PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666936

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666936

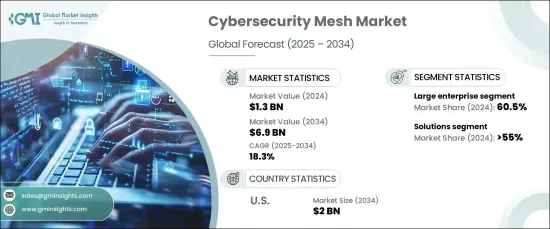

Cybersecurity Mesh Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Cybersecurity Mesh Market, valued at USD 1.3 billion in 2024, is expected to grow at a CAGR of 18.3% from 2025 to 2034. This growth is largely driven by the increasing sophistication of cyber threats, which demand more advanced and adaptive security solutions. Traditional security methods are no longer sufficient to protect organizations from modern attackers who utilize artificial intelligence (AI) and automation to exploit vulnerabilities. As a result, companies are looking for solutions that provide real-time threat detection, advanced analytics, and automated responses. This shift in demand is accelerating the adoption of cybersecurity mesh architectures, which are designed to secure complex, decentralized environments, including cloud and on-premises resources.

The rise in hybrid and multi-cloud environments is another significant factor contributing to the market's expansion. While these environments offer flexibility, scalability, and cost-efficiency, they also complicate security management. Organizations need to ensure that their security strategies can protect sensitive data and workloads across various cloud platforms while maintaining seamless interoperability between different systems. This increased complexity highlights the need for advanced cybersecurity mesh solutions to monitor and secure diverse endpoints and networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 18.3% |

The market is segmented into solutions and services, with the solutions segment holding the largest market share in 2024, accounting for more than 55%. The demand for integrated, decentralized security solutions that provide comprehensive protection across a variety of environments is driving this dominance. These solutions offer real-time threat detection, risk management, and automated responses, making them critical for organizations handling sensitive data and operating large-scale digital infrastructures.

The services segment, while smaller, is also experiencing growth. The increasing adoption of cybersecurity mesh has created a demand for expert consultation, implementation, and managed services to effectively integrate and optimize these solutions within organizations' existing IT ecosystems. This trend is particularly noticeable in large enterprises, which account for over 60% of the market share due to their need for scalable and flexible cybersecurity solutions that can secure distributed networks and vast volumes of data.

Small and medium-sized enterprises (SME) are also adopting cybersecurity mesh, though their market share is smaller. SME are increasingly looking for cost-effective, scalable solutions that can be customized to suit their specific needs. With a greater reliance on digital platforms and cloud-based services, SME are recognizing the value of cybersecurity mesh in safeguarding their networks and endpoints from cyber threats.

In the U.S., the market for cybersecurity mesh is expected to reach nearly USD 2 billion by 2034, driven by the growing demand for integrated, flexible, and scalable security solutions that can protect complex IT infrastructures. Major companies in the industry are investing in AI, machine learning, and advanced analytics to improve their cybersecurity offerings and meet the evolving needs of various sectors, including finance, healthcare, and government.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 End use

- 3.3 Profit margin analysis

- 3.4 Patent analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Use cases

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise in sophisticated cyber threats

- 3.9.1.2 Adoption of hybrid and multi-cloud environments

- 3.9.1.3 Regulatory compliance requirements

- 3.9.1.4 Expansion of IOT and edge computing

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation costs

- 3.9.2.2 Complexity in integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Solutions

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-Premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Vertical, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Banking

- 8.3 IT & Telecom

- 8.4 Healthcare

- 8.5 Insurance

- 8.6 Government

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Check Point

- 10.2 Cisco

- 10.3 CrowdStrike

- 10.4 Darktrace

- 10.5 F5

- 10.6 FireEye

- 10.7 Fortinet

- 10.8 IBM

- 10.9 Juniper Networks

- 10.10 McAfee

- 10.11 Microsoft

- 10.12 Palo Alto Networks

- 10.13 Proofpoint

- 10.14 RSA

- 10.15 SentinelOne

- 10.16 Sophos

- 10.17 Symantec

- 10.18 Tenable

- 10.19 Trend Micro

- 10.20 Zscaler