PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666652

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666652

Andalusite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

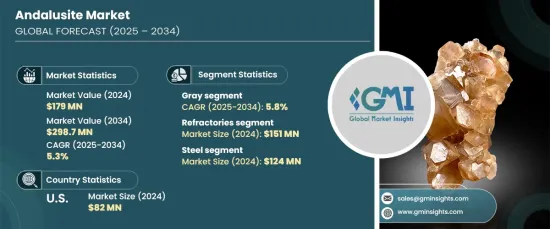

The Global Andalusite Market, valued at USD 179 million in 2024, is expected to grow at a CAGR of 5.3% between 2025 and 2034. This expansion is primarily driven by the increasing demand for refractory materials, particularly in the steel industry, the rising consumption of cement for large-scale infrastructure projects, and the growing use of andalusite in glass manufacturing.

The natural advantages of andalusite, such as its cost-effectiveness compared to synthetic alternatives and the environmentally friendly mining process, enhance its attractiveness across various industrial sectors. Moreover, the ongoing industrialization of emerging economies, coupled with the widening applications of andalusite in ceramics, foundries, and other industries, is expected to further fuel market growth. As the world shifts toward more sustainable production methods and materials, andalusite's natural origins and cost-saving properties position it as a preferred choice for businesses seeking efficiency and eco-friendly solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $179 Million |

| Forecast Value | $298.7 Million |

| CAGR | 5.3% |

The gray andalusite segment is a dominant player in the market, with a value of USD 60.7 million in 2024, and it is projected to grow at a CAGR of 5.8% through 2034. While gray remains the most popular variation, demand for colored andalusite, including pink, yellow, green, and violet, is rising due to the increasing focus on customization and personalization in various industries. The mineral's aesthetic appeal supports its integration into jewelry, ceramics, and decorative applications, where consumers increasingly prefer unique and visually striking products. This surge in demand for diverse andalusite colors reflects a broader shift in consumer preferences for distinctive, high-quality materials that combine beauty with functionality.

In terms of applications, the refractories segment remains the largest contributor to the market, reaching USD 151 million in 2024. It is expected to maintain a steady growth rate of 5.3% throughout the forecast period. Andalusite's remarkable ability to endure extreme temperatures and resist thermal shock makes it an ideal material for refractory linings used in industries such as steel, cement, and glass manufacturing. With the rapid expansion of global infrastructure projects and industrial activities, the need for durable, heat-resistant materials is increasing. Particularly, the steel industry continues to drive demand for andalusite, with ongoing growth in construction, automotive manufacturing, and infrastructure development around the world.

The U.S. andalusite market, valued at USD 82 million in 2024, is projected to grow at a robust CAGR of 5.6% through 2034. This growth is fueled by the country's robust industrial expansion, driven by significant investments in infrastructure and steel production. As the U.S. continues to modernize its steel industry and expand cement manufacturing, the demand for high-performance refractory materials like andalusite is expected to soar. The continued focus on improving efficiency and reducing production costs will contribute to the rising use of andalusite, further cementing its position as a key material in the nation's industrial landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for energy-efficient buildings

- 3.6.1.2 Growing automotive industry

- 3.6.1.3 Expanding solar energy sector

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.2.2 Availability of substitute products

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pink

- 5.3 Gray

- 5.4 Yellow

- 5.5 Green

- 5.6 Violet

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Refractories

- 6.3 Foundry

- 6.4 Kiln furniture

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Steel

- 7.3 Glass

- 7.4 Aluminum

- 7.5 Cement

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Andalucita

- 9.2 Andalucite Resources

- 9.3 Altech Chemicals

- 9.4 Golcha Minerals

- 9.5 Hamersley Andalusite

- 9.6 Halliburton (Andalusite Resources)

- 9.7 Imerys Andalusite

- 9.8 LKAB Minerals

- 9.9 Samrec Vermiculite

- 9.10 Thermolith