PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1664902

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1664902

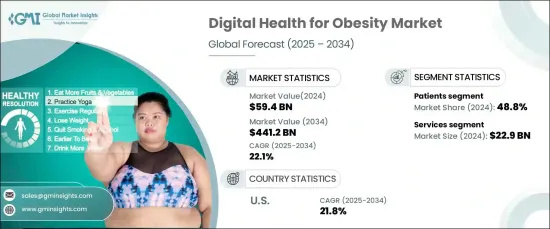

Digital Health for Obesity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Digital Health For Obesity Market was valued at USD 59.4 billion in 2024 and is anticipated to grow at an impressive CAGR of 22.1% from 2025 to 2034. This rapid expansion is driven by the rising global prevalence of obesity and the increasing adoption of cutting-edge technologies such as AI and data analytics, revolutionizing weight management with personalized and effective solutions.

The global market is categorized into software, hardware, and services, with the services segment leading the charge. In 2024, the services segment held a dominant position, valued at USD 22.9 billion. Its prominence stems from its ability to deliver comprehensive support, including personalized consultations, remote monitoring, and ongoing guidance for individuals managing health conditions like obesity. By bridging the gap between technology and patient care, services ensure tailored recommendations and sustained user engagement, making them indispensable in the digital health ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $59.4 Billion |

| Forecast Value | $441.2 Billion |

| CAGR | 22.1% |

By end use, the market is segmented into patients, providers, payers, and other end-users, with the patients segment capturing the largest market share of 48.8% in 2024. This leadership position is fueled by the surging demand for personalized and accessible healthcare solutions. Patients are the primary users of digital health tools, leveraging mobile apps, wearables, and other technologies to effectively monitor and manage obesity. The growing awareness of health and wellness, coupled with the ease and convenience of self-management, is further propelling the adoption of digital health solutions among individuals.

The U.S. digital health for obesity market is set to maintain its dominance through 2032, with a robust CAGR of 21.8%. This leadership is underpinned by a strong ecosystem of technology companies, healthcare providers, and research institutions, which drive innovation in digital health solutions. Additionally, the rising prevalence of obesity and associated chronic diseases in the U.S. has amplified the demand for effective management tools, including mobile apps, wearables, and telemedicine platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of obesity

- 3.2.1.2 Growing adoption of mHealth and wearable devices

- 3.2.1.3 Advances in telemedicine and remote monitoring

- 3.2.1.4 Increasing awareness and focus on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 Low digital awareness and accessibility

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology trends

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Hardware

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Patients

- 6.3 Providers

- 6.4 Payers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allurion

- 8.2 Calibrate Health

- 8.3 Ilant Health

- 8.4 Intellihealth

- 8.5 Noom

- 8.6 Omada Health

- 8.7 Qardio

- 8.8 Teladoc Health

- 8.9 Twin Health

- 8.10 Vida Health

- 8.11 Virta Health

- 8.12 Welldoc

- 8.13 WW International