PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071314

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071314

Durable Medical Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

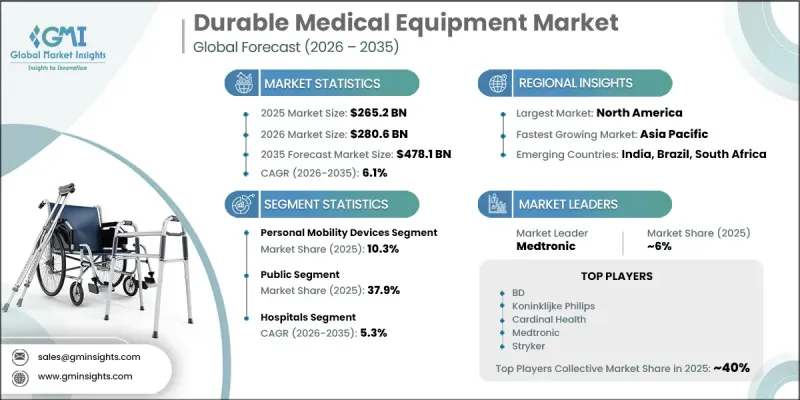

The Global Durable Medical Equipment Market was valued at USD 265.2 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 478.1 billion by 2035.

Growth is driven by the combined impact of an aging global population, the increasing prevalence of chronic diseases, and sustained investments in healthcare delivery models that emphasize decentralized and patient-centered care. The market is undergoing a significant transformation as healthcare systems increasingly shift from traditional facility-based treatment toward continuous care delivered within community and home settings. This transition is expanding the patient base that relies on durable medical equipment while increasing demand across a broad range of product categories, including mobility aids, patient support equipment, monitoring solutions, and essential medical consumables. The growing preference for home-based care is supported by advances in telehealth infrastructure, improved device accessibility, and expanding reimbursement coverage for a wider range of medical equipment. Beyond patient convenience, healthcare providers and payers are increasingly recognizing home care as a cost-effective approach that improves outcomes while reducing the burden on hospitals and other acute care facilities. These long-term structural trends are expected to remain key contributors to market expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $265.2 Billion |

| Forecast Value | $478.1 Billion |

| CAGR | 6.1% |

The personal mobility devices segment accounted for 10.3% share in 2025 and is projected to grow at a CAGR of 6.3% through 2035. The segment continues to benefit from rising demand among elderly individuals and patients experiencing mobility limitations caused by chronic health conditions, injuries, or age-related physical decline. Increasing life expectancy and the expanding global senior population are creating favorable conditions for sustained demand within this category. As healthcare providers place greater emphasis on patient independence, mobility enhancement, and quality-of-life improvements, the adoption of personal mobility equipment is expected to increase steadily across both developed and emerging healthcare markets.

The hospitals segment held a 34% share in 2025. Hospitals remain major purchasers of durable medical equipment due to the broad range of products required for patient treatment, monitoring, mobility assistance, and clinical care delivery. Procurement activities within healthcare institutions are increasingly focused on balancing clinical effectiveness, operational efficiency, and long-term value. Ongoing investments in healthcare infrastructure, patient safety initiatives, and advanced treatment capabilities continue to support equipment purchases across public and private hospital systems worldwide.

North America Durable Medical Equipment Market held a 31.2% share, growing at a CAGR of 4% through 2035. The United States remains the primary contributor to regional growth, supported by a highly developed healthcare ecosystem, extensive reimbursement programs, and strong adoption of home healthcare services. The region continues to benefit from significant healthcare spending, widespread access to medical technologies, and growing demand for equipment that supports chronic disease management and aging populations. In addition, evolving reimbursement structures and value-based care initiatives are encouraging the use of home-based treatment solutions, remote patient monitoring technologies, and specialized medical equipment, further strengthening market growth across North America.

Major companies operating in the global durable medical equipment market include CAREX Health Brands, INVACARE Corporation, Drive DeVilbiss Healthcare, Baxter International, Graham-Field, Cardinal Health, Coloplast, COMPASS HEALTH Brands, MEDLINE Industries, Koninklijke Philips, INTCO MEDICAL, B. Braun, Getinge, BD (Becton, Dickinson and Company), and ConvaTec. Companies operating in the durable medical equipment market are implementing a range of strategic initiatives to strengthen their market position and expand their customer base. Leading manufacturers are investing heavily in product innovation, digital health integration, and connected medical technologies that support remote patient monitoring and home-based care. Organizations are also focusing on expanding their distribution networks, strengthening partnerships with healthcare providers, and enhancing direct-to-consumer sales channels to improve market reach. Strategic acquisitions, portfolio diversification, and investments in advanced manufacturing capabilities are helping companies improve operational efficiency and address evolving patient needs.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Payer trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising patient preference for home-based care

- 3.2.1.2 Increasing prevalence of chronic diseases globally

- 3.2.1.3 Growing geriatric population

- 3.2.1.4 Technological advancements in products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device costs and affordability challenges

- 3.2.2.2 Complexity of Pediatric-Focused Product Development

- 3.2.3 Opportunities

- 3.2.3.1 AI/ML integration and predictive analytics

- 3.2.3.2 Emerging markets expansion and infrastructure development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pricing analysis, 2025

- 3.6 Technology and innovation landscape (Driven by Primary Research)

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Investment landscape

- 3.8 Reimbursement scenario

- 3.9 Healthcare delivery model transformation

- 3.10 Personalized medicine and precision healthcare applications

- 3.11 Software as medical device (SaMD) integrated analysis

- 3.12 Future market trends (Driven by Primary Research)

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Personal mobility devices

- 5.2.1 Wheelchair and scooter

- 5.2.2 Crutches and canes

- 5.2.3 Walkers

- 5.2.4 Other personal mobility devices

- 5.3 Monitoring and therapeutic devices

- 5.3.1 Oxygen equipment

- 5.3.2 Blood glucose analyzers

- 5.3.3 Vital sign monitors

- 5.3.4 Infusion pumps

- 5.3.5 Continuous positive airway pressure (CPAP) devices

- 5.3.6 Nebulizers

- 5.3.7 Other monitoring and therapeutic devices

- 5.4 Bathroom safety devices

- 5.5 Medical furniture

- 5.6 Incontinence pads

- 5.7 Breast pumps

- 5.8 Catheters

- 5.9 Consumables and accessories

- 5.10 Other products

Chapter 6 Market Estimates and Forecast, By Payer, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Public

- 6.3 Private

- 6.4 Out-of-pocket

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Home healthcare

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. Braun

- 9.2 Baxter

- 9.3 BD

- 9.4 Cardinal Health

- 9.5 CAREX

- 9.6 Coloplast

- 9.7 COMPASS HEALTH

- 9.8 convaTec

- 9.9 drive DeVilbiss Healthcare

- 9.10 Getinge

- 9.11 graham-field

- 9.12 INTCO MEDICAL

- 9.13 INVACARE

- 9.14 Koninklijke Philips

- 9.15 MEDLINE

- 9.16 Medtronic

- 9.17 ResMed

- 9.18 Stryker

- 9.19 SUNRISE MEDICAL