PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1698271

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1698271

Epithelioma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

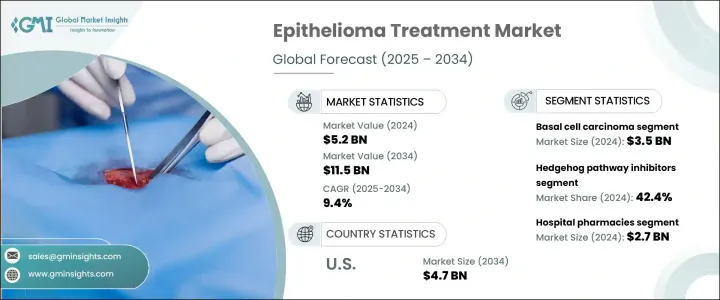

The Global Epithelioma Treatment Market was valued at approximately USD 5.2 billion in 2024 and is projected to grow at a 9.4% CAGR from 2025 to 2034. The market is expanding due to rising cases of epithelial tissue tumors, which may be benign or malignant, such as basal cell carcinoma and squamous cell carcinoma. Treatment focuses on removing tumors, preventing recurrence, and mitigating harmful effects. Increasing awareness, early detection, and government initiatives are key factors driving market growth. The growing number of skin cancer cases has fueled demand for innovative therapies, leading to significant advancements in treatment methods. Continuous R&D efforts and new drug approvals are further propelling market expansion. Regulatory bodies are supporting the introduction of advanced therapeutic solutions, improving patient access to effective treatment options. Medical technology improvements have also strengthened market growth by enabling better disease management.

The market is segmented by type, drug class, and distribution channel. Based on type, basal cell carcinoma accounted for the largest share, generating USD 3.5 billion in revenue in 2024. As the most prevalent form of non-melanoma skin cancer, its rising incidence has increased the demand for effective treatments. Factors such as prolonged UV exposure and shifting lifestyle patterns have contributed to the surge in cases. Greater awareness of early detection has further boosted the need for advanced therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 9.4% |

By drug class, hedgehog pathway inhibitors held the dominant share, contributing 42.4% of total market revenue in 2024. The segment growth is driven by the increasing prevalence of basal cell carcinoma, especially in regions with high sunlight exposure and aging populations. These inhibitors have demonstrated efficacy in treating advanced and metastatic cases, leading to their higher adoption over traditional chemotherapy and radiation therapies. Ongoing research and clinical trials are likely to introduce additional hedgehog pathway inhibitors, expanding treatment options for patients.

Regarding distribution channels, hospital pharmacies emerged as the leading segment, generating USD 2.7 billion in 2024. These pharmacies play a crucial role in providing immediate access to medications for inpatients undergoing treatment for epithelioma. The rising number of hospital admissions for basal cell carcinoma and squamous cell carcinoma has contributed to segment expansion. Hospital pharmacies also facilitate supportive care services, ensuring comprehensive treatment and improving patient outcomes.

Regionally, North America is a key player in the epithelioma treatment market. The United States, in particular, is projected to witness substantial growth, with market revenue increasing from USD 2 billion in 2023 to USD 4.7 billion by 2034. The country benefits from a favorable regulatory landscape that promotes the adoption of advanced therapies. Regulatory approvals for novel treatments are expected to drive market progression, strengthening the region's dominance in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of skin cancer

- 3.2.1.2 Advancements in targeted therapies and immunotherapies

- 3.2.1.3 Supportive healthcare infrastructure and awareness campaigns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Limited efficacy and adverse effects in advanced stages of the disease

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Basal cell carcinoma

- 5.3 Squamous cell carcinoma

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hedgehog pathway inhibitors

- 6.3 Immune checkpoint inhibitors

- 6.4 Chemotherapeutic agents

- 6.5 Other drug classes

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

- 7.5 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amgen

- 9.2 AstraZeneca

- 9.3 BeiGene

- 9.4 Bristol-Myers Squibb

- 9.5 F. Hoffmann-La Roche

- 9.6 Johnson & Johnson

- 9.7 Merck and Co.

- 9.8 Novartis

- 9.9 Pfizer

- 9.10 Regeneron Pharmaceuticals

- 9.11 Sanofi

- 9.12 Sun Pharmaceutical Industries