6.2 Oil and gas

- 6.3 Chemical processing

- 6.4 Power generation

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (MTPA, USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 Denmark

- 7.3.4 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 South Korea

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Air Products

- 8.2 Aker Solutions

- 8.3 Carbon Clean

- 8.4 Chevron

- 8.5 Dakota Gasification Company

- 8.6 Equinor

- 8.7 Exxon Mobil

- 8.8 Fluor

- 8.9 General Electric

- 8.10 Halliburton

- 8.11 Linde

- 8.12 Mitsubishi Heavy Industries

- 8.13 NRG Energy

- 8.14 Shell Cansolv

- 8.15 Siemens

- 8.16 SLB

- 8.17 Sulzer

- 8.18 TotalEnergies