PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665218

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665218

On-orbit Satellite Servicing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

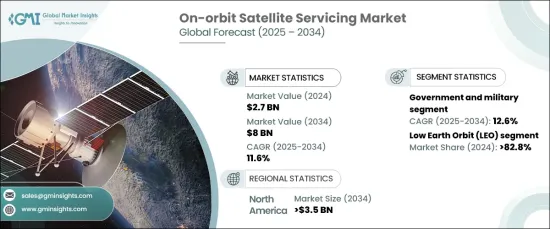

The Global On-Orbit Satellite Servicing Market is poised for significant growth, reaching USD 2.7 billion in 2024, with projections pointing to an impressive CAGR of 11.6% from 2025 to 2034. This rapid expansion is driven by the increasing demand for satellite maintenance, repair, and upgrades aimed at extending operational lifespans, cutting launch costs, and boosting performance. The rising deployment of satellites for key applications such as communications, Earth observation, and defense further accelerates the market's growth trajectory.

When analyzing the market by orbit type, Low Earth Orbit (LEO) takes the lead, commanding 82.8% of the market share in 2024. LEO's dominance can be attributed to the explosion of satellite constellations, particularly those focused on global broadband coverage and remote sensing. The dense satellite presence in this orbit necessitates innovative solutions, including robotic refueling, repair, and debris removal. Additionally, the proximity of LEO to Earth makes it easier to conduct frequent and cost-effective servicing missions, ensuring the sustainability and efficiency of satellite operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $8 Billion |

| CAGR | 11.6% |

In terms of end users, the on-orbit satellite servicing market is segmented into government and military entities and commercial operators. The government and military segment is expected to experience the fastest growth, with a forecasted CAGR of 12.6% during the 2025-2034 period. Increased investments in satellite infrastructure are fueling this demand as governments seek to preserve the functionality of critical space assets, enhance national security, and reduce replacement costs. Furthermore, collaborations between the public and private sectors are driving technological advancements, which will play a crucial role in accelerating the growth of this segment.

North America is set to dominate the global on-orbit satellite servicing market, with expectations to reach USD 3.5 billion by 2034. The region's strong position stems from substantial investments in space technologies and a well-established presence of key players in the industry. Government programs supporting innovation, coupled with increasing demand for satellite communication and defense solutions, are solidifying North America's leadership in this space. Additionally, the region's commitment to sustainable space practices and breakthroughs in in-orbit servicing technologies further enhances its market position.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in satellite constellations and space traffic

- 3.6.1.2 Cost savings through satellite lifecycle extension

- 3.6.1.3 Breakthroughs in space robotics and automation

- 3.6.1.4 Growing government and private sector investment

- 3.6.1.5 Enhanced focus on space debris management

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 High development and operational costs

- 3.6.4 Technical complexity and operational risks

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Active Debris Removal (ADR) and Orbit Adjustment

- 5.3 Robotic servicing

- 5.4 Refueling

- 5.5 Assembly

Chapter 6 Market Estimates & Forecast, By Orbit Type, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Low Earth Orbit (LEO)

- 6.3 Medium Earth Orbit (MEO)

- 6.4 Geostationary Orbit (GEO)

Chapter 7 Market Estimates & Forecast, By Satellite Type, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Small satellite (<500 Kg)

- 7.3 Medium satellite (501-1,000 Kg)

- 7.4 Large satellite (>1,000 Kg)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 Government and military

- 8.3 Commercial operators

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airbus SE

- 10.2 Altius Space Machines, Inc.

- 10.3 Astroscale Holdings Inc.

- 10.4 Atomos Space

- 10.5 ClearSpace

- 10.6 Future Space Industries

- 10.7 High Earth Orbit Robotics

- 10.8 Hyoristic Innovations

- 10.9 Infinite Orbits

- 10.10 Lúnasa Ltd.

- 10.11 Maxar Technologies

- 10.12 Momentus, Inc.

- 10.13 Nanoracks (Voyager Space)

- 10.14 Obruta Space Solutions Corp

- 10.15 Orbit Fab, Inc.

- 10.16 Orbitaid Aerospace Private Limited

- 10.17 Orion AST

- 10.18 Rogue Space Systems

- 10.19 Scout Aerospace LLC

- 10.20 Space Machines Company Pty Ltd

- 10.21 Tethers Unlimited, Inc.

- 10.22 Thales Alenia Space

- 10.23 Turion Space