PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665212

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665212

Display Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

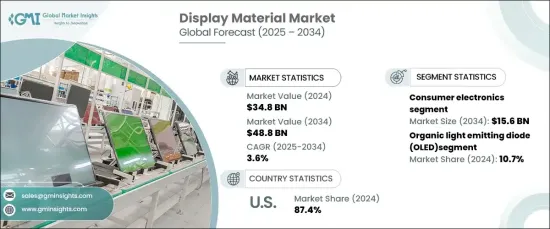

The Global Display Material Market was valued at USD 34.8 billion in 2024 and is expected to expand at a robust CAGR of 3.6% from 2025 to 2034. This growth is fueled by the rising demand for advanced consumer electronics, such as smartphones, tablets, and wearables, as consumers increasingly seek devices with enhanced visual quality, vibrant colors, and superior energy efficiency.

Technological innovations in display materials are revolutionizing the industry, enabling manufacturers to create high-quality visual experiences that also meet energy-saving demands. The growing popularity of flexible and foldable displays is also driving market demand, especially in premium devices. This trend is further accelerated by the continuous evolution of display technologies, making it easier for consumers to access products with advanced visual capabilities while promoting energy conservation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.8 Billion |

| Forecast Value | $48.8 Billion |

| CAGR | 3.6% |

The display material market is primarily segmented by technology, including micro-LED display, organic light-emitting diode (OLED), liquid crystal display (LCD), quantum dot display, and e-paper display (EPD). OLED technology dominated in 2024, accounting for a significant share of 10.7%. This technology is recognized for its self-emissive pixels, which deliver deeper blacks, vibrant colors, and faster response times. OLED's thin, flexible design makes it an ideal choice for high-end displays in smartphones, televisions, and emerging augmented reality (AR) and virtual reality (VR) applications, solidifying its position as the go-to technology for cutting-edge devices.

In terms of application, the display material market spans several industries, including consumer electronics, automotive, healthcare, retail, industrial and enterprise sectors, among others. The consumer electronics segment is projected to reach USD 15.6 billion by 2034, continuing to be the largest source of revenue in the market. This expansion is attributed to the increasing consumer preference for high-resolution, energy-efficient displays in products such as laptops, gaming monitors, and smart wearables. Displays are now an essential component, enhancing both the functionality and aesthetic appeal of modern consumer electronics.

The U.S. display material market held a dominant share of 87.4% in 2024, driven by rapid technological advancements, high consumer spending, and the swift adoption of innovative devices. The growing integration of display technologies in AR, VR, automotive displays, and healthcare imaging systems further fuels market demand in the region. Furthermore, substantial investments in research and development by leading manufacturers help reinforce the U.S.'s position as a global leader in display material innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surging demand for advanced consumer electronics

- 3.6.1.2 Growth of the automotive display sector

- 3.6.1.3 Rapid advancements in display technologies

- 3.6.1.4 Increasing penetration of high-resolution displays

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs and capital investment requirements

- 3.6.2.2 Supply chain disruptions and resource dependence

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Polarizers

- 5.3 Glass substrates

- 5.4 Color filters

- 5.5 Liquid crystals (LC)

- 5.6 Backlighting units (BLU)

- 5.7 Adhesives

- 5.8 Indium tin oxide (ITO)

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Healthcare

- 6.5 Retail

- 6.6 Industrial and enterprise

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Liquid crystal display (LCD)

- 7.3 Organic light emitting diode (OLED)

- 7.4 Quantum dot display

- 7.5 Micro LED display

- 7.6 E-paper display (EPD)

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 AGC Inc. (Asahi Glass Co., Ltd.)

- 9.3 AU Optronics Corporation

- 9.4 BOE Technology Group Co., Ltd.

- 9.5 Corning Incorporated

- 9.6 DIC Corporation

- 9.7 DowDuPont Inc.

- 9.8 Hitachi Chemical Co., Ltd.

- 9.9 Idemitsu Kosan Co., Ltd.

- 9.10 Innolux Corporation

- 9.11 Japan Display Inc.

- 9.12 JNC Corporation

- 9.13 Kyulux, Inc.

- 9.14 LG Chem, Ltd.

- 9.15 Lumileds Holding B.V.

- 9.16 Merck KGaA

- 9.17 Nanoco Technologies Limited

- 9.18 Nitto Denko Corporation

- 9.19 Samsung Display Co., Ltd.

- 9.20 Sumitomo Chemical Co., Ltd.

- 9.21 Toray Industries, Inc.

- 9.22 Universal Display Corporation