PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685233

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685233

Reprocessed Medical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

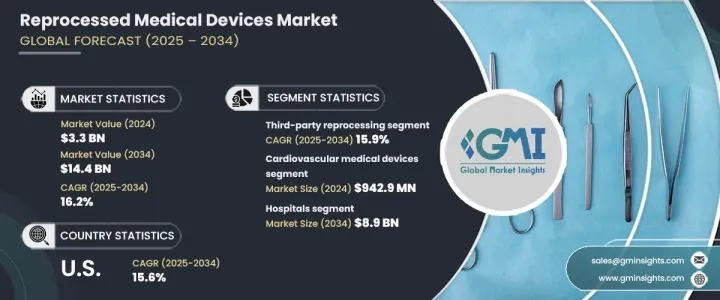

The Global Reprocessed Medical Devices Market reached USD 3.3 billion in 2024 and is set to expand at a CAGR of 16.2% from 2025 to 2034. This growth is driven by advancements in reprocessing technology, rising demand for single-use device reprocessing, and a strong focus on infection control. The expansion of healthcare services in developing regions also plays a crucial role in market growth. Educational programs highlighting the safety, efficiency, and environmental benefits of reprocessed devices have led to greater acceptance among healthcare providers and patients, further boosting market expansion.

Environmental concerns are another key factor influencing the market. The need to reduce medical waste is increasing, prompting healthcare providers to adopt sustainable practices. Reprocessing medical devices minimizes waste, aligns with global sustainability efforts, and ensures compliance with strict environmental regulations. These factors continue to drive the demand for reprocessed devices worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $14.4 Billion |

| CAGR | 16.2% |

Reprocessed medical devices, originally designed for single use, undergo thorough cleaning, disinfection, sterilization, and testing to meet high safety and performance standards before reuse. The market is segmented by product type, with cardiovascular medical devices generating the highest revenue of USD 942.9 million in 2024.

The market is also categorized by reprocessing type, which includes third-party reprocessing and in-house reprocessing. Third-party reprocessing accounted for USD 2.7 billion in 2024 and is projected to grow at a CAGR of 15.9% through 2034. These specialized services provide significant cost savings for hospitals and medical centers, ensuring devices meet rigorous safety and regulatory requirements. The expertise of third-party reprocessors helps healthcare facilities maintain compliance while reducing operational costs.

In terms of end users, hospitals represent the dominant market segment, expected to reach USD 8.9 billion by 2034. Cost pressures in the healthcare industry continue to rise, making reprocessed medical devices an attractive alternative to new equipment. Hospitals can optimize budgets by reusing devices without compromising patient safety. Additionally, the healthcare sector's push for sustainability is increasing the adoption of reprocessed devices, reducing the demand for single-use plastics, and lowering the environmental impact.

The U.S. reprocessed medical devices market was valued at USD 1.4 billion in 2024 and is expected to grow at a CAGR of 15.6% through 2034. Rising healthcare costs have led hospitals and medical centers to seek cost-effective solutions. The presence of clear regulatory guidelines set by the FDA ensures that reprocessed devices meet strict safety and performance standards, fostering confidence among healthcare providers and driving adoption across the country.

.Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Favorable regulatory landscape regarding sustainable waste disposal methods

- 3.2.1.2 Affordable costs coupled with the strengthening network of distributors in emerging economies

- 3.2.1.3 Growing use of reprocessed products in numerous cardiac surgeries and blood pressure monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of surgical site infections

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Gap analysis

- 3.10 Steps involved in medical device reprocessing

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 — 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular medical devices

- 5.2.1 Blood pressure cuffs/tourniquet cuffs

- 5.2.2 Diagnostic electrophysiology catheters

- 5.2.3 Electrophysiology cables

- 5.2.4 Cardiac stabilization and positioning devices

- 5.2.5 Deep vein compression sleeves (DVT)

- 5.2.6 Other cardiovascular medical devices

- 5.3 Laparoscopic

- 5.3.1 Endoscopic trocars and components

- 5.3.2 Harmonic scalpels

- 5.4 Orthopedic/arthroscopic

- 5.5 Gastroenterology and urology

- 5.5.1 Gastroenterology biopsy devices

- 5.5.2 Urology biopsy devices

- 5.6 General surgery equipment

- 5.6.1 Infusion pressure bags

- 5.6.2 Balloon inflation devices

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2021 — 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Third-party reprocessing

- 6.3 In-house reprocessing

Chapter 7 Market Estimates and Forecast, By End Use, 2021 — 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 — 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arjo

- 9.2 Boston Scientific

- 9.3 Cardinal Health

- 9.4 GE Healthcare

- 9.5 Halomedicals Systems

- 9.6 INNOVATIVE HEALTH

- 9.7 Johnson & Johnson

- 9.8 MEDLINE

- 9.9 Medtronic

- 9.10 SOMA TECH

- 9.11 STERIS

- 9.12 Stryker

- 9.13 SURETECH MEDICAL

- 9.14 Teleflex

- 9.15 VANGUARD