PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684785

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684785

AI in Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

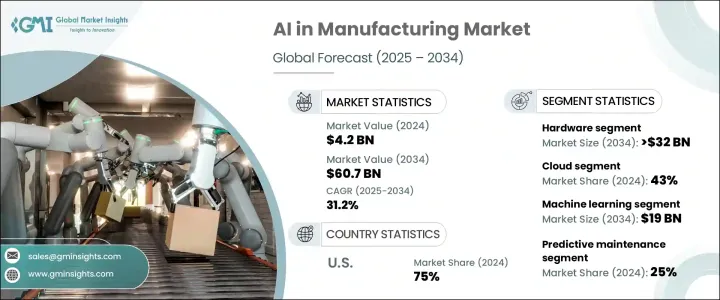

The Global AI In Manufacturing Market was valued at USD 4.2 billion in 2024 and is projected to grow at a CAGR of 31.2% between 2025 and 2034. The increasing need for streamlined outsourcing solutions within the manufacturing sector is driving AI adoption. Companies are integrating AI to enhance production efficiency, cut costs, and scale operations by automating processes such as production control, inspection, and inventory management. The rising availability of AI-powered solutions is benefiting businesses of all sizes, from large manufacturers to small and medium enterprises. Governments worldwide are prioritizing AI research and development, offering financial incentives such as funding programs, tax breaks, and regulatory support to boost AI implementation. These initiatives are designed to drive innovation, improve productivity, and reduce costs across various industries.

The market is segmented based on components into hardware, software, and services. In 2024, the hardware segment held a market share exceeding 55% and is expected to surpass USD 32 billion by 2034. The rising demand for advanced computing hardware is fueling this growth, as AI applications in manufacturing, such as robotics, predictive maintenance, and quality control, require high-performance components for real-time data processing. Machine learning and deep learning algorithms are also driving the need for powerful hardware to improve AI performance. Rapid advancements in data processing capabilities are enabling greater automation, enhanced productivity, and better decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $60.7 Billion |

| CAGR | 31.2% |

By deployment model, the market is categorized into on-premises and cloud solutions. In 2024, the cloud segment accounted for about 43% of the market. As companies across industries embrace digital transformation, the demand for cloud-based AI solutions is rising, enhancing competitiveness in manufacturing. Cloud computing offers flexibility and scalability, reducing operational costs and streamlining processes. Additionally, remote implementation allows for enhanced data storage and processing, which is critical for AI applications that rely on extensive datasets. Cloud-based solutions also enable real-time collaboration between manufacturers, suppliers, and customers, improving decision-making and accelerating time to market.

The market is also segmented by technology, including machine learning, computer vision, natural language processing, and context-aware computing. Machine learning led the market and is projected to generate around USD 19 billion by 2034. This growth is attributed to the increasing use of machine learning for intelligent automation and data-driven decision-making. AI-driven quality control solutions improve product inspection accuracy, minimizing production losses. Machine learning adoption in manufacturing is also being propelled by the rise of IoT technologies, which collect, analyze, and process data for optimized operations.

The market is further divided by application, including quality management, predictive maintenance, inventory management, energy management, industrial robotics, and others. Predictive maintenance held the largest share in 2024 at approximately 25%. AI-powered predictive maintenance solutions use machine learning algorithms to monitor and assess equipment performance in real-time, helping businesses prevent failures, reduce maintenance costs, and minimize production disruptions. The increasing need for higher productivity and reduced downtime is driving demand for these systems.

The United States led the North America AI in manufacturing market in 2024, holding about 75% of the regional share. The country's strong government support for AI-driven smart manufacturing is a key factor in market growth. Policymakers are prioritizing automation and advanced technologies to enhance the competitiveness of the nation's manufacturing sector. In addition, a focus on strengthening supply chain resilience and optimizing production efficiency is further driving AI adoption in the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Service providers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Evolution of AI in manufacturing

- 3.9 Use cases

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 The growing need for automation

- 3.10.1.2 Rapid developments in machine learning technologies

- 3.10.1.3 Adoption of AI-powered predictive maintenance solutions

- 3.10.1.4 Increasing investment in industrial automation

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Data privacy concerns

- 3.10.2.2 Lack of skilled professionals

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Processors

- 5.2.1.1 Central Processing Units (CPU)

- 5.2.1.2 Graphics Processing Units (GPU)

- 5.2.1.3 Field Programmable Gate Arrays (FPGA)

- 5.2.1.4 Application Specific Integrated Circuits (ASIC)

- 5.2.1.5 Tensor Processing Units (TPU)

- 5.2.2 Memory & storage

- 5.2.3 Networking hardware

- 5.2.1 Processors

- 5.3 Software

- 5.4 Services

- 5.4.1 Professional service

- 5.4.2 Managed service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Machine learning

- 7.3 Computer vision

- 7.4 Natural language processing

- 7.5 Context-aware computing

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Quality management

- 8.3 Predictive maintenance

- 8.4 Inventory management

- 8.5 Energy management

- 8.6 Industrial robotics

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Electronics

- 9.4 Pharmaceuticals

- 9.5 Heavy machinery

- 9.6 Food & beverage

- 9.7 Aerospace & defense

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 South Korea

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 UAE

- 10.5.2 South Africa

- 10.5.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 AWS

- 11.3 Cognex

- 11.4 Dassault

- 11.5 Fanuc

- 11.6 GE

- 11.7 Google

- 11.8 Honeywell

- 11.9 IBM

- 11.10 Intel

- 11.11 Microsoft

- 11.12 NVIDIA

- 11.13 Oracle

- 11.14 PTC

- 11.15 Qualcomm

- 11.16 Rockwell

- 11.17 SAP

- 11.18 Schneider

- 11.19 Siemens

- 11.20 Xilinx