PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665035

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665035

Automotive Battery Disconnect Unit (BDU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

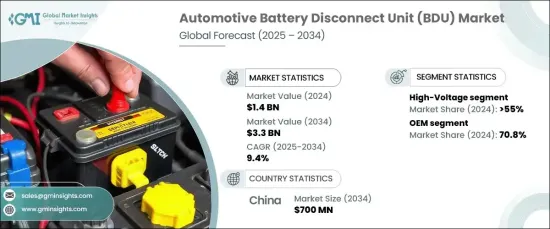

The Global Automotive Battery Disconnect Unit Market was valued at USD 1.4 billion in 2024 and is forecasted to grow at a remarkable CAGR of 9.4% between 2025 and 2034. This growth is propelled by advancements in BDU technology, particularly the integration of smart monitoring systems. Modern BDUs are now equipped with cutting-edge sensors and Internet of Things (IoT) capabilities, enabling real-time monitoring of voltage, current, and temperature. These innovations significantly enhance vehicle safety and performance, making BDUs an indispensable component of modern automotive systems.

The surging adoption of electric vehicles (EVs) in emerging markets is a key driver behind the increasing demand for advanced BDUs. As nations accelerate their transition to electric mobility, the need for cost-effective, scalable, and climate-resilient BDUs is on the rise. Governments worldwide are fueling this momentum with supportive policies, including EV incentives and the rapid expansion of charging infrastructure. This shift further underscores the demand for BDUs engineered to operate reliably across diverse conditions and environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 9.4% |

Segmented by voltage, the market comprises high-voltage and low-voltage BDUs. High-voltage BDUs accounted for 55% of the market share in 2024, reflecting their pivotal role in electric and hybrid vehicles. These BDUs are critical for managing and storing energy in EV battery systems while ensuring safety by preventing electrical hazards such as short circuits. With stricter safety regulations and a growing focus on high-performance battery systems for both passenger and commercial vehicles, the demand for high-voltage BDUs is expected to witness substantial growth in the coming years.

The market is also categorized by distribution channel into original equipment manufacturers (OEMs) and the aftermarket. In 2024, OEMs dominated with a 70.8% market share, driven by the incorporation of BDUs as standard components in new vehicles. OEMs leverage economies of scale to deliver high-quality BDUs at competitive prices, meeting the rising demand for advanced safety and automation technologies. Continuous innovation and strategic collaborations with suppliers further enhance BDU technology, ensuring it aligns with evolving regulatory standards and consumer preferences.

China is emerging as a powerhouse in the automotive BDU market, projected to reach USD 700 million by 2034. As a global leader in automotive manufacturing, China is experiencing a surge in demand for BDUs as automakers prioritize safety, energy efficiency, and performance in their EV offerings. The region's rapid urbanization, coupled with increasing disposable incomes, is driving vehicle sales and the adoption of advanced automotive technologies, solidifying China's position as a key player in the BDU market's future growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEMs

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 Service providers

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Price analysis of Battery Disconnect Unit (BDU)

- 3.5 Patent analysis

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Expansion of EV markets in emerging economies

- 3.9.1.2 Advances in smart BDU technologies

- 3.9.1.3 Rising adoption of solid-state relays

- 3.9.1.4 Integration of BDUs with battery management systems (BMS) and energy storage solutions.

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High costs of advanced BDUs

- 3.9.2.2 Complexity in design and integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 High voltage

- 5.3 Low voltage

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric vehicles

- 8.3.1 Battery Electric Vehicles (BEVs)

- 8.3.2 Plug-in Hybrid Electric Vehicles (PHEVs)

- 8.3.3 Hybrid Electric Vehicles (HEVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Automotive Grade Linux

- 10.3 Bosch

- 10.4 Continental

- 10.5 Denso

- 10.6 Eaton

- 10.7 Honeywell

- 10.8 Johnson Controls

- 10.9 Kyocera

- 10.10 Lear

- 10.11 Littelfuse

- 10.12 Mitsubishi Electric

- 10.13 Panasonic

- 10.14 Schaeffler

- 10.15 Sensata Technologies

- 10.16 Siemens

- 10.17 STMicroelectronics

- 10.18 Valeo

- 10.19 Vitesco Technologies

- 10.20 ZF Friedrichshafen