PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685152

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685152

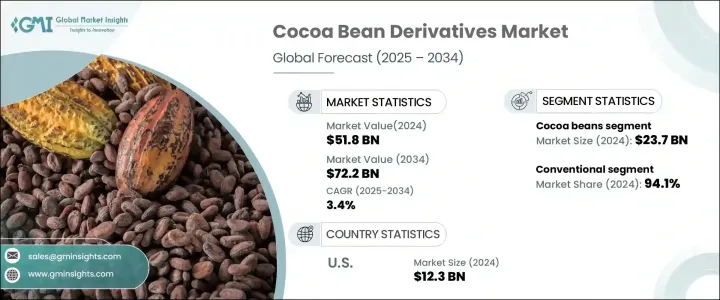

Cocoa Bean Derivatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Cocoa Bean Derivatives Market, valued at USD 51.8 billion in 2024, is on track for steady expansion, projected to grow at a CAGR of 3.4% between 2025 and 2034. As a critical component of the broader cocoa industry, this market encompasses various products that play a fundamental role in the food, beverage, cosmetics, and pharmaceutical sectors. With cocoa derivatives widely recognized for their rich flavor, nutritional benefits, and functional properties, demand is steadily increasing across multiple industries.

Cocoa-based products have witnessed a surge in popularity, largely driven by growing consumer preference for premium-quality chocolates, clean-label ingredients, and ethically sourced raw materials. Health-conscious consumers are also fueling this growth, given cocoa's high antioxidant content and associated wellness benefits. Meanwhile, sustainability concerns and ethical sourcing practices have reshaped the cocoa industry, with businesses increasingly focusing on transparent supply chains and fair-trade initiatives. Advances in processing technologies have further optimized production efficiency, reducing costs while ensuring the highest product quality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $51.8 Billion |

| Forecast Value | $72.2 Billion |

| CAGR | 3.4% |

By type, the cocoa bean derivatives market includes cocoa butter, cocoa powder, and other essential derivatives. Cocoa beans, the fundamental raw material, generated USD 23.7 billion in 2024, making them the most valuable segment of the market. Various factors, including weather conditions, crop yields, and global supply-demand dynamics, influence the value of cocoa beans. Cocoa butter, renowned for its smooth texture and rich taste, commands a substantial market share, particularly in confectionery and personal care products.

The market is also segmented into organic and conventional cocoa derivatives. Conventional products accounted for a dominant 94.1% share in 2024, primarily due to cost-effective production methods involving synthetic fertilizers and pesticides. These products remain widely available, meeting the needs of large-scale food manufacturers and chocolatiers. However, organic cocoa derivatives are gaining momentum as consumers increasingly gravitate toward sustainable, ethically sourced, and chemical-free alternatives. This shift is especially evident among premium chocolate brands and wellness-oriented food manufacturers, where demand for organic, non-GMO, and fair-trade certified ingredients continues to grow.

The U.S. cocoa bean derivatives market stood at USD 12.3 billion in 2024, reflecting robust growth driven by heightened demand for high-quality chocolate and plant-based products. Consumers in the U.S. are increasingly favoring cocoa-based items rich in flavonoids, antioxidants, and natural health benefits. This trend extends beyond food and beverages, with cocoa butter and cocoa powder gaining traction in the cosmetics and pharmaceutical industries. Their skin-nourishing and therapeutic properties make them sought-after ingredients in skincare formulations, while pharmaceutical applications leverage cocoa's bioactive compounds for various health benefits.

With an expanding consumer base, rising health consciousness, and ongoing innovation in cocoa processing, the global cocoa bean derivatives market is positioned for long-term growth. As brands continue to prioritize sustainability and premium product offerings, demand for high-quality cocoa derivatives will remain strong across diverse industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 The growing global consumption of chocolate products

- 3.6.1.2 Growing adoption of cocoa derivatives in non-food applications

- 3.6.1.3 Advancements in manufacturing technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Competition from other food and beverage ingredients

- 3.6.2.2 Fluctuating cocoa bean prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cocoa butter

- 5.3 Cocoa powder

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Category, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.3 Personal care

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Barry Callebaut

- 9.2 Cargill

- 9.3 CEMOI

- 9.4 Cocoa Touton

- 9.5 ECOM Agroindustrial

- 9.6 Ecuakao Group

- 9.7 Ferrero

- 9.8 Indcre

- 9.9 JB Foods

- 9.10 Mondelez International

- 9.11 Moner Cocoa

- 9.12 Natra

- 9.13 Nestlé

- 9.14 Olam Group

- 9.15 United Cocoa Processor