PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666710

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666710

Pipe Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

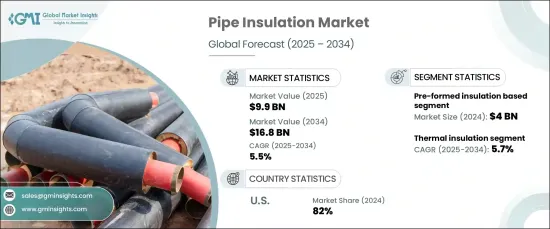

The Global Pipe Insulation Market was valued at USD 9.9 billion in 2024 and is expected to grow at a CAGR of 5.5% from 2025 to 2034. This growth is largely driven by the increasing focus on energy efficiency, compliance with regulatory standards, and the rising adoption of sustainable construction practices. Insulating pipes effectively minimizes energy loss in heating and cooling systems, contributing to improved energy efficiency in residential, commercial, and industrial settings.

As energy costs continue to climb and the urgency to reduce carbon emissions intensifies, pipe insulation is gaining prominence as a practical solution to lower overall energy consumption. It helps maintain consistent temperatures in piping systems, reducing the energy required for heating or cooling, thus offering long-term cost savings and sustainability benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 5.5% |

The market is segmented by product type into pre-formed insulation, rigid board insulation, blanket insulation, roll insulation, spray foam insulation, and others. Among these, pre-formed insulation emerged as a leading segment, generating approximately USD 4 billion in revenue in 2024. This segment is projected to grow steadily, owing to its user-friendly installation process and ability to accommodate various pipe dimensions and configurations. Manufactured using materials such as fiberglass and mineral wool, pre-formed insulation reduces labor costs and installation time, making it a preferred choice across sectors.

By function, the market is categorized into thermal insulation, acoustic insulation, fire protection, and others. Thermal insulation accounted for around 40% of the market share in 2024 and is anticipated to grow at a CAGR of 5.7% over the forecast period. Its primary role is to maintain temperature consistency in pipes, thus minimizing energy waste and optimizing performance in industrial processes. This functionality is particularly important in sectors like manufacturing and energy production, where efficiency and operational cost reduction are priorities.

Regionally, the United States dominates the North America pipe insulation market, holding a substantial share of approximately 82%. Stricter building codes and energy-efficiency mandates are fueling demand for advanced insulation solutions. Regulatory frameworks aim to reduce energy loss in HVAC and plumbing systems, boosting the adoption of high-performance insulation materials.

The pipe insulation market is poised for robust growth, driven by the increasing emphasis on energy conservation and the need for efficient and sustainable infrastructure solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 5.1 Key trends

- 5.2 Pre-formed insulation

- 5.3 Rigid board insulation

- 5.4 Blanket insulation

- 5.5 Roll insulation

- 5.6 Spray Foam insulation

- 5.7 Others (loose fill insulation, etc.)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 6.1 Key trends

- 6.2 Fiberglass

- 6.3 Mineral wool

- 6.4 Polyurethane

- 6.5 Polyethylene

- 6.6 Elastomeric foam

- 6.7 Rubber

- 6.8 Others (calcium silicate, etc.)

Chapter 7 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Thousand Square Feet)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Fire protection

- 7.5 Others (condensation control, etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Thousand Square Feet)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.4.1 Oil & gas

- 8.4.2 Chemical

- 8.4.3 Energy & power

- 8.4.4 Marine

- 8.4.5 Others (pharmaceutical, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Thousand Square Feet)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Thousand Square Feet)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Alfa Laval

- 11.3 Armacell International

- 11.4 BASF

- 11.5 Covestro

- 11.6 Huntsman Corporation

- 11.7 Insulation Technologies

- 11.8 Johns Manville

- 11.9 Kingspan Group

- 11.10 Knauf Insulation

- 11.11 Owens Corning

- 11.12 Rockwool International

- 11.13 Saint Gobain

- 11.14 Shenzhen Lanxuan Industrial

- 11.15 Thermaflex