PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665034

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1665034

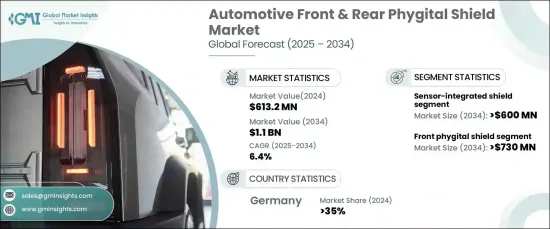

Automotive Front and Rear Phygital Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Automotive Front And Rear Phygital Shield Market was valued at USD 613.2 million in 2024 and is projected to grow at a robust CAGR of 6.4% from 2025 to 2034. Phygital shields have emerged as a critical component in the integration of cutting-edge sensor systems such as LiDAR, radar, and cameras, which are pivotal for the navigation, communication, and safety of autonomous and connected vehicles. These shields are meticulously designed to incorporate these advanced technologies while maintaining the vehicle's aesthetic appeal, meeting both functional and stylistic demands.

The market is segmented by product type into front phygital shields and rear phygital shields. In 2024, front phygital shields held the lion's share, accounting for 65% of the market. This segment is anticipated to reach USD 730 million by 2034, driven by the growing adoption of LED and display-enabled front shields in electric and luxury vehicles. These advanced shields incorporate features such as adaptive lighting systems and digital displays, which provide dynamic branding, signaling, and enhanced communication capabilities-key differentiators in modern automotive design.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $613.2 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.4% |

On the technology front, the market is categorized into sensor-integrated shields, LED/display shields, and aerodynamic shields. Sensor-integrated shields are forecasted to generate USD 600 million by 2034, showcasing rapid advancements in smart shield technology. These shields now feature preprocessing capabilities that handle sensor data before it reaches the vehicle's central systems. By enabling distributed processing, they significantly reduce latency and enhance real-time decision-making for autonomous driving features. Furthermore, the ability to support over-the-air (OTA) updates aligns with the growing emphasis on edge computing, enabling automakers to refine sensor algorithms remotely and ensure continuous performance enhancements.

Germany represented a significant share of the market in 2024, accounting for 35% of the global demand. As a leading hub for automotive innovation, the country is home to numerous premium automotive manufacturers driving the adoption of advanced phygital shields. These shields play an integral role in housing sensors and cameras essential for Advanced Driver Assistance Systems (ADAS), which power features like lane-keeping assistance, collision avoidance, and pedestrian detection. The rising focus on vehicle safety and autonomy in the automotive sector continues to fuel the demand for these technologically sophisticated shields.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Tier-1 suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Technology integrators

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 Sensor integration

- 3.4.2 LED lighting and display systems

- 3.4.3 Aerodynamic design enhancements

- 3.4.4 Others

- 3.5 Key news & initiatives

- 3.6 Patent analysis

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rise in electric vehicle adoption

- 3.8.1.2 Growth of autonomous and connected vehicles

- 3.8.1.3 Growing consumer demand for vehicle personalization

- 3.8.1.4 Growing focus on aerodynamics of vehicle body

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development costs

- 3.8.2.2 Complex manufacturing process

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front phygital shield

- 5.3 Rear phygital shield

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Sensor-integrated shield

- 7.3 LED/display

- 7.4 Aerodynamic

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Plastic/polymer-based

- 8.3 Metal-based

- 8.4 Composite

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Covestro

- 11.2 Forvia Hella

- 11.3 Harman

- 11.4 Hyundai Mobis

- 11.5 Infineon

- 11.6 Intops

- 11.7 Kia

- 11.8 Magna

- 11.9 Marelli

- 11.10 Motherson

- 11.11 Niebling

- 11.12 Plastic Omnium

- 11.13 Prolim

- 11.14 Texas Instruments

- 11.15 Valeo