PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665335

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665335

Automotive Thermoelectric Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

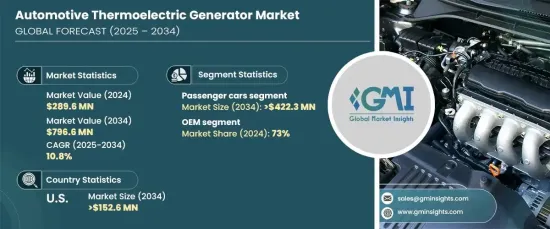

The Global Automotive Thermoelectric Generator Market, valued at USD 289.6 million in 2024, is set to experience robust growth, projected at a CAGR of 10.8% from 2025 to 2034. This growth is driven by the rising costs of fuel and increasingly stringent government regulations aimed at reducing vehicle emissions. As a result, the demand for technologies that enhance fuel efficiency and minimize environmental impact is surging.

A significant driver of this market expansion is the growing popularity of electric and hybrid vehicles. These advanced vehicles rely on energy management systems to optimize battery performance and driving range. ATEGs, which convert waste heat from exhaust systems into usable electricity, play a pivotal role in this optimization. By powering auxiliary systems and supporting battery charging, these generators contribute to enhanced energy efficiency in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $289.6 Million |

| Forecast Value | $796.6 Million |

| CAGR | 10.8% |

In terms of vehicle type, the market is segmented into passenger cars, commercial vehicles, and hybrid and electric vehicles. Passenger cars led the market in 2024, commanding 57% of the market share. This segment is forecasted to generate USD 422.3 million by 2034, fueled by the mass production of passenger vehicles and the increasing demand for fuel-efficient technologies. The widespread adoption of ATEGs in passenger cars creates substantial opportunities for innovation and integration of energy recovery systems, ensuring continuous growth in this segment.

The market is further categorized based on sales channels into original equipment manufacturers (OEMs) and aftermarket. In 2024, OEMs dominated with a 73% share, a trend expected to persist throughout the forecast period. OEMs excel in seamlessly incorporating ATEGs into vehicles during the manufacturing process, ensuring compatibility and optimized performance. By fulfilling bulk orders for automakers, OEMs achieve cost efficiencies while accelerating the adoption of these technologies. Additionally, their technical expertise enables them to design systems tailored to specific vehicle architectures, enhancing overall efficiency and reliability.

In the United States, the automotive thermoelectric generator market held an impressive 86% share in 2024 and is projected to reach USD 152.6 million by 2034. Stringent fuel efficiency and emissions regulations, including the Corporate Average Fuel Economy (CAFE) standards, are key drivers of this demand. The U.S. market also benefits from a high demand for premium and luxury vehicles, which increasingly incorporate advanced fuel-saving systems. Furthermore, significant investments in research and development, coupled with the presence of leading ATEG manufacturers, foster innovation and support the market's growth trajectory.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for fuel efficiency

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing adoption of electric and hybrid vehicles

- 3.7.1.4 Technological advancements in thermoelectric materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial cost of technology

- 3.7.2.2 Limited awareness among consumers

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Bismuth telluride

- 5.3 Lead telluride

- 5.4 Silicon germanium

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Hybrid and electric vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Waste heat recovery

- 7.3 Power generation

- 7.4 Battery management

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet Energy

- 10.2 European Thermodynamics

- 10.3 Faurecia

- 10.4 Ferrotec Holdings Corporation

- 10.5 Gentherm Incorporated

- 10.6 Hi-Z Technology, Inc.

- 10.7 II-VI Marlow

- 10.8 KELK Ltd.

- 10.9 Komatsu Ltd.

- 10.10 Laird Thermal Systems

- 10.11 SANGO Co., Ltd.

- 10.12 Tenneco Inc.

- 10.13 Thermonamic Electronics (Jiangxi) Corp., Ltd.

- 10.14 Valeo

- 10.15 Yamaha Motor Co., Ltd.