PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684518

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1684518

Lithography Metrology Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

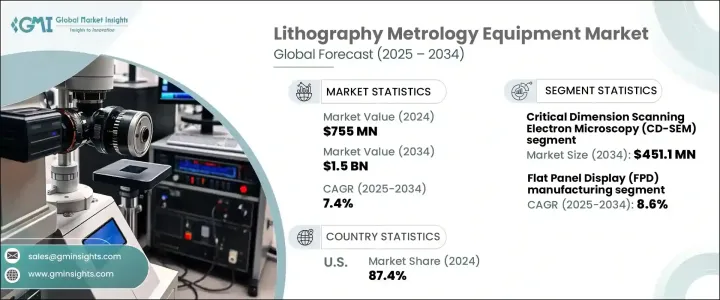

The Global Lithography Metrology Equipment Market reached USD 755 million in 2024 and is poised to grow at an impressive CAGR of 7.4% between 2025 and 2034. This growth is primarily driven by the surging demand for advanced consumer electronics such as smartphones, tablets, and wearables, which continue to dominate the global market. These devices rely on compact, high-performance integrated circuits (ICs), placing a premium on cutting-edge lithography processes. These advanced techniques are critical for achieving higher chip densities, which are necessary to deliver the next-generation capabilities demanded by consumers and industries alike. Additionally, the rising focus on innovations in semiconductor fabrication, 5G technology adoption, and AI applications is fueling the need for precision metrology solutions. Manufacturers are increasingly investing in state-of-the-art equipment to meet the evolving demands of industries that prioritize accuracy and efficiency in production processes.

By technology, the market is segmented into overlay metrology, Atomic Force Microscopy (AFM), Critical Dimension Scanning Electron Microscopy (CD-SEM), optical metrology, and scatterometry. Among these, CD-SEM is set to dominate, with its market value expected to reach USD 451.1 million by 2034. The unparalleled precision of CD-SEM in measuring nanoscale dimensions makes it indispensable for semiconductor fabrication. This technology ensures unmatched accuracy during the inspection of mask patterns, lithography structures, and intricate designs, enabling the production of highly miniaturized and complex semiconductors. The growing demand for next-generation chips is pushing advancements in CD-SEM technology, with a strong focus on achieving higher resolution, increased throughput, and enhanced automation to meet industry standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $755 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 7.4% |

The market is further categorized based on applications, which include LED manufacturing, semiconductor manufacturing, Flat Panel Display (FPD) manufacturing, MEMS (Micro-Electro-Mechanical Systems), and others. FPD manufacturing is projected to experience the highest growth, with a CAGR of 8.6% from 2025 to 2034. The rising adoption of larger, high-resolution displays and cutting-edge OLED and microLED technologies has significantly amplified the demand for precise metrology tools. These tools play a pivotal role in measuring layer thickness, alignment, and resolution, ensuring optimal display performance and quality, which are crucial for maintaining a competitive edge in the electronics market.

In the United States, the lithography metrology equipment market accounted for a substantial 87.4% share in 2024. The country's dominance stems from its advanced semiconductor manufacturing capabilities and strong R&D infrastructure. Investments in cutting-edge nodes, including 5nm and beyond, are accelerating the adoption of EUV lithography and advanced metrology solutions. Additionally, the growing focus on 3D packaging technologies and the widespread implementation of AI, IoT, and 5G are further driving the demand for innovative and precise lithography metrology equipment in the United States.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in semiconductor technology

- 3.6.1.2 Rising demand for consumer electronics

- 3.6.1.3 Growth in 5G and artificial intelligence (AI) applications

- 3.6.1.4 Increasing focus on foundry and memory manufacturing

- 3.6.1.5 Technological advancements in optical and non-optical metrology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced metrology equipment

- 3.6.2.2 Complexity in measuring advanced nodes

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million) (Million Units)

- 5.1 Key trends

- 5.2 Optical metrology

- 5.3 Critical dimension scanning electron microscopy (CD-SEM)

- 5.4 Overlay metrology

- 5.5 Atomic force microscopy (AFM)

- 5.6 Scatterometry

Chapter 6 Market Estimates & Forecast, By Product, 2021-2034 (USD Million) (Million Units)

- 6.1 Key trends

- 6.2 Chemical control equipment

- 6.3 Gas control equipment

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Process, 2021-2034 (USD Million) (Million Units)

- 7.1 Key trends

- 7.2 Edge

- 7.3 Cloud

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Million Units)

- 8.1 Key trends

- 8.2 Semiconductor manufacturing

- 8.3 Flat panel display (FPD) manufacturing

- 8.4 MEMS (micro-electro-mechanical systems)

- 8.5 LED manufacturing

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Million Units)

- 9.1 Key trends

- 9.2 Integrated Device Manufacturers (IDMs)

- 9.3 Foundries

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ASML Holding NV

- 11.2 Advantest Corporation

- 11.3 Applied Materials Inc

- 11.4 Canon Inc.

- 11.5 Carl Zeiss SMT

- 11.6 EV Group

- 11.7 Hitachi High-Tech Corporation

- 11.8 Holon co Ltd.

- 11.9 KLA Corporation

- 11.10 KLA-Tencor

- 11.11 LAM Research

- 11.12 Nikon Corporation

- 11.13 Nova Measuring Instruments Ltd.

- 11.14 Onto innovation

- 11.15 Thermo Fisher Scientific Inc.