PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844331

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1844331

Airway Clearance Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

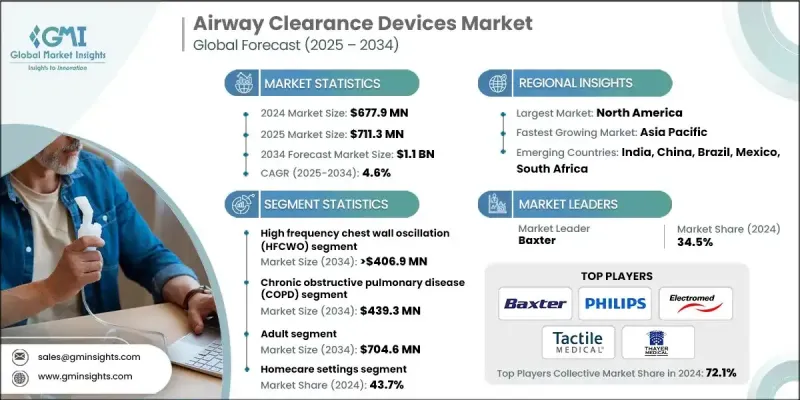

The Global Airway Clearance Devices Market was valued at USD 677.9 million in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 1.1 billion by 2034.

The rising prevalence of respiratory illnesses, advancements in technology, an aging population, and greater awareness of airway therapy are all key contributors to this market's growth. Healthcare providers, payers, and life sciences companies are increasingly adopting airway clearance solutions to improve outcomes, streamline care delivery, and enhance regulatory compliance. The introduction of high-frequency chest wall oscillation (HFCWO) vests, oscillatory positive expiratory pressure (OPEP) systems, and connected digital health solutions is reshaping how patients manage chronic pulmonary conditions. These innovations enable personalized therapy adjustments and remote monitoring, making care more efficient and patient-centric.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $677.9 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 4.6% |

Patient education initiatives and awareness programs are helping boost early diagnosis and adherence to respiratory treatments. At the same time, rising global healthcare expenditure, supportive reimbursement frameworks, and public health initiatives for managing chronic lung diseases are encouraging higher adoption of airway clearance therapies across regions. With the push toward outpatient and home care models, the demand for compact, user-friendly, and non-invasive respiratory devices is expected to rise consistently over the forecast period.

In 2024, the flutter mucus clearance device segment reached USD 152 million and is forecast to grow at a CAGR of 5.3% through 2034. These devices are becoming increasingly popular due to their compact design, ease of use, and cost-efficiency. They are particularly well-suited for individuals with less severe respiratory issues and are often preferred for self-administered care. Their affordability also makes them accessible in low-resource settings and across a wide range of healthcare systems. As the focus shifts toward prevention and remote care, these devices offer a convenient option for maintaining respiratory health in non-hospital environments.

The chronic obstructive pulmonary disease (COPD) segment held a 42% share and is expected to reach USD 439.3 million by 2034. COPD remains one of the most widespread respiratory conditions globally, with environmental and lifestyle factors such as pollution, smoking, and occupational hazards driving its prevalence. Patients with COPD frequently suffer from mucus build-up and obstructed airways, creating a strong need for effective airway clearance to improve breathing, reduce hospitalizations, and enhance daily function.

North America Airway Clearance Devices Market held a 38.7% share in 2024. The region benefits from well-established healthcare infrastructure, high adoption of durable medical equipment, and favorable regulatory frameworks. There's growing use of oscillatory and air-pulse devices in residential settings, driven by initiatives aimed at promoting independent care and improving quality of life. The region's focus on personalized treatment and integration of advanced technologies into home care is accelerating the uptake of airway clearance solutions.

Key players shaping the Global Airway Clearance Devices Market include ICU Medical, Monaghan Medical Corporation, VYAIRE MEDICAL, Baxter, Dymedso, ABM Respiratory Care, Mercury Medical, Pari Medical, Thayer Medical, Sentec, Dima Italia, Electromed, Tactile Medical, Philips, Pneumo Care Health, and VORTRAN Medical Technology. Leading companies in the airway clearance devices market are pursuing product innovation, digital integration, and strategic collaborations to reinforce their market presence. By incorporating smart connectivity, remote monitoring, and personalized therapy features, they're making devices more intuitive and responsive to patient needs. Firms are also expanding their distribution networks globally and entering new geographic markets to tap into unmet demand. Several players are investing in clinical research to validate device efficacy and meet evolving regulatory standards. Mergers and partnerships with respiratory care providers, hospitals, and telehealth platforms allow for greater adoption in both inpatient and home care environments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Device type trends

- 2.2.3 Application trends

- 2.2.4 Age group trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in incidence of respiratory conditions

- 3.2.1.2 Growing patient awareness and product launches

- 3.2.1.3 Increasing adoption of non-invasive treatment options

- 3.2.1.4 Surge in government initiatives towards controlling respiratory disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device cost and stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of digital health and remote monitoring

- 3.2.3.2 Product innovation and customization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Growth of portable and home-based airway clearance devices

- 3.5.1.2 Digital health platforms enabling remote monitoring

- 3.5.1.3 Patient-friendly oscillatory PEP and HFCWO systems

- 3.5.2 Emerging technologies

- 3.5.2.1 AI-powered respiratory monitoring and predictive analytics

- 3.5.2.2 Wearable connected airway clearance devices

- 3.5.2.3 Smart devices with adaptive therapy modes

- 3.5.1 Current technological trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.9.1 Convergence of AI, digital health, and connected devices

- 3.9.2 Expansion of homecare solutions for chronic respiratory care

- 3.9.3 Growth in emerging markets with improved infrastructure

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 High frequency chest wall oscillation (HFCWO)

- 5.3 Flutter mucus clearance device

- 5.4 Intrapulmonary percussive ventilation (IPV)

- 5.5 Mechanical cough assist devices

- 5.6 Positive expiratory pressure (PEP)

- 5.7 Other device types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic obstructive pulmonary disease (COPD)

- 6.3 Bronchiectasis

- 6.4 Cystic fibrosis

- 6.5 Neuromuscular

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Homecare settings

- 8.3 Hospital

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABM Respiratory Care

- 10.2 Baxter

- 10.3 Dima Italia

- 10.4 Dymedso

- 10.5 Electromed

- 10.6 ICU Medical

- 10.7 Philips

- 10.8 Mercury Medical

- 10.9 Monaghan Medical Corporation

- 10.10 Pari Medical

- 10.11 Pneumo Care Health

- 10.12 Sentec

- 10.13 Tactile Medical

- 10.14 Thayer Medical

- 10.15 VORTRAN Medical Technology

- 10.16 VYAIRE MEDICAL