PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666688

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666688

Automotive Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

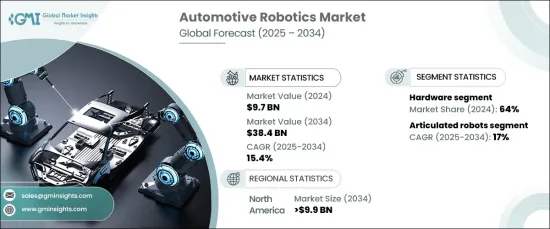

The Global Automotive Robotics Market, valued at USD 9.7 billion in 2024, is expected to expand at a CAGR of 15.4% from 2025 to 2034. This surge is driven by the increasing reliance on automation to streamline automotive manufacturing, improve efficiency, and enhance production quality. The integration of robotics into the industry ensures greater consistency, reduces errors, and boosts productivity, with automation becoming essential in key operations such as assembly, welding, and material handling.

One of the primary factors fueling the demand for automotive robotics is the need for improved manufacturing precision and efficiency. Modern vehicle designs, especially those involving electric or hybrid models, demand a higher level of accuracy. Robots are critical in performing tasks like welding, painting, and assembly, all with a level of precision that surpasses manual labor. The automation of repetitive tasks reduces production times, increases throughput, and maintains high-quality standards. Additionally, the integration of robotics with IoT and smart manufacturing, enabled by Industry 4.0 technologies, optimizes production workflows and lowers operational costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.7 Billion |

| Forecast Value | $38.4 Billion |

| CAGR | 15.4% |

The automotive robotics market is divided into three key segments: hardware, software, and services. Among these, the hardware segment holds the largest share, accounting for approximately 64% of the market in 2024. This segment includes components like robotic arms, sensors, actuators, and controllers, which are crucial for enhancing the accuracy, speed, and durability of robotic systems. As the demand for more advanced, lightweight, and precise hardware increases, manufacturers continue to invest in cutting-edge technology to meet the complex demands of automotive production.

When it comes to robot types, articulated robots dominate the market due to their versatility and precision. They are particularly effective in performing tasks such as welding, painting, and material handling. The advanced capabilities of articulated robots, including multi-axis movement and real-time adjustments, contribute to their widespread use in automotive manufacturing. Their flexibility allows them to cater to both mass production and customized manufacturing needs, making them an essential part of the automotive sector's automation strategy.

In North America, the U.S. automotive robotics market is expected to exceed USD 9.9 billion by 2034. The country's growth in this sector is driven by advanced manufacturing technologies, the adoption of smart factories, and the rise of electric vehicles (EVs). The focus on flexible automation systems, including the integration of AI and collaborative robots (cobots), is expected to play a key role in shaping the market's future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Growth drivers

- 3.7.1 Increased demand for automation

- 3.7.2 Surge in demand for electric and autonomous vehicles

- 3.7.3 Focus on safety and worker well-being

- 3.7.4 Rise of collaborative robots (cobots)

- 3.7.5 Ongoing technological advancements in robotics

- 3.8 Industry pitfalls & challenges

- 3.8.1 High Initial Investment

- 3.8.2 Skilled labor shortages for robotics operation

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Controller

- 5.2.2 Robot arm

- 5.2.3 End-effector

- 5.2.4 Sensors

- 5.2.4.1 Vision sensors

- 5.2.4.2 Force/torque sensors

- 5.2.4.3 Others

- 5.2.5 Others

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD billion)

- 6.1 Key trends

- 6.2 Articulated robots

- 6.2.1 4-axis robots

- 6.2.2 6-axis robots

- 6.2.3 Others

- 6.3 Scara robots

- 6.4 Cartesian robots

- 6.5 Cylindrical robots

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD billion)

- 7.1 Key trends

- 7.2 Material handling

- 7.3 Welding

- 7.3.1 Spot welding

- 7.3.2 Arc welding

- 7.4 Assembly/disassembly

- 7.5 Inspection

- 7.6 Cutting and processing

- 7.7 Logistics and warehouse automation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Payload Capacity, 2021-2034 (USD billion)

- 8.1 Key trends

- 8.2 Up to 16 kg

- 8.3 16–60 kg

- 8.4 60–225 kg

- 8.5 More than 225 kg

Chapter 9 Market Estimates & Forecast, By Deployment Type, 2021-2034 (USD billion)

- 9.1 Key trends

- 9.2 Fixed robots

- 9.3 Mobile robots

- 9.3.1 Automated Guided Vehicles (AGVs)

- 9.3.2 Autonomous Mobile Robots (AMRs)

Chapter 10 Market Estimates & Forecast, By Technology, 2021-2034 (USD billion)

- 10.1 Key trends

- 10.2 Machine learning and artificial intelligence

- 10.3 3D vision systems

- 10.4 IoT integration

- 10.5 Cloud robotics

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Comau SpA

- 12.3 Denso Wave

- 12.4 Dürr AG

- 12.5 Fanuc Corporation

- 12.6 Harmonic Drive System

- 12.7 Kawasaki Heavy Industries

- 12.8 KUKA Robotics

- 12.9 Nachi-Fujikoshi Corp

- 12.10 Omron Corporation

- 12.11 Panasonic Welding Systems Co. Ltd.

- 12.12 Reis Gmbh & Co.

- 12.13 Rockwell Automation

- 12.14 Seiko Epson Corporation

- 12.15 Stäubli

- 12.16 Universal Robots

- 12.17 Yamaha Robotics

- 12.18 Yaskawa Electric Corporation