PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684687

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684687

Connected Vehicle Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

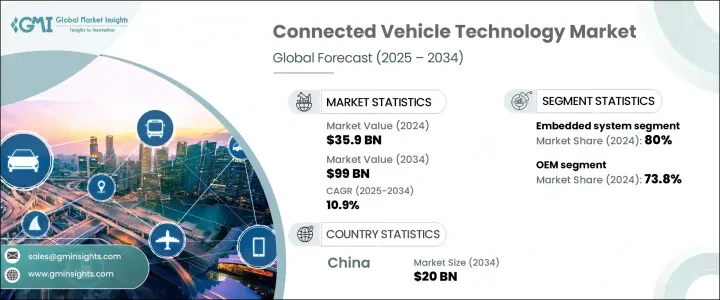

The Global Connected Vehicle Technology Market, valued at USD 35.9 billion in 2024, is set to expand at a CAGR of 10.9% between 2025 and 2034. The growth is driven by the rapid adoption of digital solutions and the increasing demand for smarter, safer, and more efficient transportation. This growth is fueled by government incentives such as tax breaks on vehicle safety features and subsidies for car purchases, which encourage both consumers and manufacturers to embrace cutting-edge automotive technologies. Connectivity has become an essential aspect of modern vehicle design, with automakers focusing on integrating advanced telematics, infotainment, and safety systems into their models. As technology continues to evolve, the growing use of artificial intelligence, 5G networks, and cloud-based platforms is enhancing vehicle-to-everything (V2X) communication, improving overall driving experiences, and ensuring higher safety standards.

The rising popularity of electric and autonomous vehicles is also propelling market expansion, as these vehicles rely heavily on embedded systems for navigation, diagnostics, and remote monitoring. Automakers are increasingly collaborating with technology companies to develop secure, high-performance digital solutions that enhance connectivity while maintaining cybersecurity. Consumer expectations are shifting towards personalized, seamless digital experiences within their vehicles, further pushing manufacturers to innovate. With the rise of over-the-air (OTA) updates, car manufacturers can now enhance vehicle functionality post-purchase, keeping cars up to date with the latest software improvements. This trend is making connected vehicle technology a necessity rather than an option, accelerating its adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.9 Billion |

| Forecast Value | $99 Billion |

| CAGR | 10.9% |

The market for connected vehicle technology is primarily divided into V2X communication and embedded systems. Embedded systems commanded the largest share in 2024 due to their direct integration into vehicles during the manufacturing process. These systems include telematics, infotainment, and navigation solutions that improve user experience, enhance vehicle performance, and enable real-time data exchange. With the push toward autonomous driving, embedded systems are becoming even more critical, supporting advanced driver-assistance systems (ADAS) and predictive maintenance solutions. Automakers are leveraging AI-driven analytics to optimize performance and increase road safety, making embedded systems the backbone of the connected vehicle ecosystem.

Connected vehicle technology is utilized by two major segments: original equipment manufacturers (OEMs) and the aftermarket. In 2024, the OEM segment held a commanding 73.8% market share, reflecting the industry's strong focus on factory-installed connectivity solutions. Manufacturers are embedding telematics and V2X communication capabilities into new vehicles, addressing growing consumer demands for seamless digital integration. This direct integration enhances vehicle safety, optimizes performance, and improves driving efficiency, positioning OEMs as the primary drivers of market growth. As more automakers invest in smart manufacturing and cloud-based platforms, the role of OEMs in shaping the future of connected mobility continues to expand.

China connected vehicle technology market is on track to generate USD 20 billion by 2034, driven by aggressive marketing campaigns, increasing vehicle sales, and a strong consumer appetite for high-tech automotive features. The country's commitment to reducing emissions and advancing smart transportation solutions is also accelerating adoption. The Asia-Pacific region as a whole is witnessing rapid market expansion, with governments and automotive leaders actively promoting digital transformation in the sector. North America is experiencing similar momentum as consumer interest in advanced connectivity features grows. A rising number of car buyers now prioritize vehicles equipped with integrated digital solutions, solidifying connected vehicle technology as a core component of the automotive industry's future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Automotive OEMs

- 3.1.2 Technology providers

- 3.1.3 Telecommunication companies

- 3.1.4 Platform developers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Use cases of connected vehicle technology

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for safety features

- 3.8.1.2 Advancements in 5G connectivity

- 3.8.1.3 Integration of AI and machine learning

- 3.8.1.4 Growing government regulations and incentives

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Data privacy and security concerns

- 3.8.2.2 High cost of implementation

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034, ($Bn)

- 5.1 Key trends

- 5.2 V2X communication

- 5.3 Embedded system

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021-2034, ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Heavy Commercial Vehicles (HCVs)

- 6.4 Electric Vehicles (EVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034, ($Bn)

- 7.1 Key trends

- 7.2 Autonomous driving

- 7.3 Mobility as a Service (MaaS)

- 7.4 Infotainment

- 7.5 Fleet management

- 7.6 Safety and security

- 7.7 Vehicle diagnostics and maintenance

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034, ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Atos

- 10.3 AWS

- 10.4 Bosch

- 10.5 Cisco

- 10.6 Continental

- 10.7 Denso

- 10.8 Ericsson

- 10.9 Harman (Samsung Electronics)

- 10.10 IBM

- 10.11 Infineon Technologies

- 10.12 Intel

- 10.13 Microsoft

- 10.14 Mobileye

- 10.15 NXP Semiconductors

- 10.16 Orange

- 10.17 Qualcomm

- 10.18 Telenor

- 10.19 Verizon

- 10.20 Vodafone