PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684558

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684558

Calcineurin Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

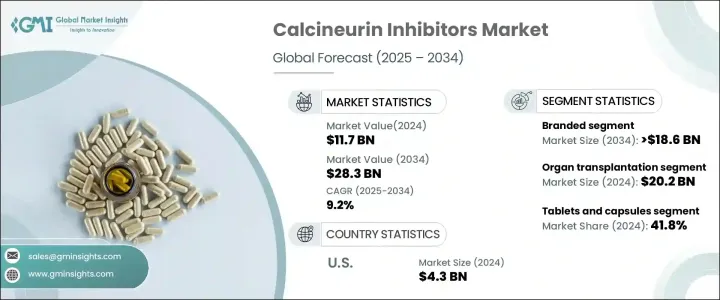

The Global Calcineurin Inhibitors Market, valued at USD 11.7 billion in 2024, is projected to expand at a CAGR of 9.2% from 2025 to 2034. This market growth is primarily fueled by the increasing prevalence of autoimmune disorders and the rising number of organ transplants across the globe. Calcineurin inhibitors are essential in transplant medicine, as they suppress the immune system to prevent organ rejection, particularly in high-demand procedures such as kidney, liver, heart, and lung transplants. The critical role these medications play in ensuring transplant success continues to drive their adoption, thus enhancing their market demand. As the global healthcare landscape evolves, the increasing number of individuals requiring organ transplants-due to factors like aging populations and the rising incidence of organ failure-has further solidified the demand for these immunosuppressive drugs.

Within the calcineurin inhibitors market, the competition is segmented into branded and generic options. The branded segment, accounting for a significant portion of the market, is anticipated to lead with a growth rate of 9%. By 2034, it is expected to reach USD 18.6 billion. Branded calcineurin inhibitors remain the preferred choice among healthcare professionals because of their proven efficacy, strong safety profiles, and solid backing from clinical trial data. These products are manufactured to meet rigorous quality standards, ensuring consistency and reliability. This makes them the go-to option in critical transplant protocols, where success depends on minimizing the risk of organ rejection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 9.2% |

Calcineurin inhibitors are utilized primarily in three areas: organ transplantation, autoimmune diseases, and other specialized applications. The organ transplantation segment is expected to generate USD 20.2 billion between 2025 and 2034, underlining the central role of these drugs in post-transplant care. Their ability to manage the body's immune response effectively ensures the survival of transplanted organs, making them indispensable in transplant medicine worldwide. As immunosuppressive therapy remains the cornerstone of preventing organ rejection, calcineurin inhibitors continue to dominate this segment.

In the United States, the calcineurin inhibitors market, valued at USD 4.3 billion in 2024, is projected to grow at a CAGR of 8.4% from 2025 to 2034. The U.S. is a key market for these medications, with the presence of world-leading transplant centers, strong reimbursement policies, and a robust investment in research and development driving the market forward. Moreover, the high rates of chronic conditions such as diabetes and hypertension, which often lead to organ failure, further amplify the demand for calcineurin inhibitors. These factors position the U.S. as a dominant force in the global market, ensuring continued growth and innovation within the sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of organ transplant procedures

- 3.2.1.2 Rising prevalence of autoimmune diseases

- 3.2.1.3 Surge in immunosuppressive research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects and the availability of alternative treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.2.1 Tacrolimus

- 5.2.2 Cyclosporine

- 5.2.3 Other branded products

- 5.3 Generic

- 5.3.1 Tacrolimus

- 5.3.2 Cyclosporine

- 5.3.3 Other generic products

Chapter 6 Market Estimates and Forecast, By Dosage, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets and capsules

- 6.3 Ointments

- 6.4 Injections

- 6.5 Other dosage forms

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Organ transplantation

- 7.3 Autoimmune disease

- 7.4 Other indications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 abbvie

- 9.2 astellas

- 9.3 Aurinia

- 9.4 Biocon

- 9.5 Dr. Reddy’s

- 9.6 Glenmark

- 9.7 LUPIN

- 9.8 Novartis

- 9.9 Roche

- 9.10 VIATRIS