PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665315

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665315

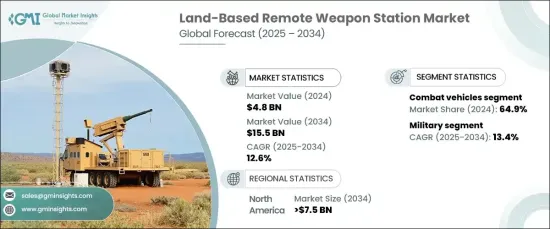

Land-Based Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Land-Based Remote Weapon Station Market is projected to reach USD 4.8 billion in 2024 and is expected to grow at a robust CAGR of 12.6% from 2025 to 2034. The market growth is largely driven by the rising demand for advanced defense systems and the ongoing modernization of military forces. As nations prioritize enhancing combat effectiveness and troop safety, the adoption of automated and remote-controlled weapon systems is reshaping modern warfare. These systems offer superior precision, reduce the risk to operators, and play a crucial role in evolving combat strategies.

The market is categorized by platform, with combat vehicles taking the lead, holding a dominant share of 64.9% in 2024. This segment continues to expand as the need for enhanced firepower, situational awareness, and protection against emerging threats intensifies. Remote-controlled weapon stations (RCWS) integrated into combat vehicles allow operators to engage targets with high accuracy while remaining securely inside the vehicle. These systems are key to providing both offensive and defensive capabilities, making them an indispensable part of modern armored platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 billion |

| Forecast Value | $15.5 billion |

| CAGR | 12.6% |

In terms of application, the land-based remote weapon station market is divided into military and homeland security sectors. The military segment is the fastest-growing, expected to increase at a CAGR of 13.4% through 2034. Demand for force protection, precision targeting, and overall operational efficiency is driving this growth. Remote weapon stations are critical components of armored vehicles, defense trucks, and fixed military installations. These systems not only enhance surveillance and targeting accuracy but also improve response times, all while minimizing the exposure of personnel to hostile environments. Their widespread deployment underscores their vital role in enhancing troop safety and combat performance.

In North America, the land-based remote weapon station market is forecasted to reach USD 7.5 billion by 2034. This growth is fueled by significant defense spending and ongoing investments in military modernization. The United States, in particular, is leading the charge by integrating advanced remote-controlled systems into its armored vehicles and defense infrastructure. The increasing use of artificial intelligence and automation in these systems is further driving innovation, boosting targeting capabilities, and improving operational efficiency. Continued investments in autonomous defense technologies are strengthening the region's defense posture and addressing evolving security challenges.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for precision targeting in modern warfare operations

- 3.6.1.2 Increasing military investments in advanced land-based defense systems

- 3.6.1.3 Growing adoption of remote-operated systems for soldier safety

- 3.6.1.4 Technological advancements enhancing weapon system interoperability and efficiency

- 3.6.1.5 Geopolitical tensions driving procurement of advanced military equipment

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and integration costs for advanced weapon systems

- 3.6.2.2 Regulatory and export challenges impacting global market opportunities

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Combat Vehicles

- 5.2.1 Main battle tanks

- 5.2.2 Infantry fighting vehicles

- 5.2.3 Armored fighting vehicles

- 5.2.4 Unmanned ground vehicles

- 5.2.5 Others

- 5.3 Stationary Structures

Chapter 6 Market Estimates & Forecast, By Weapon Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Lethal Weapons

- 6.2.1 Small Caliber

- 6.2.1.1 5.56mm

- 6.2.1.2 7.62mm

- 6.2.1.3 12.7mm

- 6.2.2 Medium Caliber

- 6.2.3 20mm

- 6.2.4 25mm

- 6.2.5 30mm

- 6.2.6 40mm

- 6.2.1 Small Caliber

- 6.3 Non-lethal Weapons

Chapter 7 Market Estimates & Forecast, By Mobility, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Fixed

- 7.3 Moving

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Military

- 8.3 Homeland Security

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aselsan A.S.

- 10.2 BAE Systems

- 10.3 Bharat Electronics Limited (BEL)

- 10.4 Copenhagen Sensor Technology

- 10.5 Elbit Systems Ltd.

- 10.6 EVPU Defense

- 10.7 FN Herstal

- 10.8 General Dynamics Corporation

- 10.9 Hornet

- 10.10 Israel Aerospace Industries (IAI)

- 10.11 Kongsberg Gruppen

- 10.12 Leonardo S.p.A.

- 10.13 Northrop Grumman Corporation

- 10.14 Rafael Advanced Defense Systems

- 10.15 Raytheon Technologies Corporation

- 10.16 Rheinmetall AG

- 10.17 Saab AB

- 10.18 Singapore Technologies Engineering Ltd.

- 10.19 Thales Group