PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716659

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716659

Advanced Air Mobility Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

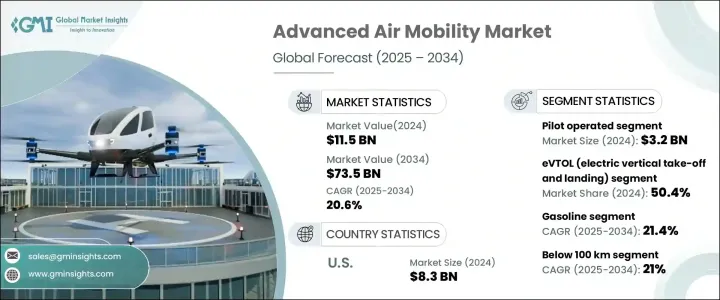

The Global Advanced Air Mobility Market generated USD 11.5 billion in 2024 and is projected to grow at a CAGR of 20.6% between 2025 and 2034. As the world intensifies its efforts to reduce carbon emissions and combat climate change, the transportation sector is undergoing a transformative shift toward cleaner solutions. Advanced air mobility is emerging as a game-changer, offering sustainable air transport options that reduce traffic congestion, enhance transportation efficiency, and minimize environmental impacts. The increasing integration of electric propulsion systems, autonomous technologies, and innovative vehicle designs is accelerating the adoption of AAM solutions.

Governments and regulatory authorities across the globe are supporting these advancements through favorable policies and investments, enabling rapid certification and commercialization of AAM technologies. Furthermore, the growing interest from urban planners and transportation authorities in incorporating AAM systems into smart city frameworks is driving market growth. With the rise of urbanization and increasing demand for faster and more efficient travel solutions, AAM is expected to revolutionize regional and urban mobility by offering seamless, point-to-point transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $73.5 Billion |

| CAGR | 20.6% |

The piloted advanced air mobility segment, valued at USD 3.2 billion in 2024, is witnessing robust growth as it blends human expertise with technological innovations to deliver safe and reliable urban air transportation. Piloted AAM vehicles offer an added layer of safety by leveraging the skills of experienced pilots, ensuring smooth operations even in complex or densely populated environments. Additionally, the integration of existing aviation infrastructure and the implementation of favorable regulatory frameworks are expediting the certification process, paving the way for faster deployment and wider acceptance of these technologies. As the industry moves toward autonomous solutions, piloted AAM vehicles are serving as a bridge to build public trust and refine operational processes.

The AAM market is categorized by vehicle types, including electric vertical take-off and landing (eVTOL) aircraft, short take-off and landing (STOL) aircraft, and conventional fixed-wing aircraft. In 2024, the eVTOL segment accounted for 50.4% of the market share, driven by the growing adoption of electric and hybrid propulsion systems. eVTOL aircraft are gaining traction due to their ability to meet passenger transportation requirements while adhering to stringent safety and operational standards. The development of eVTOL technology is expected to play a pivotal role in shaping the future of advanced air mobility, as these vehicles offer the potential for scalable, cost-effective, and environmentally sustainable transportation solutions.

The U.S. advanced air mobility market, valued at USD 8.3 billion in 2024, is positioned as a global leader fueled by a strong technological innovation ecosystem and the presence of prominent aerospace companies. With significant investments in research and development and a well-established infrastructure for testing and deploying new technologies, the U.S. is driving the advancement and adoption of AAM solutions. The country's proactive regulatory environment, combined with continuous collaboration between public and private sector stakeholders, is accelerating the commercialization of advanced air mobility technologies and positioning the U.S. as a frontrunner in the global AAM landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and traffic congestion

- 3.2.1.2 Changing consumer preferences

- 3.2.1.3 Investment and government support

- 3.2.1.4 Strategic partnerships and collaborations

- 3.2.1.5 Expansion of use cases and applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and safety challenges

- 3.2.2.2 Public acceptance and perception

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pilot operated

- 5.3 Autonomous/Remotely operated

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 eVTOL (Electric Vertical Takeoff and Landing) aircraft

- 6.3 STOL (Short Takeoff and Landing) aircraft

- 6.4 Conventional fixed-wing aircraft

Chapter 7 Market Estimates and Forecast, By Propulsion Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Gasoline

- 7.2.1 Turbine engines (Turbo)

- 7.2.2 Reciprocating (Piston) engines

- 7.3 Electric propulsion

- 7.4 Hybrid propulsion

Chapter 8 Market Estimates and Forecast, By Range, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 100 km

- 8.3 100 km – 250 km

- 8.4 250 km – 500 km

- 8.5 More than 500 km

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Cargo transport

- 9.3 Passenger transport

- 9.4 Mapping & surveying

- 9.5 Special mission

- 9.6 Surveillance & monitoring

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Commercial

- 10.3 Government & military

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Airbus S.A.S.

- 12.2 Aurora Flight Sciences

- 12.3 Bell Textron Inc.

- 12.4 Embraer S.A.

- 12.5 Garmin Aviation

- 12.6 GE Aviation

- 12.7 GKN Aerospace

- 12.8 Guangzhou EHang Intelligent Technology Co. Ltd.

- 12.9 Honywell

- 12.10 Joby Aviation

- 12.11 Lilium GmbH

- 12.12 Opener, Inc.

- 12.13 Safran

- 12.14 Siemens

- 12.15 Thales Group

- 12.16 The Boeing Company