PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750555

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750555

Retinal Disorder Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

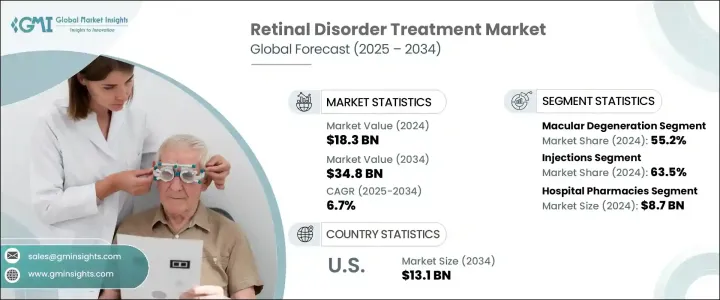

The Global Retinal Disorder Treatment Market was valued at USD 18.3 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 34.8 billion by 2034, driven by the increasing prevalence of diabetes, along with its complications such as diabetic retinopathy (DR) and diabetic macular edema (DME). Retinal disorder treatments encompass a range of medical, surgical, and pharmaceutical interventions, including anti-VEGF injections, laser therapy, corticosteroid treatments, and vitrectomy. The primary goal of these treatments is to prevent further retinal damage and preserve or restore vision. The selection of a treatment depends on the severity of the condition, the stage of the disorder, and the overall health of the patient's eye. DME is a leading cause of vision loss, particularly among individuals with type 2 diabetes, highlighting the need for timely interventions and specialized care.

Recent advancements in treatment methods, such as sustained-release intraocular therapies, enhance patient compliance by reducing the frequency of injections. For example, certain injectable devices are designed for continuous drug delivery, offering relief from frequent eye injections. These innovations are helping to minimize the treatment burden while providing more effective solutions for retinal disorders.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.3 Billion |

| Forecast Value | $34.8 Billion |

| CAGR | 6.7% |

Macular degeneration, particularly age-related macular degeneration (AMD), dominated the market in 2024, accounting for a 55% share. AMD, which primarily affects individuals over 60 years old, is one of the leading causes of vision loss in this age group. As the global population ages, comorbidities such as hypertension and obesity further exacerbate the prevalence of AMD, driving the need for continued research and treatment innovation.

The injection segment is a key driver in the market, accounting for 63.5% share in 2024. Intravitreal injections are commonly used for treating retinal conditions like AMD, retinal vein occlusion, and DME. Anti-VEGF therapies have shown promising results in treating these conditions, as they offer rapid therapeutic responses. Drugs such as Avastin, Eylea, and Lucentis are proving effective in reducing retinal edema and neovascularization, ultimately improving visual acuity for patients.

United States Retinal Disorder Treatment Market is poised to grow from USD 7.1 billion in 2024 to USD 13.1 billion by 2034, driven by the aging population susceptible to retinal conditions and the widespread availability of advanced intravitreal injection therapies. Moreover, favorable reimbursement policies and the strong presence of key pharmaceutical manufacturers continue to fuel market expansion.

Key players in the Global Retinal Disorder Treatment Market include Regeneron Pharmaceuticals, Bayer, AbbVie, Novartis, Pfizer, and F. Hoffmann-La Roche. These companies are investing in R&D and new product development to stay ahead in the competitive landscape. To strengthen their position in the retinal disorder treatment market, companies are focusing on expanding their product portfolios and advancing treatment technologies. Key strategies include forming partnerships to leverage complementary expertise in drug development and distribution. Furthermore, companies are enhancing patient treatment through innovative drug delivery systems and improved reimbursement structures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes

- 3.2.1.2 Rising geriatric population

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Macular degeneration

- 5.2.1 Wet macular degeneration

- 5.2.2 Dry macular degeneration

- 5.3 Diabetic retinopathy

- 5.4 Inherited retinal diseases (IRDs)

- 5.5 Diabetic macular edema

- 5.6 Retinal vein occlusion

- 5.7 Other types

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Capsules and tablets

- 6.3 Eye drops

- 6.4 Eye solutions

- 6.5 Gels

- 6.6 Ointments

- 6.7 Injections

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Alimera Sciences

- 9.3 Amgen

- 9.4 Apellis Pharmaceuticals

- 9.5 Astellas Pharma

- 9.6 Bayer

- 9.7 Biogen

- 9.8 Bausch + Lomb

- 9.9 Celltrion

- 9.10 F. Hoffmann-La Roche

- 9.11 Novartis

- 9.12 Pfizer

- 9.13 Regeneron Pharmaceutical

- 9.14 Santen Pharmaceuticals

- 9.15 Sandoz Group