PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1699266

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1699266

Rapid Influenza Diagnostic Tests (RIDT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

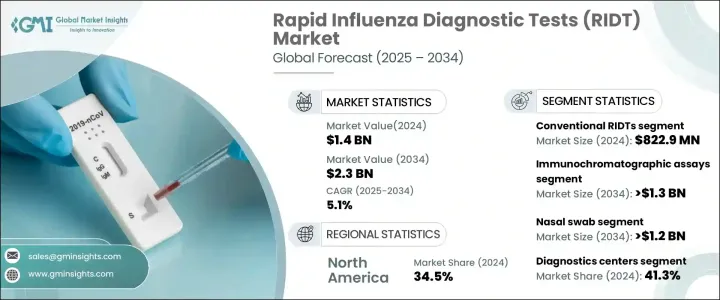

The Global Rapid Influenza Diagnostic Tests Market reached USD 1.4 billion in 2024 and is projected to grow at a CAGR of 5.1% from 2025 to 2034. The rising prevalence of seasonal flu, advancements in point-of-care testing, and continuous innovations in diagnostic methods are driving market growth. Governments worldwide are strengthening influenza surveillance and running awareness campaigns, further expanding the adoption of RIDTs. Technological advancements have significantly improved test accuracy, with digital RIDTs offering enhanced sensitivity and specificity.

The shift from qualitative to semi-quantitative RIDTs has increased their clinical relevance, and multiplexed tests capable of detecting multiple respiratory pathogens are becoming more common. Artificial intelligence (AI) and machine learning are optimizing test interpretation, reducing errors, and making diagnostics more accessible. Growing investments in healthcare infrastructure are also improving the availability of these tests. Regulatory bodies are supporting rapid influenza diagnosis through streamlined approvals and financial support for public health initiatives. Increased funding for diagnostic testing is helping expand public awareness, encouraging early detection and treatment, and driving the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.1% |

The RIDTs market is segmented based on product type, technology, sample type, end-use, and region. The conventional RIDTs segment generated USD 822.9 million in 2024. These tests remain widely used due to their affordability and ease of access, particularly in regions with limited healthcare infrastructure. Their simple design and low production cost make them ideal for use in public health programs, ensuring broad availability. The ease of use and minimal training requirements allow these tests to be implemented in a variety of settings, including clinics, workplaces, and schools. Fast results enable quick decision-making, making them highly effective in managing seasonal flu outbreaks.

By technology, immunochromatographic assays are expected to lead market growth with a projected CAGR of 5.9%, reaching over USD 1.3 billion by 2034. These tests offer high sensitivity and specificity, making them particularly valuable for detecting influenza in vulnerable populations, such as children and the elderly. The demand for immunochromatographic assays is increasing in decentralized healthcare settings, including pharmacies and urgent care centers. Their compact design and minimal equipment requirements make them well-suited for such locations. Continued technological advancements have further improved their speed and accuracy, making them a preferred choice among healthcare professionals.

Based on sample type, the nasal swab segment is projected to grow at a CAGR of 5.9%, surpassing USD 1.2 billion by 2034. Nasal swabs are widely used due to their ease of application and high accuracy in detecting influenza. They are less invasive than other sample collection methods, making them suitable for both children and adults. Their ability to capture high viral loads makes them effective in early influenza diagnosis, benefiting healthcare providers in both point-of-care and laboratory testing environments.

Diagnostic centers accounted for the highest end-use revenue share of 41.3% in 2024. These facilities offer advanced diagnostic technologies and employ trained professionals, ensuring accurate and efficient testing. The increasing demand for comprehensive diagnostic services, including multiplex testing for multiple respiratory infections, has contributed to the growing reliance on RIDTs in diagnostic centers. These facilities play a crucial role in large-scale influenza monitoring programs, reinforcing their market dominance.

North America captured the largest market share of 34.5% in 2024, driven by a well-established healthcare system, the widespread availability of rapid test kits, and the increasing adoption of point-of-care testing. The US market was valued at USD 331 million in 2021, rising to USD 365.8 million in 2022 and USD 401.3 million in 2023, reflecting its dominant position within the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of influenza

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising demand for early influenza diagnosis and management

- 3.2.1.4 Increasing popularity of rapid diagnostic tests

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals

- 3.2.2.2 Stringent regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pricing analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional RIDTs

- 5.3 Digital RIDTs

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunochromatographic assays

- 6.3 Lateral flow assays

- 6.4 PCR

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Sample Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Nasal swab

- 7.3 Throat swab

- 7.4 Other sample types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostic centers

- 8.3 Hospitals

- 8.4 Research laboratories

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3B BlackBio

- 10.2 Abbott

- 10.3 Access Bio

- 10.4 BD

- 10.5 bioMérieux

- 10.6 CHEMBIO

- 10.7 DiaSorin

- 10.8 Meridian

- 10.9 Quidel Corporation

- 10.10 Roche

- 10.11 SEKISUI

- 10.12 Siemens HEALTHINEERS

- 10.13 Thermo Fisher