PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665240

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665240

Monopolar Electrosurgery Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

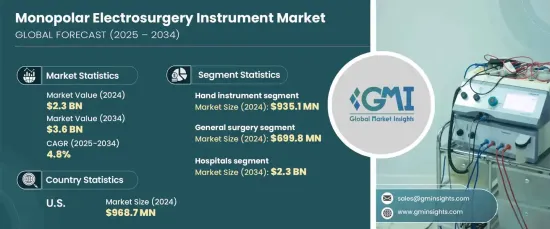

The Global Monopolar Electrosurgery Instrument Market reached USD 2.3 billion in 2024 and is expected to experience strong growth, with a projected CAGR of 4.8% from 2025 to 2034. This growth is driven by the increasing demand for minimally invasive procedures, the rising prevalence of chronic diseases, and expanding healthcare investments around the world. Additionally, technological advancements and the growing need for precise surgical instruments are fueling the market's upward trajectory.

Minimally invasive procedures have become standard practice across various medical specialties such as general surgery, gynecology, urology, and gastroenterology. Monopolar electrosurgery instruments play a crucial role in these fields due to their precision, efficiency, and ability to minimize tissue damage during surgical procedures. Their versatility in cutting, coagulating, and desiccating tissues makes them indispensable for both routine and complex surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.8% |

The market is segmented into product types, including hand instruments, electrosurgical generators, dispersive electrodes, and accessories. The hand instrument segment led the market with a revenue of USD 935.1 million in 2024. These instruments are widely used across numerous surgical disciplines, offering the precision and control required for delicate procedures. Their adaptability to both open and minimally invasive surgeries ensures they remain the dominant segment, addressing a wide array of medical needs.

In terms of application, the market is divided into general surgery, cardiovascular surgery, gynecology, neurosurgery, and others. General surgery accounted for USD 699.8 million in 2024 and is projected to grow at a CAGR of 4.6% during the forecast period. Monopolar electrosurgery instruments are highly regarded in this segment for their efficiency in managing soft tissues, providing hemostasis, and reducing surgical time. Their ability to enhance surgical outcomes and promote faster patient recovery continues to drive demand across hospitals and surgical centers.

The U.S. monopolar electrosurgery instrument market generated USD 968.7 million in 2024. This market is expected to grow at a CAGR of 4.2% through 2034, supported by the presence of leading manufacturers and a well-established healthcare infrastructure. The growing prevalence of chronic conditions and the increasing adoption of minimally invasive procedures contribute to sustained demand for these instruments. Additionally, the availability of advanced medical training and expertise further accelerates the adoption of monopolar electrosurgery instruments, reinforcing the U.S.'s leadership position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive procedures

- 3.2.1.2 Advancements in electrosurgical technologies

- 3.2.1.3 Growing prevalence of chronic diseases

- 3.2.1.4 Rising global healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of thermal injuries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hand instrument

- 5.3 Electrosurgical generators

- 5.4 Dispersive electrodes

- 5.5 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Cardiovascular surgery

- 6.4 Gynecology surgery

- 6.5 Neurosurgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apyx Medical

- 9.2 B.Braun

- 9.3 BOWA MEDICAL

- 9.4 CONMED

- 9.5 Encision

- 9.6 Erbe Elektromedizin

- 9.7 Johnson & Johnson

- 9.8 KLS Martin Group

- 9.9 Medtronic

- 9.10 Meyer-Haake

- 9.11 Olympus

- 9.12 Stryker