PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1859001

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1859001

Power Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

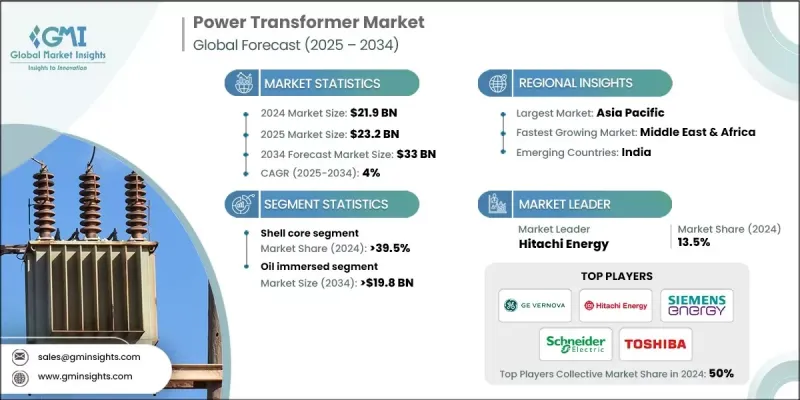

The Global Power Transformer Market was valued at USD 21.9 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 33 billion by 2034.

The increasing integration of renewable energy is fueling the demand for larger, high-voltage transformers to connect remote wind and solar farms to centralized load centers, ensuring the stability of fluctuating power outputs. As the need for more resilient and efficient grids grows, transformer manufacturers are focusing on localizing production to reduce supply chain vulnerabilities. The shift toward digital grids is also driving demand for transformers with embedded sensors and IoT capabilities to improve grid management and enable dynamic load balancing. Additionally, the regulatory push for higher energy efficiency is accelerating the demand for eco-friendly transformers, which use advanced materials such as amorphous steel cores and biodegradable insulating fluids. Utilities are moving toward adopting automation and digital control systems to improve grid efficiency, resilience, and reliability. Industry developments are shaped by hybrid AC/DC grid management, with utilities focusing on building smarter, more flexible grid systems to support renewable integration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.9 Billion |

| Forecast Value | $33 Billion |

| CAGR | 4% |

In 2024, the shell core power transformers accounted for a 39.5% share, with this segment projected to grow at a CAGR of 3.6% through 2034. These transformers are favored for their enhanced short-circuit strength, which makes them ideal for large-scale industrial and renewable integration projects.

The oil-immersed power transformers segment held 63.1% share and is expected to reach USD 19.8 billion by 2034, owing to their superior cooling and overload handling capabilities. These transformers are essential for high-voltage transmission and renewable integration projects that require high reliability and thermal efficiency. Self-cooled oil-immersed transformers continue to be used in rural and medium-voltage networks for their cost-effectiveness and minimal maintenance requirements.

U.S. Power Transformer Market held 74% share in 2024, with rapid grid modernization and electrification driving the demand for advanced transformer technologies. The market is supported by the need to replace aging transmission infrastructure and expand electric vehicle (EV) charging networks.

Prominent players operating in the Global Power Transformer Market include GE Vernova, Hitachi Energy, Mitsubishi Electric Corporation, Siemens Energy, Toshiba Energy Systems & Solutions Corporation, WEG, Schneider Electric, Bharat Heavy Electricals Limited, Bharat Bijlee Limited, Hyundai Electric & Energy Systems, Hammond Power Solutions, Kirloskar Electric Company, and Hyosung Heavy Industries. To strengthen their position in the power transformer market, companies are increasingly focusing on expanding their local manufacturing capabilities to cater to regional demand and reduce reliance on imports. Many are investing heavily in research and development to create more efficient and innovative transformer technologies, including solutions with integrated digital capabilities for smart grid management.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Core trends

- 2.1.3 Winding trends

- 2.1.4 Cooling trends

- 2.1.5 Insulation trends

- 2.1.6 Rating trends

- 2.1.7 Mounting trends

- 2.1.8 Application trends

- 2.1.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import export trade analysis

- 3.3.1 Key importing countries

- 3.3.2 Key exporting countries

- 3.4 Price trend analysis, (USD/Unit)

- 3.5 Cost analysis of power transformers

- 3.6 Industry impact forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.8.1 Bargaining power of suppliers

- 3.8.2 Bargaining power of buyers

- 3.8.3 Threat of new entrants

- 3.8.4 Threat of substitutes

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Core, 2021 - 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 Closed

- 5.3 Shell

- 5.4 Berry

Chapter 6 Market Size and Forecast, By Winding, 2021 - 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 Two winding

- 6.3 Auto-transformer

Chapter 7 Market Size and Forecast, By Cooling, 2021 - 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 Dry type

- 7.2.1 Self air

- 7.2.2 Air blast

- 7.3 Oil immersed

- 7.3.1 Self cooled

- 7.3.2 Water cooled

- 7.3.3 Forced oil

- 7.3.4 Others

Chapter 8 Market Size and Forecast, By Insulation, 2021 - 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 Gas

- 8.3 Oil

- 8.4 Solid

- 8.5 Air

- 8.6 Others

Chapter 9 Market Size and Forecast, By Rating, 2021 - 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 ≤ 100 MVA

- 9.3 > 100 MVA to ≤ 500 MVA

- 9.4 > 500 MVA to ≤ 800 MVA

- 9.5 > 800 MVA

Chapter 10 Market Size and Forecast, By Mounting, 2021 - 2034 (Units & USD Million)

- 10.1 Key trends

- 10.2 Pad

- 10.3 Pole

- 10.4 Others

Chapter 11 Market Size and Forecast, By Application, 2021 - 2034 (Units & USD Million)

- 11.1 Key trends

- 11.2 Residential

- 11.3 Commercial & industrial

- 11.4 Utility

Chapter 12 Market Size and Forecast, By Region, 2021 - 2034 (Units & USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 France

- 12.3.3 Russia

- 12.3.4 UK

- 12.3.5 Italy

- 12.3.6 Spain

- 12.3.7 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 South Korea

- 12.4.4 India

- 12.4.5 Australia

- 12.5 Middle East & Africa

- 12.5.1 Saudi Arabia

- 12.5.2 UAE

- 12.5.3 Qatar

- 12.5.4 Egypt

- 12.5.5 South Africa

- 12.5.6 Nigeria

- 12.6 Latin America

- 12.6.1 Brazil

- 12.6.2 Peru

- 12.6.3 Argentina

Chapter 13 Company Profiles

- 13.1 Bharat Heavy Electricals Limited

- 13.2 Bharat Bijlee Limited

- 13.3 CG Power & Industrial Solutions

- 13.4 Celme S.r.l.

- 13.5 DAIHEN Corporation

- 13.6 Grupo Comtrafo

- 13.7 GE Vernova

- 13.8 Hitachi Energy

- 13.9 Hyosung Heavy Industries

- 13.10 Hammond Power Solutions

- 13.11 Hyundai Electric & Energy Systems

- 13.12 Hangzhou Qiantang River Electric Group

- 13.13 JSHP Transformer

- 13.14 Kirloskar Electric Company

- 13.15 Mitsubishi Electric Corporation

- 13.16 Siemens Energy

- 13.17 Schneider Electric

- 13.18 Toshiba Energy Systems & Solutions Corporation

- 13.19 WEG

- 13.20 YueBian Electric