PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1698228

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1698228

Atopic Dermatitis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

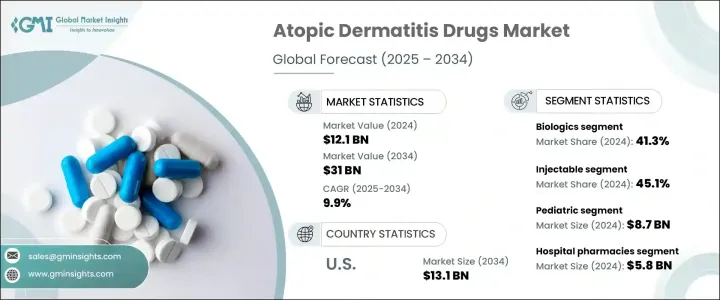

The Global Atopic Dermatitis Drugs Market was valued at USD 12.1 billion in 2024 and is projected to grow at a 9.9% CAGR from 2025 to 2034. Atopic dermatitis drugs help manage skin inflammation, itching, and dryness, targeting flare-ups and controlling the condition. These treatments include topical medications, systemic therapies, and biologics, chosen based on disease severity. The rising prevalence of atopic dermatitis, strong drug pipelines, and increased investment in research and development are fueling market growth. Pharmaceutical companies are launching new products, and positive clinical trial results are driving revenue expansion.

In 2023, the atopic dermatitis drugs market was worth USD 11.1 billion. The biologics segment led the market in 2024, holding a 41.3% revenue share, driven by higher efficacy and long-term symptom control. The demand for biologics continues to rise due to their superior treatment outcomes and growing product approvals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.1 Billion |

| Forecast Value | $31 Billion |

| CAGR | 9.9% |

By route of administration, the market is divided into injectable, topical, and oral treatments. The injectable segment dominated in 2024 with a 45.1% revenue share. New biologic injections targeting inflammatory pathways, such as IL-4, IL-13, and JAK inhibitors, are expanding treatment options. Regulatory approvals have accelerated product launches, increasing accessibility and adoption rates in major markets.

The patient demographic segmentation includes pediatric and adult categories. The pediatric segment led with USD 8.7 billion in revenue in 2024, primarily due to the high incidence of atopic dermatitis in children. The demand for pediatric therapies continues to grow as regulatory bodies approve more treatments tailored for younger patients. Expedited approvals for biologic formulations specifically designed for pediatric use are further driving market expansion.

Distribution channels include hospital pharmacies, retail pharmacies, and e-commerce. Hospital pharmacies accounted for USD 5.8 billion in revenue in 2024. These pharmacies play a crucial role in managing patients who require specialized or systemic treatments, ensuring proper monitoring of therapy outcomes and potential side effects.

The U.S. market has witnessed significant growth, with revenue rising from USD 4.7 billion in 2023 to a projected USD 13.1 billion by 2034. Increased awareness efforts and advocacy initiatives are enhancing research funding and improving patient access to advanced treatment options. Regulatory agencies continue to fast-track the approval of biologics, particularly for severe cases and pediatric patients, further supporting market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of atopic dermatitis

- 3.2.1.2 Advancements in biologic therapies

- 3.2.1.3 Growing awareness and access to dermatological care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biologic and advanced therapies

- 3.2.2.2 Side effects and compliance issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Calcineurin inhibitors

- 5.4 Biologics

- 5.5 Phosphodiesterase-4 (PDE-4) inhibitors

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Patient Demographics, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Arcutis Biotherapeutics

- 10.3 Eli Lilly and Company

- 10.4 Galderma Laboratories

- 10.5 Incyte Corporation

- 10.6 Leo Pharma

- 10.7 Maruho

- 10.8 Novartis

- 10.9 Otsuka Pharmaceutical

- 10.10 Pfizer

- 10.11 Regeneron Pharmaceuticals

- 10.12 Sanofi

- 10.13 Viatris